Opening an art gallery is an exciting entrepreneurial journey, but like any brick-and-mortar business, it requires real capital to get off the ground. From leasing a commercial space to building inventory, hiring staff, and marketing your brand, startup costs can add up quickly. That's where the SBA 7(a) loan program can make a meaningful difference. It's one of the most widely used financing tools available to small business owners in the United States, and creative entrepreneurs are increasingly turning to it for startup funding. However, the application process involves a thorough documentation requirement that many first-time borrowers find overwhelming. Understanding what documents are needed for SBA 7(a) loan for art gallery startup before you begin can save you significant time and improve your chances of approval.

Understanding the SBA 7(a) Loan and Why It Works for Creative Startups

The SBA 7(a) loan program is the Small Business Administration's flagship lending product, designed to help small businesses access affordable financing when traditional bank loans may not be an option. For art gallery startups, this program can be particularly well-suited because it covers a wide range of business expenses, including working capital, equipment, leasehold improvements, and even the purchase of commercial real estate.

SBA 7(a) loans are not issued directly by the SBA. Instead, the SBA guarantees a portion of the loan, which reduces the risk for lenders and makes them more willing to work with startups and newer businesses that may lack an extensive financial track record. This guarantee structure is one reason why financing for new creative businesses through the SBA 7(a) program has become increasingly popular.

For art gallery owners, loan proceeds might cover costs such as gallery renovation and build-out, lighting and display equipment, point-of-sale systems, initial artwork acquisition or consignment agreements, and marketing campaigns. Loan amounts can vary widely depending on the lender and the business plan, with the program generally supporting loans up to $5 million. Repayment terms may extend up to ten years for working capital and up to 25 years for real estate, which can help keep monthly payments manageable for a growing gallery.

SBA 7(a) Requirements Art Gallery Startup: Basic Eligibility First

Before diving into the document checklist, it's important to understand the basic eligibility criteria that apply to all SBA 7(a) borrowers. Meeting these requirements is the first step toward a successful application, and lenders will assess them before reviewing your documentation package.

- For-profit status: Your art gallery must operate as a for-profit business. Nonprofits and charitable arts organizations typically do not qualify for SBA 7(a) financing.

- Small business size standards: The SBA defines size eligibility based on industry. For retail galleries and most arts-related businesses, the standard is typically measured by annual revenue or number of employees. Your lender or an SBA resource partner can confirm the specific threshold for your NAICS code.

- U.S. operation: Your business must be physically located and operating within the United States or its territories.

- Owner equity investment: The SBA generally expects business owners to have some personal financial stake in the business, often referred to as a reasonable equity injection. For startups, this could mean personal savings or other contributed funds.

- Creditworthiness: While the SBA does not publish a hard minimum credit score, most participating lenders prefer a personal credit score of at least 650 to 680. Stronger credit improves your chances and may lead to better loan terms.

- No existing federal debt delinquency: Applicants must not be delinquent on any federal debt obligations, including student loans or prior government-backed loans.

Understanding these baseline SBA 7(a) requirements for art gallery startups early on helps you determine whether to proceed with a full application or address any gaps first.

What Documents Are Needed for SBA 7(a) Loan for Art Gallery Startup: The Core Checklist

This is the heart of the process. When you apply for an SBA 7(a) loan, lenders require a comprehensive set of documents to evaluate your creditworthiness, business viability, and ability to repay the loan. Below is a detailed breakdown of what you'll typically need to prepare.

