Business Line of Credit Explained for Real Estate Investors

Real estate investing often requires quick access to capital for unexpected opportunities or expenses. A business line of credit explained simply is a flexible financing tool that provides investors with on-demand access to funds without the rigid structure of traditional loans. Unlike term loans that provide a lump sum upfront, a line of credit allows you to draw funds as needed and only pay interest on what you actually use.

For real estate investors managing multiple properties or pursuing fix and flip projects, this financing option can serve as a crucial bridge between deals, provide working capital for renovations, or cover carrying costs during extended holding periods. Understanding how these credit facilities work, their qualification requirements, and strategic applications can help investors make more informed financing decisions for their portfolios.

Common Questions About Business Lines of Credit

Many real estate investors have similar questions when considering business lines of credit for their investment strategies.

Q: How does a business line of credit differ from a traditional business loan?

A business line of credit provides revolving access to funds up to a predetermined limit, similar to a credit card but typically with lower interest rates. You can draw funds as needed and repay them, then access those funds again. Traditional business loans provide a lump sum that you repay in fixed installments over a set term.

Q: Can I use a business line of credit for real estate investments?

Many lenders allow business lines of credit to be used for working capital, inventory, equipment, and business expansion, which may include real estate investments depending on your business structure and the lender's policies.

Q: What happens if I don't use the full credit line?

You typically only pay interest on the amount you actually draw from the line of credit, not the entire available limit. Some lenders may charge small maintenance fees for unused portions.

Key Benefits for Real Estate Investors

Business lines of credit offer several advantages that align well with real estate investment strategies and cash flow patterns.

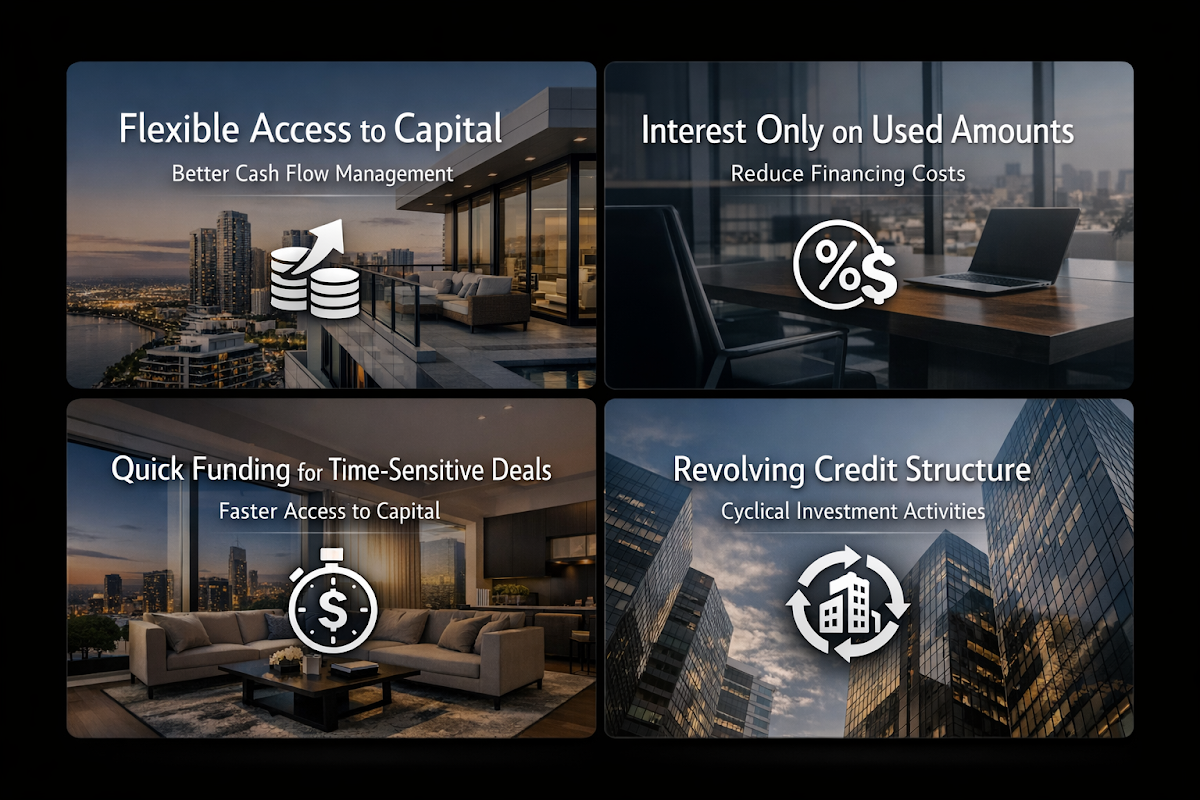

- Flexible Access to Capital: Draw funds only when needed for opportunities, renovations, or carrying costs, providing better cash flow management than fixed loan payments

