When you're ready to buy a home or refinance your existing mortgage, understanding mortgage rates becomes crucial to making informed financial decisions. These rates don't just determine your monthly payment—they significantly impact your purchasing power, total loan costs, and long-term financial health. Whether you're a first-time homebuyer or an experienced real estate investor, grasping how mortgage rates work can save you thousands of dollars over the life of your loan and help you time your financing decisions more strategically.

What Are Mortgage Rates and How They're Determined

Mortgage rates represent the annual cost of borrowing money to purchase or refinance a home, expressed as a percentage of your loan amount. These rates fluctuate based on various economic factors, including Federal Reserve policies, inflation expectations, employment data, and overall market conditions.

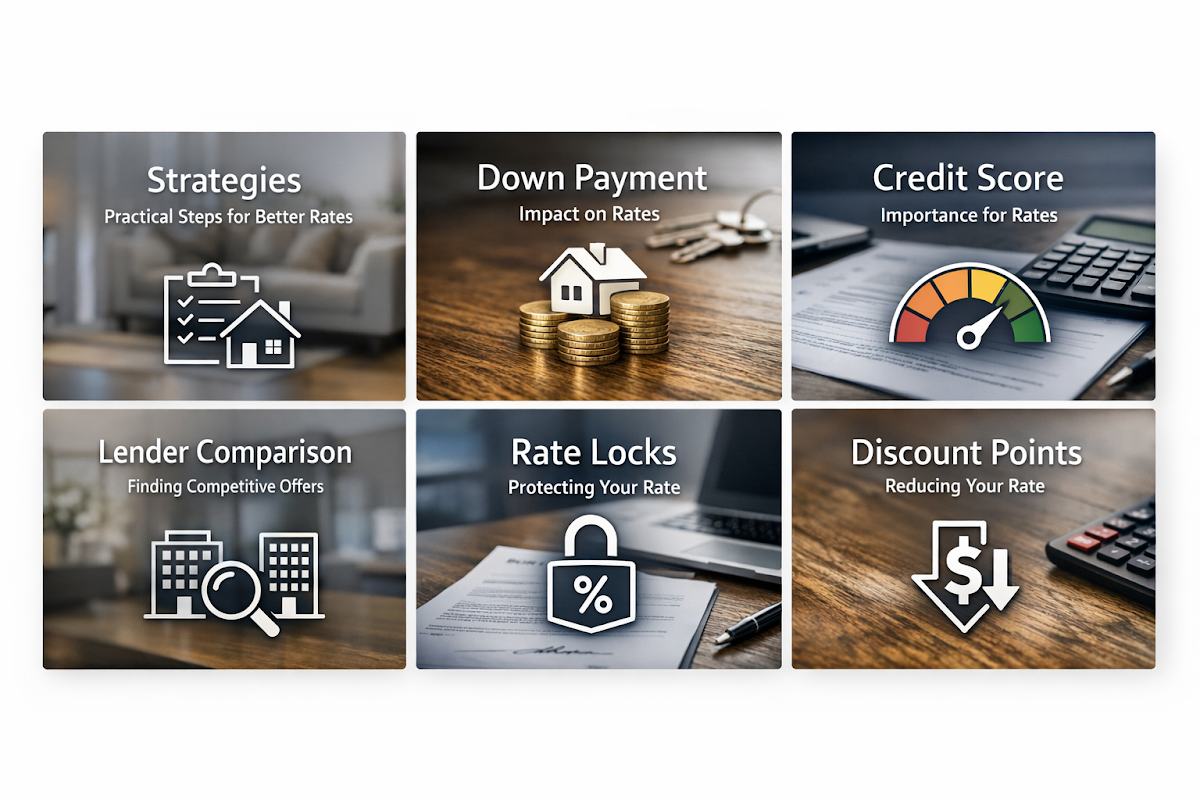

Lenders typically consider several personal factors when determining your specific rate. Your credit score plays a significant role—borrowers with higher scores often qualify for better rates because they represent lower risk to the lender. The size of your down payment also matters, as larger down payments typically result in more favorable rates since they reduce the lender's risk.

The type of loan you choose affects your rate as well. Conventional loans, FHA loans, VA loans, and USDA loans each have different rate structures and qualification requirements. Additionally, the length of your loan term impacts your rate, with shorter-term loans generally offering lower rates but higher monthly payments.

How Mortgage Rates Impact Your Monthly Payment and Buying Power

Even small changes in mortgage rates can significantly affect your monthly payment and how much home you can afford. For example, on a $300,000 loan, a one percentage point increase in your mortgage rate could add approximately $150-200 to your monthly payment, depending on the loan term.

This payment difference directly impacts your buying power. If you're pre-approved for a certain monthly payment amount, higher rates mean you'll qualify for a smaller loan amount. Conversely, when rates are lower, you might be able to afford a more expensive home while maintaining the same monthly payment.

