For many small business owners and entrepreneurs, getting access to capital can feel like an uphill battle. Traditional bank loans often come with strict requirements that newer or smaller businesses simply can't meet. That's where SBA Microloans come in. Designed to help startups, early-stage businesses, and underserved entrepreneurs, SBA Microloans may offer a practical path to the funding needed to grow. In this article, we'll break down everything you need to know about this lending program — from how it works to who it's designed for and how to get started.

What Are SBA Microloans and How Do They Work?

The SBA Microloan program is administered by the U.S. Small Business Administration and provides small, short-term loans to eligible small businesses and nonprofit childcare centers. Unlike conventional bank loans, SBA Microloans are not issued directly by the SBA. Instead, the SBA provides funds to specially designated nonprofit intermediary lenders, who in turn issue loans to qualifying borrowers.

These intermediary lenders are typically community-based organizations with experience in lending and business development. Because they work closely with local entrepreneurs, they often have a deeper understanding of the challenges small business owners face — which can make the approval process more accessible and flexible than what you'd find at a traditional bank.

Loan amounts under this program can go up to $50,000, though the average loan tends to be significantly smaller. Repayment terms may vary depending on the lender and the specific use of the funds, but terms generally do not exceed six years. Interest rates can vary as well, and they're typically influenced by the intermediary lender's costs and the needs of the borrower.

Who Can Benefit from the SBA Microloan Program?

SBA Microloans are primarily designed for small business owners, startups, and entrepreneurs who may not yet qualify for larger conventional financing. This program tends to be especially helpful for:

- New business owners who haven't yet established a long credit or revenue history

- Women-owned businesses looking for accessible funding options

- Minority entrepreneurs who may face additional barriers in traditional lending markets

- Low-income entrepreneurs operating in underserved communities

- Nonprofit childcare centers seeking operational or expansion funding

If you're just getting your business off the ground or you've faced difficulty qualifying for conventional loans, this program could be a strong option to explore. That said, each intermediary lender sets its own eligibility criteria, so requirements may vary from one organization to the next. It's worth reaching out to multiple lenders in your area to compare what each one offers.

