Mortgage Refinance to Lower Rate: Your Path to Enhanced Investment Returns

Real estate investors in 2026 are witnessing a significant shift in refinancing opportunities. With DSCR loan rates dropping from the previous 8-9% range to approximately 5.875% to 7.375%, the landscape for mortgage refinance to lower rate strategies has become increasingly favorable. This decline presents a strategic window for investors to optimize their rental property portfolios and enhance cash flow through intelligent refinancing decisions.

The current market conditions offer unique advantages for investors who understand how to leverage these lower rates effectively. Unlike traditional mortgage products focused on personal financial credentials, DSCR loans prioritize the income-generating potential of your properties, making them an ideal vehicle for refinancing strategies that maximize investment returns.

Current Market Opportunities for Lower Rate Refinancing

The refinancing landscape in 2026 presents compelling opportunities for investors seeking to reduce their mortgage costs. Current market opportunities for lower rates refinancing have expanded significantly, driven by evolving lending criteria and competitive rate structures.

- DSCR Rate Improvements: Interest rates for qualified borrowers now range from 5.875% to 7.375%, representing substantial savings compared to previous years when rates typically exceeded 8-9%

- Portfolio-Based Qualification: Lenders increasingly focus on property income rather than personal financial metrics, enabling investors to refinance multiple properties based on rental income performance

- Enhanced Cash Flow Potential: Lower rates translate directly to improved monthly cash flow, allowing investors to reinvest savings into additional properties or property improvements

- Flexible Refinancing Terms: Modern DSCR loan products offer various term lengths and payment structures designed specifically for investment property portfolios

Benefits of Refinancing for Lower Rate Investment Properties

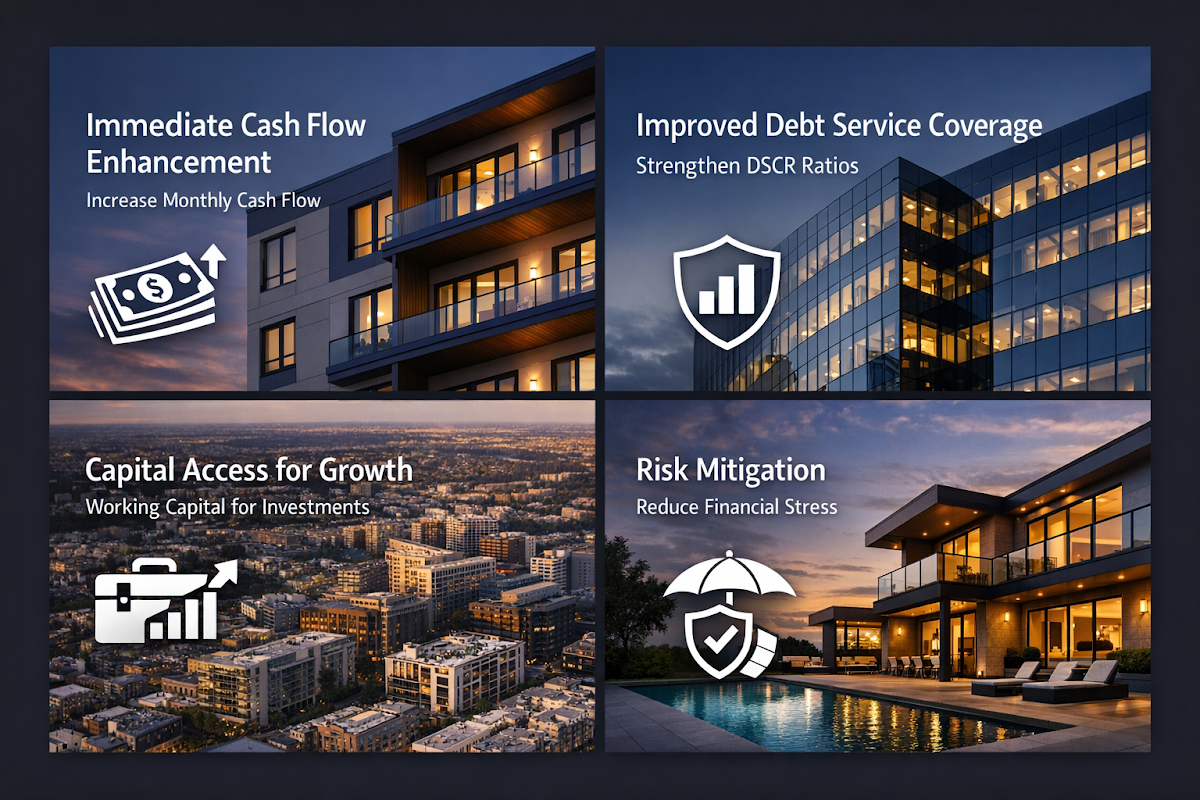

Understanding the benefits of refinancing for lower rate investment properties extends beyond simple monthly payment reductions. These advantages can significantly impact your overall investment strategy and portfolio growth potential.

