Rental arbitrage has become an increasingly popular business model for entrepreneurs who want to profit from short-term rentals without owning property outright. The strategy involves leasing a property long-term and then subletting it on platforms like Airbnb or Vrbo at a higher nightly rate. But getting started — or scaling — often requires startup capital, and that's where a Home Equity Line of Credit, or HELOC, can come into play. For homeowners who've built meaningful equity in their primary residence, tapping into that equity could provide the flexible funding needed to launch or grow a rental arbitrage operation. However, understanding HELOC requirements for a rental arbitrage business is essential before you apply. Lenders have specific standards, and using the funds for a business purpose adds a layer of complexity that borrowers should be well-prepared for.

What Is a HELOC and How Does It Work for Investors

A home equity Line of Credit is a revolving credit product secured by the equity in your home. Think of it like a credit card, but with your property as collateral. Lenders typically allow homeowners to borrow against a portion of their available equity — often up to 80% to 85% of the home's appraised value, minus any outstanding mortgage balance. This is commonly referred to as the combined loan-to-value, or CLTV, ratio.

What makes a HELOC especially appealing for rental arbitrage business entrepreneurs is its flexibility. During the draw period — which typically lasts around 10 years — you can borrow, repay, and borrow again as needed. This revolving access to capital is well-suited for covering upfront costs like furniture purchases, security deposits on leased properties, platform listing fees, and operational expenses tied to launching new rental units.

Interest is generally only charged on the amount you draw, not the full credit line, which may help keep borrowing costs manageable during slower business periods. After the draw period ends, most HELOCs enter a repayment phase where both principal and interest become due. Understanding this structure is important for cash flow planning, especially when your rental income may fluctuate seasonally.

Core HELOC Eligibility Standards Lenders Typically Evaluate

Before approving a HELOC, lenders will review several key financial factors. While specific requirements can vary by institution, there are common benchmarks that most lenders use to assess risk and creditworthiness.