- Interest Only on Used Amounts: Pay interest solely on drawn funds rather than the entire credit limit, potentially reducing overall financing costs during inactive periods

- Quick Funding for Time-Sensitive Deals: Once established, accessing funds from a line of credit can be much faster than applying for new loans, crucial for competitive real estate markets

- Revolving Credit Structure: Repay and redraw funds multiple times within the credit limit, making it suitable for cyclical investment activities like fix and flip projects

Typical Qualification Requirements

Business line of credit requirements vary among lenders, but real estate investors should generally prepare for these common qualification requirements.

- Business Operating History: Most lenders prefer businesses operating for at least 12-24 months, though some may consider newer entities with strong personal credit and experience

- Revenue and Cash Flow: Lenders typically review business income statements and bank statements to assess ability to service the credit line, often requiring minimum annual revenues

- Credit Score Standards: Both business and personal credit scores may be evaluated, with many lenders preferring personal scores above 650 and established business credit profiles

- Collateral or Personal Guarantees: Secured lines may require business assets or real estate as collateral, while unsecured options often require personal guarantees from business owners

Understanding Interest Rates and Costs

Business line of credit interest rates and associated costs can vary significantly based on multiple factors that investors should evaluate carefully.

- Variable Rate Structure: Many lines of credit feature variable interest rates tied to prime rate or other benchmarks, meaning rates can fluctuate over time

- Credit Score Impact: Higher personal and business credit scores typically qualify for lower interest rates, making credit improvement a valuable investment strategy

- Secured vs. Unsecured Pricing: Secured lines of credit backed by collateral often offer lower rates than unsecured options, but put assets at risk

- Additional Fees: Consider draw fees, annual fees, or maintenance charges that can affect the overall cost of the credit facility beyond the stated interest rate

Strategic Applications for Working Capital

Using a business line of credit for working capital can provide real estate investors with enhanced financial flexibility and operational efficiency.

- Bridge Financing Between Properties: Cover carrying costs, taxes, and maintenance while waiting for property sales or refinancing opportunities to close

- Renovation and Improvement Projects: Fund materials, contractor payments, and permits for fix and flip projects or rental property upgrades without depleting cash reserves

- Seasonal Cash Flow Management: Address seasonal variations in rental income or property management expenses, particularly for vacation rental or seasonal market investments

- Opportunity Fund for Quick Acquisitions: Maintain readily available capital for time-sensitive investment opportunities or distressed property purchases that require fast closing

- Emergency Repairs and Maintenance: Handle unexpected property expenses like HVAC failures, roof repairs, or other major maintenance issues without disrupting other investment plans

How to Get a Business Line of Credit

The application process for obtaining a business line of credit typically involves several key steps that real estate investors should prepare for in advance.

- Prepare Financial Documentation: Gather business tax returns, profit and loss statements, bank statements, and personal financial information to demonstrate creditworthiness and repayment ability

- Research and Compare Lenders: Evaluate options from traditional banks, credit unions, and alternative lenders, comparing rates, terms, and qualification requirements that fit your investment strategy

- Complete the Application Process: Submit detailed applications including business plans, use of funds statements, and any required collateral documentation for secured credit lines

- Undergo Credit Review and Approval: Allow time for lenders to review credit histories, verify income, and assess the overall risk profile of your real estate investment business

●Conclusion

A business line of credit explained in practical terms represents a valuable financing tool for real estate investors seeking flexible access to capital. The ability to draw funds as needed while paying interest only on used amounts can provide significant advantages for managing cash flow, seizing investment opportunities, and handling unexpected expenses.

Success with business lines of credit often depends on understanding the qualification requirements, comparing interest rates and terms among different lenders, and developing a clear strategy for how the credit facility will support your investment goals. Whether you're managing rental properties, pursuing fix and flip projects, or building a diversified real estate portfolio, the right line of credit can serve as a crucial component of your financing strategy.

At Trulo Mortgage, we understand that real estate investors need financing solutions that match their unique operational requirements and investment timelines. While traditional mortgage products remain essential for property acquisitions and refinancing, flexible credit facilities can complement these tools to create a more robust financial foundation for your real estate investment business.