- Immediate Cash Flow Enhancement: Reducing your interest rate by even 1-2% can increase monthly cash flow by hundreds of dollars per property, compounding across your entire portfolio

- Improved Debt Service Coverage: Lower payments strengthen your DSCR ratios, potentially qualifying you for better terms on future acquisitions and creating a positive cycle of portfolio expansion

- Capital Access for Growth: Enhanced cash flow provides working capital for property improvements, maintenance reserves, or down payments on additional investment properties

- Risk Mitigation: Lower monthly obligations reduce financial stress during vacancy periods or unexpected maintenance costs, providing greater investment stability

DSCR Loan Refinancing Strategies

DSCR loan refinancing strategies offer unique advantages for real estate investors who want to optimize their financing structure. These approaches focus on property performance rather than personal income documentation, creating opportunities that traditional refinancing might not provide.

- Income-First Qualification: DSCR loans evaluate your property's rental income against mortgage payments, typically requiring a ratio of 1.0 or higher, allowing investors with complex personal finances to qualify based on property performance alone

- Portfolio Consolidation Options: Some lenders offer blanket loan refinancing, enabling you to consolidate multiple properties under single loan terms, potentially reducing overall interest rates and simplifying management

- No Income Documentation Required: These loans eliminate the need for tax returns, W-2s, or employment verification, streamlining the refinancing process for self-employed investors or those with multiple income streams

- Strategic Timing Opportunities: Current market conditions with lower DSCR rates create windows for refinancing that might improve cash flow while maintaining or enhancing your investment leverage

Mortgage Rate Comparison for Refinance Evaluation

Effective mortgage rate comparison for refinance evaluation requires understanding multiple factors beyond the advertised interest rate. Investors must evaluate the total cost structure and terms to make informed refinancing decisions.

- Rate Structure Analysis: Compare fixed versus adjustable rate options, considering your holding period and market outlook, as some investors benefit from short-term adjustable rates when planning property dispositions

- Total Cost Evaluation: Factor in origination fees, appraisal costs, title insurance, and other closing expenses to determine the true cost of refinancing and break-even timeline

- Lender-Specific Terms: Different mortgage lenders may offer varying prepayment penalties, seasoning requirements, or portfolio size limitations that could impact your refinancing strategy

- Market Timing Considerations: Monitor rate trends and lock-in opportunities, as DSCR loan rates may fluctuate based on investor demand and secondary market conditions

Maximizing Savings Through Strategic Refinancing

Strategic refinancing approaches can significantly amplify your investment returns when implemented thoughtfully. These numbered strategies help maximize savings through systematic evaluation and execution of your refinancing decisions.

- Calculate True Break-Even Points: Determine how long it will take for monthly savings to offset refinancing costs, typically 18-36 months for investment properties, and ensure this aligns with your property holding strategy

- Optimize Property Performance First: Improve rental income through strategic upgrades or rent increases before refinancing, as higher income can qualify you for better DSCR loan terms and lower rates

- Bundle Portfolio Refinancing: Consider refinancing multiple properties simultaneously to negotiate better rates and terms, as lenders often provide volume discounts for larger loan packages

- Time Market Cycles Strategically: Plan refinancing during periods of rate stability or decline, while avoiding peak refinancing seasons when lender capacity might be constrained and processing times extended

- Maintain Relationship Banking: Work with lenders who understand real estate investment and can provide ongoing portfolio support, as these relationships often yield better rates and terms over time

●Conclusion

The current market environment presents exceptional opportunities for real estate investors to implement mortgage refinance to lower rate strategies. With DSCR loan rates significantly below previous levels, investors who act strategically can enhance their portfolio performance while positioning for future growth.

Success in refinancing requires careful evaluation of your entire portfolio, understanding the true costs and benefits of each opportunity, and working with lenders who specialize in investment property financing. The combination of improved rates and flexible DSCR loan structures creates a powerful foundation for optimizing your real estate investment returns.

As market conditions continue to evolve, staying informed about refinancing opportunities and maintaining relationships with experienced investment property lenders will be crucial for maximizing your portfolio's potential. The investors who take advantage of these favorable conditions today will likely see compounding benefits in their cash flow and overall investment performance for years to come.