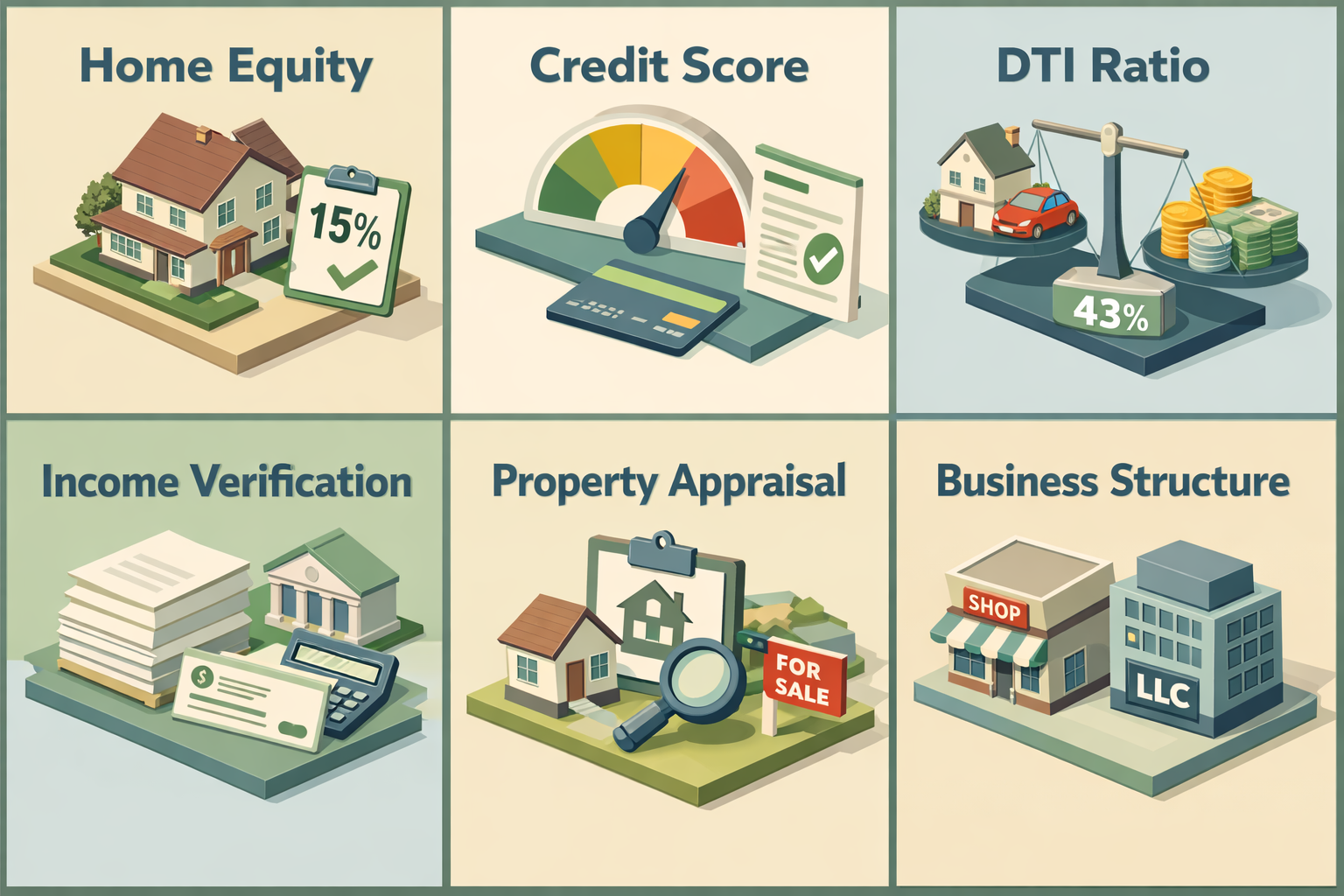

- Home equity: You'll generally need at least 15% to 20% equity in your home after the HELOC is factored in. The more equity you have, the more favorable your credit terms may be.

- Credit score: Most lenders look for a minimum score in the mid-600s, though borrowers with scores in the 700s or higher are likely to receive better interest rates and higher credit limits.

- Debt-to-income ratio (DTI): Lenders typically want your total monthly debt obligations — including the potential HELOC payment — to stay within a certain percentage of your gross monthly income. A DTI below 43% is often cited as a general threshold, though some lenders may be more flexible.

- Income verification: Stable, documented income is important. For rental arbitrage entrepreneurs who may be self-employed or operating as an LLC, income documentation requirements could be more involved.

- Property appraisal: Lenders will typically require a current appraisal or automated valuation to confirm your home's market value before extending a credit line.

If you're already running a rental arbitrage business and reporting that income on your taxes, some lenders may consider it in your qualifying income — but policies on this can vary significantly, so it's worth discussing directly with a loan officer.

How Your Business Structure Could Affect HELOC Approval

One important nuance when it comes to understanding HELOC requirements for a rental arbitrage business is how your business structure might influence the approval process. Many rental arbitrage operators register as a sole proprietor or form a Limited Liability Company (LLC) to protect personal assets and streamline tax reporting.

If you're applying for a personal HELOC on your primary residence, the loan is technically in your name — not your business entity. However, lenders will still want to understand how the funds will be used, particularly if your rental arbitrage income is part of your qualifying profile. Self-employed borrowers and business owners may face additional scrutiny, including requests for two years of tax returns, profit and loss statements, or business bank statements.

It's also worth noting that some lenders may view rental arbitrage income with caution, since it often depends on third-party platforms and can fluctuate based on occupancy, platform policies, and local regulations. Being prepared with thorough documentation — including platform earnings summaries and lease agreements — may strengthen your application and help demonstrate business stability to a skeptical underwriter.

Using HELOC Funds Strategically in a HELOC for Rental Property Business

Once you've secured a HELOC for rental property business purposes, how you deploy those funds can make a significant difference in your return on investment. Rental arbitrage has relatively low barriers to entry compared to property ownership, but the upfront costs can still add up quickly when you're furnishing and equipping multiple units.

