When you need access to significant funds for home improvements, debt consolidation, or major expenses, your home's equity might provide the solution you're looking for. Two popular options stand out: a home equity line of credit (HELOC) and a traditional home equity loan. Understanding the differences between these financing methods can help you make an informed decision that aligns with your financial goals and circumstances.

Understanding Home Equity Financing Basics

Home equity represents the difference between your property's current market value and the outstanding balance on your mortgage. This equity can serve as collateral for additional borrowing, allowing homeowners to access funds at typically lower interest rates than unsecured loans or credit cards.

Both home equity lines of credit and home equity loans tap into this valuable resource, but they function quite differently. The choice between them often depends on your specific financial needs, spending patterns, and comfort level with variable interest rates.

Most lenders allow you to borrow up to 80% of your home's value, minus any existing mortgage debt. This means if your home is worth $300,000 and you owe $200,000 on your mortgage, you might qualify for up to $40,000 in home equity financing.

How Home Equity Lines of Credit Work

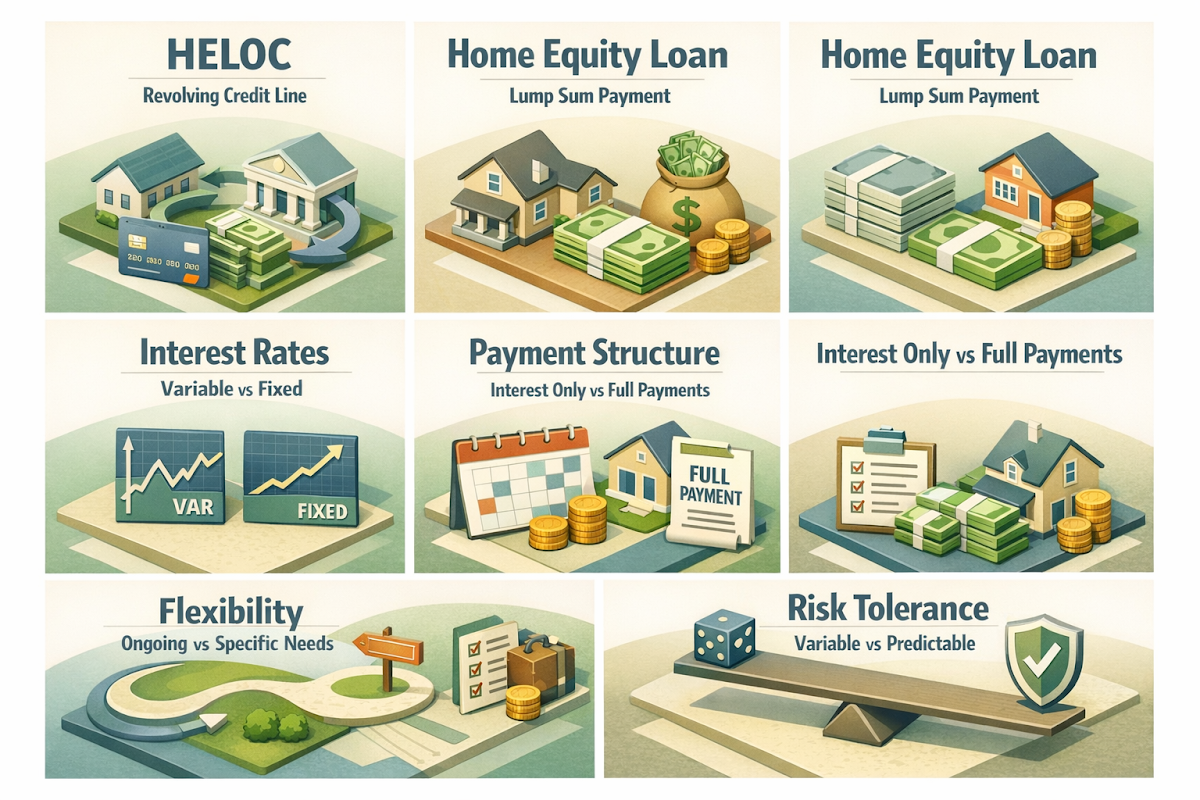

A home equity line of credit functions similarly to a credit card, providing you with a revolving credit line that you can draw from as needed. During the initial draw period, which typically lasts 5-10 years, you can access funds up to your credit limit and may only be required to make interest payments.