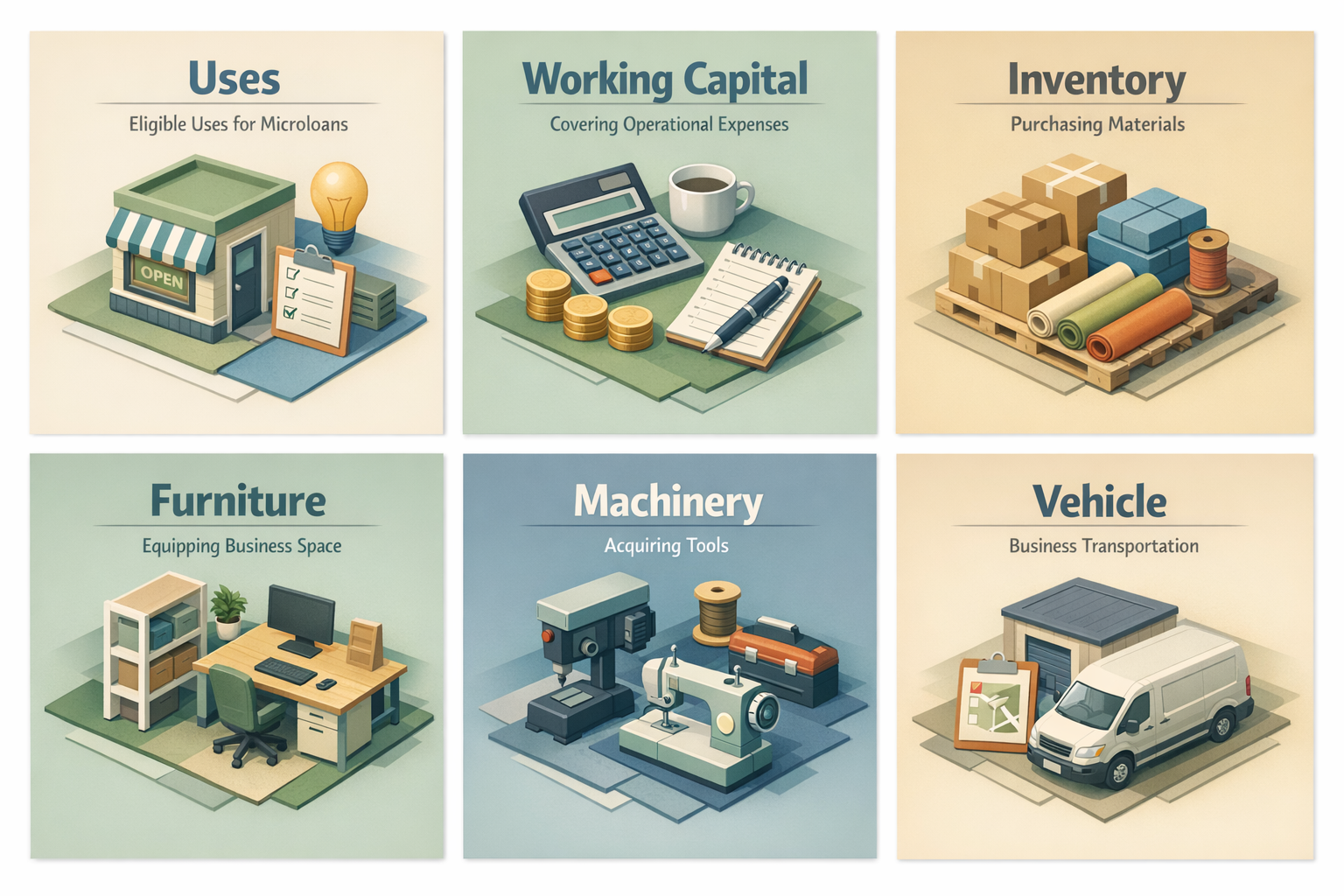

Approved Uses for Microloan Funds

One important thing to understand about SBA Microloans is that there are specific guidelines around how the funds can be used. Knowing these approved uses upfront can help you plan your application and ensure the loan aligns with your business needs.

Eligible uses for microloan funds typically include:

- Working capital — covering day-to-day operational expenses such as payroll, rent, or utilities

- Inventory or supplies — purchasing the materials needed to fulfill orders or stock shelves

- Furniture and fixtures — equipping your business space with the essentials

- Machinery and equipment — acquiring tools or technology needed to operate

It's important to note that SBA Microloan funds generally cannot be used to pay off existing debt or purchase real estate. If either of those is your primary goal, you may want to explore other SBA loan programs, such as the SBA 7(a) or SBA 504 loan, which may better fit your financing needs.

Understanding the Application and Approval Process

Applying for an SBA Microloan is a bit different from applying for a traditional business loan. Because the loans are issued through nonprofit intermediary lenders, the process may feel more personal and community-focused. Here's what you can generally expect:

Finding an Intermediary Lender

Your first step is to identify an SBA-approved intermediary lender in your region. The SBA provides a searchable directory of participating lenders, which makes this step more straightforward. Each lender operates independently, so their processes and documentation requirements may differ.

Preparing Your Application Materials

Most intermediary lenders will ask for a combination of the following:

- A completed business plan

- Personal and business financial statements

- Information about how you intend to use the loan funds

- Details about your business's history and structure

- Personal background and credit information

Business Training and Technical Assistance

One distinctive feature of the SBA Microloan program is that many intermediary lenders require borrowers to complete business training or technical assistance as part of the loan process. This requirement is designed to support long-term business success, not just provide a short-term cash infusion. Many borrowers find this added support genuinely helpful in building a stronger business foundation.

Key Advantages of SBA Microloans for Entrepreneurs

There are several compelling reasons why small business owners and entrepreneurs might consider SBA Microloans as part of their financing strategy. Let's take a closer look at what makes this program stand out:

- Accessible to newer businesses: Unlike many conventional loans that require years of operating history, SBA Microloans may be available to startups and businesses with limited track records.

- Community-focused lending: Because intermediary lenders are typically nonprofit organizations, they often prioritize the well-being of local entrepreneurs and may offer more flexible underwriting.

- Included business support: The technical assistance and training component can add real value, especially for first-time business owners who are still learning the ropes of running a company.

- Reasonable loan sizes: With loans up to $50,000, this program is well-suited for businesses that need modest capital — not a massive infusion of funds that comes with higher debt obligations.

- Credit-building opportunity: Successfully repaying a microloan can help establish or improve your business credit profile, making it easier to qualify for larger financing down the road.

Of course, no single loan product is right for every situation. It's always a good idea to compare your options and consult with a financial advisor or lending professional before committing to any financing arrangement.

Potential Limitations to Keep in Mind

While SBA Microloans offer meaningful benefits, it's equally important to understand their limitations before applying. Being informed helps you set realistic expectations and make the best decision for your business.

- Lower maximum loan amounts: If your business needs more than $50,000, you'll likely need to explore other loan programs or combine multiple funding sources.

- Restricted use of funds: As mentioned, you cannot use microloan proceeds to repay existing debt or purchase real estate, which limits the program's versatility.

- Collateral may be required: Some intermediary lenders may require collateral or a personal guarantee, which could be a concern for newer business owners with limited assets.

- Availability varies by location: Not every region has an equally robust network of intermediary lenders, so access to this program may be more limited depending on where your business is located.

- Training requirements: While the business training component can be beneficial, it does add time to the process, which may not be ideal if you need funding quickly.

Understanding these factors upfront can help you plan more effectively and determine whether an SBA Microloan is the right fit — or whether another financing option might serve you better.

●Conclusion

SBA Microloans represent a thoughtful and community-driven approach to small business financing. For entrepreneurs who are just starting out, operating in underserved markets, or simply unable to meet the requirements of traditional lending, this program could open doors that might otherwise stay closed. The combination of accessible loan amounts, flexible underwriting through nonprofit lenders, and included business support makes it a genuinely valuable resource worth exploring.

That said, like any financial product, it's important to do your research, compare your options, and work with a knowledgeable lending professional who can help guide you through the process. At LoanWise, we're here to help small business owners and entrepreneurs find the financing solutions that fit their goals. Reach out today to learn how we can help you take the next step toward growing your business.