Running a rare book dealership is a fascinating and rewarding business. But like any specialty retail operation, it comes with unique cash flow challenges. You might need to purchase an entire estate collection before you have buyers lined up, or float inventory costs while waiting for an auction payout. A business line of credit can be an excellent tool for managing these financial gaps. However, before a lender approves your application, they'll want to see a clear picture of your business's health and stability. Understanding what documents are needed for a business line of credit for a rare book dealer can help you prepare a strong application and improve your chances of approval.

Why Rare Book Dealers Often Turn to Business Lines of Credit

The rare book trade is inherently unpredictable. Inventory opportunities can appear without warning — a private collection surfaces, a library deaccessions volumes, or a competitor closes shop. These moments demand fast capital. Unlike term loans, a business line of credit gives you flexible, revolving access to funds that you draw on as needed and repay over time.

For rare book dealers specifically, this flexibility is especially valuable. Your revenue may be seasonal or tied to major book fairs, auction schedules, and collector demand cycles. A line of credit helps bridge the gap between large inventory purchases and eventual sales. It can also cover everyday operating expenses like website maintenance, catalog printing, shipping supplies, and staff wages during slower periods.

Lenders understand that specialty retail businesses operate differently from traditional storefronts, but they still need documentation to assess risk. The more organized and complete your paperwork is, the smoother your application process is likely to be.

Core Business Documents Every Lender Will Typically Request

Regardless of your industry, most lenders start the review process with a set of foundational business documents. As a rare book dealer, you'll want to have these ready before you begin your application.

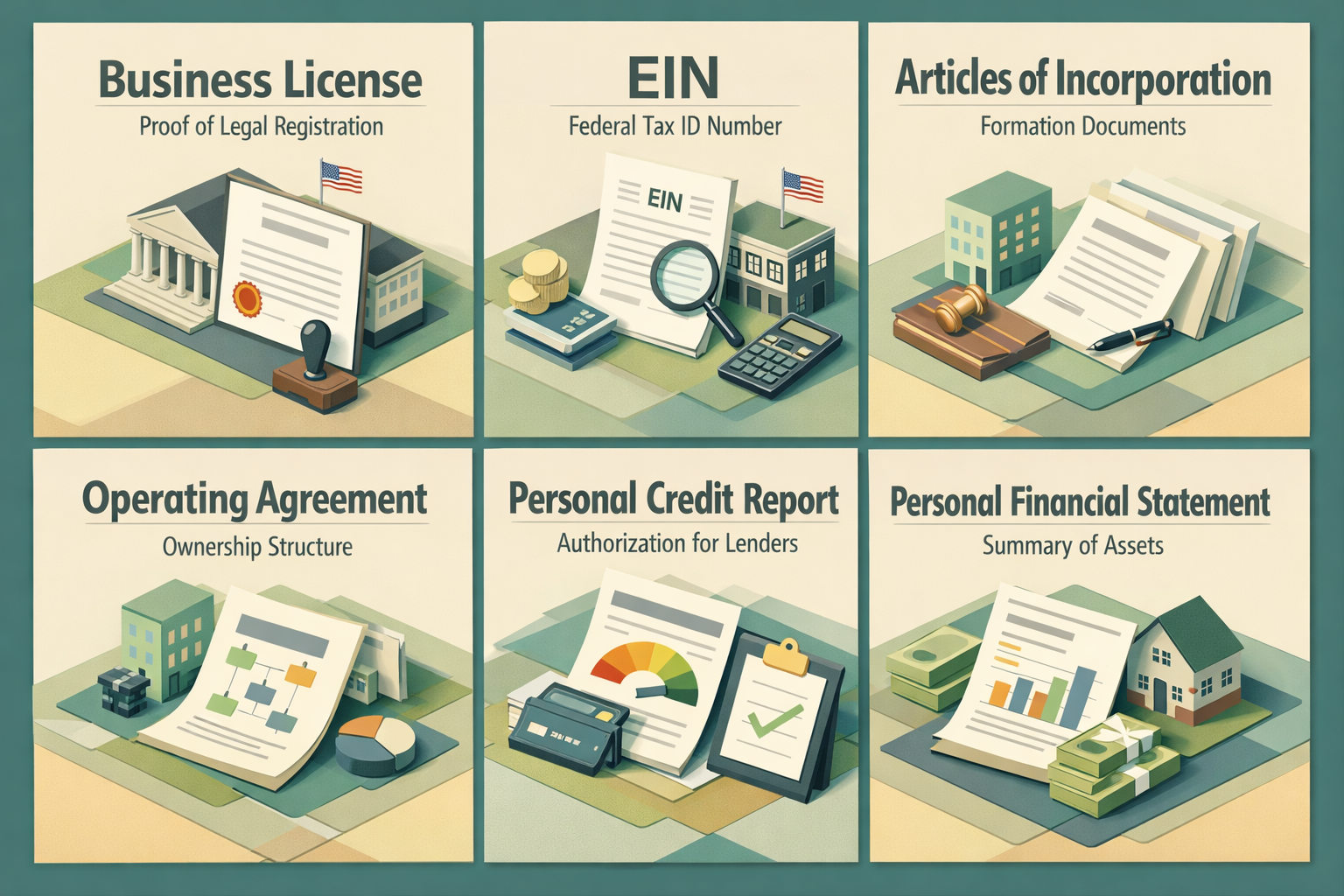

- Business license and registration: Proof that your dealership is legally registered in your state or locality. This could include a DBA (doing business as) certificate if you operate under a trade name.

- Employer Identification Number (EIN): Your federal tax ID number, issued by the IRS. If you operate as a sole proprietor, lenders may accept your Social Security Number instead, though an EIN adds a layer of credibility.