Understanding this relationship helps you make strategic timing decisions. Some homebuyers choose to adjust their price range based on current rate environments, while others might decide to wait if rates are expected to decrease. However, it's important to remember that predicting rate movements can be challenging, and other factors like home prices and inventory should also influence your decision.

Fixed vs. Adjustable Rate Mortgages in Different Rate Environments

Choosing between fixed-rate and adjustable-rate mortgages (ARMs) becomes particularly important when considering current and future rate trends. Fixed-rate mortgages offer predictable payments throughout the loan term, providing stability and protection against rising rates.

Adjustable-rate mortgages typically start with lower initial rates that can change after a specified period. These loans might be attractive when rates are high, as they offer the potential for lower payments if rates decrease. However, they also carry the risk of payment increases if rates rise.

When evaluating ARMs, consider factors like how long you plan to stay in the home, your risk tolerance, and current rate trends. If you expect to move or refinance within the initial fixed period of an ARM, the lower initial rate might save you money. However, if you plan to stay long-term and value payment predictability, a fixed-rate mortgage might be more suitable.

Strategies to Secure Better Mortgage Rates

Several practical steps can help you qualify for better mortgage rates. Start by checking and improving your credit score well before applying for a loan. Even small improvements can result in rate reductions that save significant money over time.

Consider making a larger down payment if possible. While not everyone can put down 20%, increasing your down payment from 5% to 10% or from 10% to 15% might help you secure a better rate. Additionally, some loan programs offer rate improvements for larger down payments.

Shopping around with multiple lenders is crucial, as rates and fees can vary significantly between institutions. Don't just compare rates—look at annual percentage rates (APRs) which include both the interest rate and associated fees. Getting quotes from different types of lenders, including banks, credit unions, and mortgage brokers, can help you find the most competitive offer.

Consider paying discount points if you plan to stay in the home long enough to recoup the upfront cost through lower monthly payments. Each point typically costs 1% of your loan amount and reduces your rate by about 0.25%, though this can vary by lender and market conditions.

Rate Lock Strategies and Timing Your Application

Once you find a favorable rate, protecting it through a rate lock becomes important. Most lenders offer rate locks for 30 to 60 days, with some extending to 90 days or longer for a fee. This protection ensures your rate won't increase while your loan is being processed, even if market rates rise.

Timing your rate lock strategically can save money and reduce stress. Lock your rate when you have a signed purchase contract and are confident the loan will close within the lock period. If you're refinancing, you have more flexibility in timing since you're not dependent on a purchase transaction.

Be aware that rate locks typically can't be improved if rates drop after you've locked, though some lenders offer float-down options for an additional fee. If rates decrease significantly after you've locked, you might consider whether paying for a float-down or starting over with a new application makes financial sense.

Understanding the Total Cost Impact Beyond Monthly Payments

While monthly payments are important, mortgage rates affect your total loan cost over the entire term. A seemingly small rate difference can result in tens of thousands of dollars in additional interest payments over a 30-year loan.

Consider both the immediate impact on your monthly budget and the long-term financial implications. Higher rates mean more of your payment goes toward interest rather than principal, slowing your equity building. This affects your net worth growth and the financial benefit you receive from homeownership.

For investment properties, mortgage rates directly impact your cash flow and return on investment. Higher rates reduce your profit margins and might affect which properties make financial sense to purchase. Understanding these broader implications helps you make more informed decisions about your real estate investments and overall financial strategy.

Market Trends and Future Rate Considerations

While predicting exact rate movements is impossible, understanding broader economic trends can inform your financing decisions. Mortgage rates often correlate with economic indicators like employment rates, inflation, and Federal Reserve policies, though the relationship isn't always direct or immediate.

Stay informed about economic conditions, but avoid trying to perfectly time the market. Rates can change quickly, and other factors like home prices, inventory levels, and your personal financial situation are equally important. Focus on finding a rate and payment you're comfortable with based on current conditions rather than waiting for perfect timing.

Consider your personal timeline and goals when evaluating rate environments. If you need to buy a home due to family changes, job relocation, or other life circumstances, the current rate environment becomes less relevant than finding financing that works for your situation. Remember that you can often refinance later if rates improve significantly.

●Conclusion

Understanding mortgage rates empowers you to make better financing decisions and potentially save thousands of dollars over your loan's lifetime. While rates are just one factor in your home financing journey, their impact on your monthly payments, buying power, and total costs makes them worthy of careful consideration. Focus on improving your credit profile, shopping with multiple lenders, and choosing loan terms that align with your long-term goals. Remember that the best mortgage rate is one that fits your financial situation and helps you achieve your homeownership objectives while maintaining overall financial stability.