Here are some common ways rental arbitrage operators might use HELOC funds strategically:

- Security deposits and first/last month's rent: Leasing a furnished or unfurnished property often requires substantial upfront payments before you can generate a single dollar in rental income.

- Furnishing and staging units: Guests on short-term rental platforms expect a well-appointed space. Quality furniture, bedding, kitchen equipment, and décor are essential investments in your listing's performance.

- Marketing and photography: Professional listing photos and paid promotion can meaningfully improve your occupancy rates and nightly pricing power.

- Scaling into new markets: Once your first unit is cash-flowing, a HELOC's revolving structure lets you draw additional funds to expand into new properties or cities without reapplying for credit.

It's important to keep detailed records of how HELOC funds are used, both for tax purposes and to ensure your business remains financially organized as it grows. Mixing personal and business expenses without clear documentation can create complications at tax time.

Risks and Considerations Every Homeowner Borrower Should Weigh

While a HELOC can be a powerful financing tool, it comes with meaningful risks — especially when the borrowed funds are being used to support a business with variable income. Since your home serves as collateral, failure to repay could ultimately put your property at risk. That's a serious consideration that deserves careful thought before you proceed.

Here are some key risk factors to evaluate:

- Variable interest rates: Most HELOCs carry variable rates tied to an index like the prime rate. If interest rates rise, your borrowing costs will increase, which could squeeze margins in your rental arbitrage business.

- Occupancy volatility: Short-term rental income can be unpredictable. Seasonal demand, platform algorithm changes, or local regulatory shifts — such as new short-term rental ordinances — could reduce your revenue unexpectedly.

- Personal liability: Even if your rental business operates under an LLC, the HELOC is secured by your personal residence. Business struggles don't insulate your home from the consequences of default.

- Draw period end risk: When the draw period closes, your monthly payments may increase substantially as principal repayment begins. Business owners should plan for this transition proactively.

Consulting with both a financial advisor and a tax professional before using home equity to fund a business is generally a wise step. They can help you model out realistic cash flow scenarios and assess whether the return on investment justifies the risk to your most valuable personal asset.

How to Strengthen Your Application Before Applying

If you're planning to apply for a HELOC to fund your rental arbitrage venture, taking steps to improve your application profile beforehand may improve your chances of approval and help you secure more favorable terms.

Consider the following preparation strategies:

- Build your credit score: Pay down revolving balances and resolve any outstanding negative items on your credit report. Even a modest improvement in your score could make a meaningful difference in your interest rate offer.

- Reduce existing debt: Lowering your DTI ratio before applying can make you a more attractive borrower, particularly if you carry auto loans, student debt, or other obligations.

- Document your rental income: If you're already earning income from rental arbitrage, organize your platform statements, 1099 forms, and tax returns to present a clear picture of business performance.

- Get a home appraisal estimate: Understanding your home's current market value can help you estimate how much equity you have available and whether a HELOC is a realistic option at this time.

- Shop multiple lenders: HELOC terms, rates, and requirements can vary considerably between banks, credit unions, and online lenders. Comparing multiple offers gives you leverage and helps ensure you're not leaving money on the table.

Working with a mortgage professional who has experience with self-employed borrowers or real estate investors may also be beneficial. They can guide you through lender-specific nuances and help you position your application as strongly as possible.

●Conclusion

For homeowners with sufficient equity and a clear business plan, a HELOC can be a smart and flexible way to fund a rental arbitrage operation. But understanding HELOC requirements for a rental arbitrage business goes beyond simply knowing your credit score. It means preparing for income documentation challenges, anticipating lender scrutiny around business use of funds, and carefully weighing the risks of pledging your home as collateral for a variable-income venture. When approached with thorough preparation and sound financial planning, home equity financing could serve as a meaningful catalyst for rental arbitrage growth. If you're ready to explore your options, connecting with an experienced mortgage professional at LoanWise is a great first step toward understanding what's possible for your specific situation.