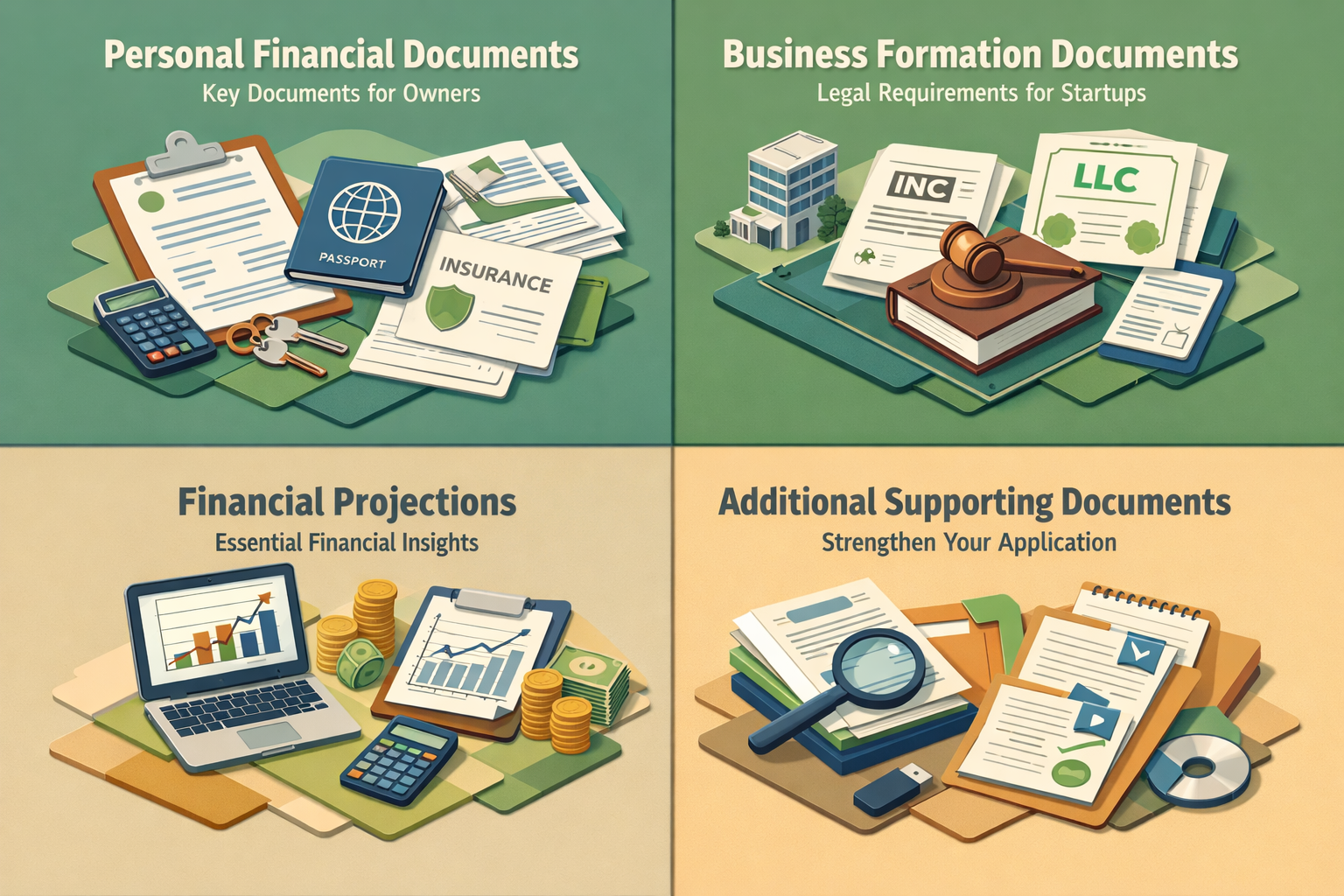

Personal Financial Documents

- Personal financial statement (SBA Form 413): This form captures your personal assets, liabilities, and net worth. Every owner with 20% or more ownership stake in the business is typically required to complete it.

- Personal tax returns: Most lenders request two to three years of personal federal tax returns to assess income history and financial stability.

- Government-issued photo ID: A valid driver's license or passport is standard.

- Resume or personal background statement: Lenders want to understand your professional history, especially any experience in the arts, retail, business management, or related fields.

Business Formation and Legal Documents

- Business plan: For a startup art gallery, this is arguably the most critical document. It should include an executive summary, market analysis, description of your gallery concept, operational plan, and detailed financial projections. Lenders use this to gauge whether your business model is viable and whether you understand your local market.

- Business licenses and permits: Copies of any state, county, or city business licenses required to legally operate your gallery.

- Articles of incorporation or organization: If your gallery is structured as an LLC, corporation, or partnership, you'll need to provide your formation documents.

- Operating agreement or bylaws: These outline how the business is managed and owned.

- Employer Identification Number (EIN): Your federal tax identification number, typically obtained through the IRS.

Financial Projections and Statements

- Startup cost estimate: A detailed list of all anticipated expenses needed to open your gallery, including leasehold improvements, equipment, signage, initial inventory, and working capital reserves.

- Projected profit and loss statements: Most lenders expect financial projections covering at least two to three years. These should be realistic and supported by market research.

- Cash flow projections: Monthly cash flow forecasts help lenders assess your ability to make loan payments, especially in the early months of operation.

- Balance sheet projection: A forward-looking snapshot of your expected assets, liabilities, and equity at launch and at key milestones.

Additional Supporting Documents That Strengthen Your Application

Beyond the core checklist, certain supplementary materials can meaningfully strengthen your application and demonstrate to lenders that you've done your homework as a prospective gallery owner.