HELOCs usually feature variable interest rates that fluctuate with market conditions. This flexibility can work in your favor when rates are falling, but it also means your payments could increase if rates rise. The variable nature of these rates makes budgeting somewhat more challenging compared to fixed-rate options.

After the draw period ends, the repayment period begins, usually lasting 10-20 years. During this phase, you can no longer access additional funds and must begin paying both principal and interest on the outstanding balance. This transition often results in significantly higher monthly payments.

Traditional Home Equity Loan Structure

A home equity loan, sometimes called a second mortgage, provides you with a lump sum of money upfront at a fixed interest rate. You'll begin making regular monthly payments immediately, covering both principal and interest over a predetermined term, typically 5-30 years.

The fixed interest rate offers predictability, making it easier to budget for monthly payments throughout the life of the loan. This stability can be particularly valuable in uncertain economic times or when interest rates are expected to rise.

Since you receive all the funds at closing, home equity loans work best when you know exactly how much money you need and when you'll need it. This makes them ideal for specific projects like home renovations, debt consolidation, or major expenses with known costs.

Comparing Interest Rates and Payment Structures

Interest rate differences between HELOCs and home equity loans can significantly impact your overall borrowing costs. Home equity loans typically start with slightly higher rates than initial HELOC rates, but they provide rate certainty throughout the loan term.

HELOC rates often begin lower than home equity loan rates, but their variable nature means they could increase substantially over time. During periods of rising interest rates, HELOC borrowers might find their payments becoming uncomfortably high, especially during the repayment period.

Payment structures also differ considerably. With a HELOC, you might pay only interest during the draw period, keeping payments relatively low initially. However, home equity loans require full principal and interest payments from the start, which might strain your budget initially but builds equity more quickly.

Choosing the Right Option for Your Needs

Your specific financial situation and intended use of funds should guide your choice between these options. HELOCs work well for ongoing expenses like home renovation projects that occur in phases, educational expenses spread over several years, or as an emergency fund for unexpected costs.

Home equity loans suit situations where you need a specific amount upfront, such as debt consolidation, major home improvements with fixed costs, or large purchases. The predictable payment structure makes them ideal for borrowers who prefer consistent monthly obligations.

Consider your risk tolerance regarding interest rate changes. If you're comfortable with potential payment fluctuations and want flexibility in accessing funds, a HELOC might suit you better. If you prefer predictable payments and know your exact borrowing needs, a home equity loan could be the wiser choice.

Application Process and Qualification Requirements

Both financing options typically require similar qualification criteria, including good credit scores, stable income, and sufficient home equity. Lenders generally prefer credit scores of 680 or higher, though some may work with lower scores under certain circumstances.

The application process involves property appraisals, income verification, and credit checks. HELOCs might have slightly more flexible qualification requirements since lenders can adjust credit limits based on your financial profile, while home equity loans require approval for the full requested amount upfront.

Processing times are usually comparable, taking 30-45 days from application to closing. However, once approved, HELOCs provide immediate access to funds during the draw period, while home equity loans disburse the entire amount at closing.

Tax Implications and Financial Planning

Recent tax law changes have modified the deductibility of home equity debt interest. Generally, interest may be deductible if you use the funds to buy, build, or substantially improve your home. However, interest on funds used for other purposes, such as debt consolidation or personal expenses, might not qualify for tax deductions.

Both options should fit into your broader financial planning strategy. Consider how the additional debt payments will affect your monthly budget, emergency fund, and other financial goals. The secured nature of these loans means your home serves as collateral, making timely payments crucial to avoid foreclosure risk.

Working with a qualified tax professional can help you understand the specific implications for your situation and ensure you're maximizing any available tax benefits while making responsible borrowing decisions.

●Conclusion

Choosing between a home equity line of credit and a home equity loan requires careful consideration of your financial needs, risk tolerance, and long-term plans. HELOCs offer flexibility and potentially lower initial costs, while home equity loans provide predictability and fixed payments. Both options can be valuable tools for accessing your home's equity, but the right choice depends on your unique circumstances. Consider consulting with a qualified loan officer who can help you evaluate your options and make the decision that best supports your financial goals.