- Articles of incorporation or organization: If your dealership is structured as an LLC, corporation, or partnership, lenders will want to see your formation documents.

- Operating agreement or partnership agreement: These clarify ownership structure, which is important to lenders evaluating who is responsible for repayment.

Having clean, current versions of these documents on hand signals that your business is professionally managed — something that can work in your favor during underwriting.

Financial Statements That Show Your Business Can Repay

One of the most critical parts of understanding what documents are needed for a business line of credit for a rare book dealer involves your financial records. Lenders use these to evaluate your revenue trends, profitability, and ability to service new debt.

- Profit and loss statements (P&L): Most lenders will ask for at least two years of P&L statements. These show your total revenue, cost of goods sold (which for rare book dealers includes the cost of acquiring inventory), and net income.

- Balance sheet: A snapshot of your assets, liabilities, and equity. For rare book dealers, your inventory may represent a significant asset — lenders may scrutinize how it's valued.

- Cash flow statements: These illustrate how money moves through your business over time. Since rare book sales can be lumpy and irregular, demonstrating consistent cash flow — even with seasonal fluctuations — can strengthen your case.

If your bookkeeping isn't fully up to date, it's worth working with an accountant before applying. Lenders may view disorganized financials as a red flag, even if your business is fundamentally healthy.

Tax Returns and Bank Statements Lenders Commonly Require

Beyond internal financial statements, lenders typically want third-party verification of your income. This usually takes two forms: tax returns and bank statements.

Business tax returns for the past two to three years are a standard request. These confirm that the income you're reporting internally matches what you've declared to the IRS. Discrepancies between your P&L statements and tax returns can raise concerns, so consistency matters.

Personal tax returns may also be required, especially if your dealership is a sole proprietorship or small LLC where your personal finances are closely tied to the business. Lenders often view the owner's financial picture as an extension of the business's risk profile.

Business bank statements from the past three to twelve months give lenders a real-time view of your cash flow. They'll look at average daily balances, deposit frequency, and any overdrafts. For rare book dealers, irregular deposit patterns are common due to the nature of sales, so be prepared to explain any gaps or spikes in activity.

Personal Financial Information and Credit History Requirements

Most small business lenders — particularly banks and credit unions — will review the personal credit profile of the business owner as part of the application process. This is especially true if the business is relatively new or doesn't have a long credit history of its own.

You may be asked to provide:

- A personal credit report authorization: Lenders will pull your credit report with your permission. A score above 680 is often considered favorable, though requirements vary by lender and loan product.

- Personal financial statement: A summary of your personal assets, liabilities, and net worth. Some lenders have a standardized form for this.

- Personal guarantee: Many lenders require business owners — especially those of small or closely held companies — to personally guarantee the line of credit. This means you're agreeing to repay the debt from personal assets if the business cannot.

If your personal credit has blemishes, it doesn't necessarily disqualify you, but it may affect the credit limit offered or the interest rate applied. Being upfront with your lender about any issues and offering context can sometimes help.

Inventory Documentation and Business-Specific Details for Rare Book Dealers

Here's where rare book dealers face a unique documentation challenge. Unlike a hardware store or clothing boutique, your inventory consists of items with highly variable and sometimes subjective value. A first edition Hemingway and a mid-century paperback are both "books," but their financial weight is vastly different.

Lenders who are unfamiliar with the antiquarian book trade may need additional context. Consider preparing the following:

- Inventory records: A detailed list of your current stock, including acquisition cost and estimated market value. If you use dealer management software or a cataloging system like LibraryThing or Booxter, export reports can be helpful.

- Appraisal documentation: For high-value items, formal appraisals from a recognized expert or organization such as the Antiquarian Booksellers' Association of America (ABAA) may add credibility to your asset claims.

- Sales history: Records of past transactions, ideally showing consistent sales volume and revenue. This could come from your point-of-sale system, online marketplace reports (AbeBooks, BIBLIO, eBay), or customer invoices.

Providing this kind of documentation proactively may help lenders feel more comfortable extending credit to a business in a niche market they may not fully understand at first glance.

Tips for Strengthening Your Application as a Specialty Business Borrower

Knowing what documents are needed for a business line of credit for a rare book dealer is just the first step. Presenting those documents effectively can make a real difference in the outcome of your application.

- Work with a lender who understands specialty retail: Community banks, credit unions, and online lenders with experience in niche or arts-based businesses may be more receptive than large national banks with rigid underwriting criteria.

- Prepare a brief business overview: A one- to two-page summary of your dealership, how you source inventory, who your customers are, and how you price and sell books can go a long way in educating an underwriter unfamiliar with your trade.

- Maintain clean, organized records year-round: Lenders respond well to businesses that demonstrate financial discipline. Using accounting software like QuickBooks or Wave can make document preparation much faster.

- Consider a smaller initial credit line: Starting with a modest line of credit and using it responsibly can build your business credit profile, making future applications for larger amounts more successful.

- Speak with a business lending advisor: A knowledgeable advisor can help you identify the right lender, review your documents before submission, and flag any gaps that might slow down approval.

The rare book trade may be a niche market, but it's a legitimate and often profitable one. With the right preparation and documentation strategy, securing a business line of credit is a realistic goal.

●Conclusion

A business line of credit can give a rare book dealer the financial flexibility to seize inventory opportunities, manage seasonal cash flow, and grow with confidence. The key to a successful application lies in preparation. From core business registration documents and financial statements to tax returns, bank records, and inventory documentation, each piece of the file tells your lender a story about the health and credibility of your business.

If you're a rare book dealer exploring financing options, LoanWise is here to help. Our team understands the unique needs of specialty business borrowers and can guide you through the documentation process from start to finish. Reach out today to speak with a business lending advisor and take the first step toward securing the credit your dealership deserves.