Location and Lease Information

If you've already identified a space for your gallery, providing a signed or proposed commercial lease agreement can work in your favor. Lenders want to know where your business will be located, as foot traffic, neighborhood demographics, and lease terms all affect your revenue potential. If you're still searching for a space, a letter of intent from a landlord may be acceptable in the early stages.

Collateral Documentation

The SBA generally requires lenders to take available collateral to secure the loan. This might include business assets such as equipment and fixtures, or personal assets such as real estate equity. You'll need to provide documentation for any collateral being offered, such as a property appraisal, mortgage statement, or equipment list with estimated values.

Resumes and Industry Credentials

Because art galleries are a niche business, demonstrating relevant expertise can make a meaningful difference. If you have prior experience curating exhibitions, managing a creative business, working in retail, or building community partnerships with artists, document it thoroughly. Letters of support from established artists, art associations, or community organizations may also add credibility.

Franchise or Licensing Agreements (If Applicable)

If your gallery will operate under a franchise model or a licensed brand concept, include those agreements in your application package. The SBA has specific guidelines around franchise businesses, and lenders will want to review any franchisor disclosure documents.

SBA Borrower Application Forms

Standard SBA forms are also required as part of the application. These typically include SBA Form 1919 (Borrower Information Form) and SBA Form 912 (Statement of Personal History) for each owner. Your lender may also require additional proprietary forms depending on their internal underwriting process.

Building a Business Plan That Supports Financing for New Creative Businesses

For a startup art gallery, the business plan deserves special attention. Unlike an established business with years of financial records, a startup leans heavily on the strength of its plan to make the case for financing. This is especially true when it comes to financing for new creative businesses, where revenue can be harder to predict and the market may be more niche.

Your business plan should open with a compelling executive summary that clearly explains what your gallery does, who your target audience is, and why your concept is positioned to succeed in your chosen market. Follow this with a thorough market analysis that includes data on local arts attendance, competitive galleries, tourist demographics, and community interest in the arts.

Include a detailed description of your revenue model. Art galleries can generate income through artwork sales commissions, event hosting, membership programs, private sales, and art classes or workshops. The more diversified and well-explained your revenue streams, the more confidence lenders may have in your ability to repay the loan.

Financial projections should be grounded in realistic assumptions. Lenders are experienced at spotting overly optimistic forecasts, so it's better to present conservative but credible numbers supported by market data. If you have pre-committed consignment agreements with artists, letters of intent from corporate art buyers, or event bookings already lined up, include those as evidence of early demand.

Working with a SCORE mentor, a Small Business Development Center (SBDC) advisor, or a professional business plan writer who has experience with creative industry startups could be a worthwhile investment before you submit your application.

Tips to Improve Your Approval Odds Before You Apply

Preparing your documents is only part of the equation. There are several proactive steps you can take to strengthen your overall application profile before you submit it to a lender.

- Check and improve your personal credit: Review your credit reports from all three major bureaus well in advance. Dispute any inaccuracies and pay down outstanding balances where possible. A stronger credit score may give you access to better loan terms.

- Save for an equity injection: The SBA typically expects borrowers to contribute some of their own funds. A meaningful down payment — often in the range of 10% to 30% of total project costs for startups — signals commitment and reduces lender risk.

- Choose an SBA-preferred lender: Working with an SBA Preferred Lender can streamline the approval process. These lenders have delegated authority to approve loans without waiting for SBA review, which can reduce turnaround times significantly.

- Work with an SBA resource partner: Organizations like SCORE, Women's Business Centers, and SBDCs offer free or low-cost consulting and can help you refine your application before submission.

- Organize your documents early: Assembling a complete, well-organized application package demonstrates professionalism and may speed up the underwriting process. Missing documents are one of the most common reasons for delays.

●Conclusion

Understanding what documents are needed for SBA 7(a) loan for art gallery startup is the first real step toward turning your creative vision into a funded business. The application process may feel detailed and demanding, but it's designed to help lenders understand your opportunity and your ability to succeed. With a well-prepared business plan, organized financial documentation, and a clear picture of your gallery concept, you'll be in a much stronger position to secure the capital you need.

At LoanWise, we work with entrepreneurs across a wide range of industries, including creative and arts-based businesses, to help them navigate the SBA lending process with confidence. Whether you're just beginning to explore your options or you're ready to submit an application, our team can help you understand your financing choices and connect you with lenders who understand your vision. Reach out to LoanWise today and take the next step toward opening the gallery you've been dreaming about.