Running a beekeeping operation as a freelance professional is deeply rewarding — but it comes with real financial pressures. From buying new hives and protective equipment to managing seasonal cash flow gaps, the costs can add up quickly. That's where a business line of credit can make a meaningful difference. Unlike a traditional term loan, a line of credit gives you flexible, revolving access to funds you can draw on when you need them and repay as your income allows. But qualifying isn't always straightforward, especially for agricultural freelancers. Understanding the requirements for a business line of credit for a freelance beekeeper is the first step toward securing the financing your apiary needs to grow.

Why Freelance Beekeepers Often Need Revolving Credit

Beekeeping is a seasonal business. Honey harvests, pollination contracts, and beeswax product sales tend to fluctuate significantly throughout the year. During peak seasons, revenue may be strong — but in the off-season, expenses like hive maintenance, winter feeding, equipment repairs, and colony replacements don't stop. This creates a cash flow gap that many freelance beekeepers struggle to bridge with savings alone.

A business line of credit is designed specifically to handle these kinds of short-term working capital needs. Rather than borrowing a lump sum and paying interest on the full amount, you draw only what you need, when you need it. This makes it an especially practical tool for working capital for agricultural freelancers who operate on unpredictable income cycles.

Beyond seasonal gaps, freelance beekeepers may also need credit to:

- Purchase new colonies or nucleus hives to expand their operation

- Buy bulk quantities of jars, labels, or packaging for honey products

- Cover veterinary or treatment costs during a disease outbreak

- Fund marketing and e-commerce setup for direct-to-consumer sales

- Bridge the gap while waiting on pollination service contracts to pay out

A revolving line of credit can address all of these scenarios without requiring a new loan application each time a need arises. That kind of financial flexibility is often critical for small-scale agricultural entrepreneurs.

How Lenders View Freelance Beekeeping as a Business

One of the first hurdles freelance beekeepers face is convincing a lender that their operation qualifies as a legitimate business. Lenders want to see that you're running a structured, documented enterprise — not just a hobby. The good news is that even small-scale apiary operations can qualify as businesses in the eyes of lenders, provided you've taken the right steps to establish your business identity.

Lenders will typically look for evidence that your beekeeping work generates consistent revenue and that it's operated with a degree of professionalism. This may include:

- A registered business name or legal entity (such as an LLC or sole proprietorship)

- A dedicated business bank account separate from personal finances

- A federal Employer Identification Number (EIN) or use of your Social Security Number for sole proprietors

- Business licenses or agricultural permits required in your state or county

- A track record of documented income from honey sales, pollination services, or related products

If your beekeeping operation is newer or hasn't yet generated significant revenue, lenders may place greater weight on your personal credit history and financial standing. Establishing your business formally before applying can strengthen your case considerably.

Core Requirements for a Business Line of Credit for a Freelance Beekeeper

Meeting the requirements for a business line of credit for a freelance beekeeper involves satisfying several key criteria that lenders use to assess risk. While exact standards vary by lender and loan product, most will evaluate the following areas closely.

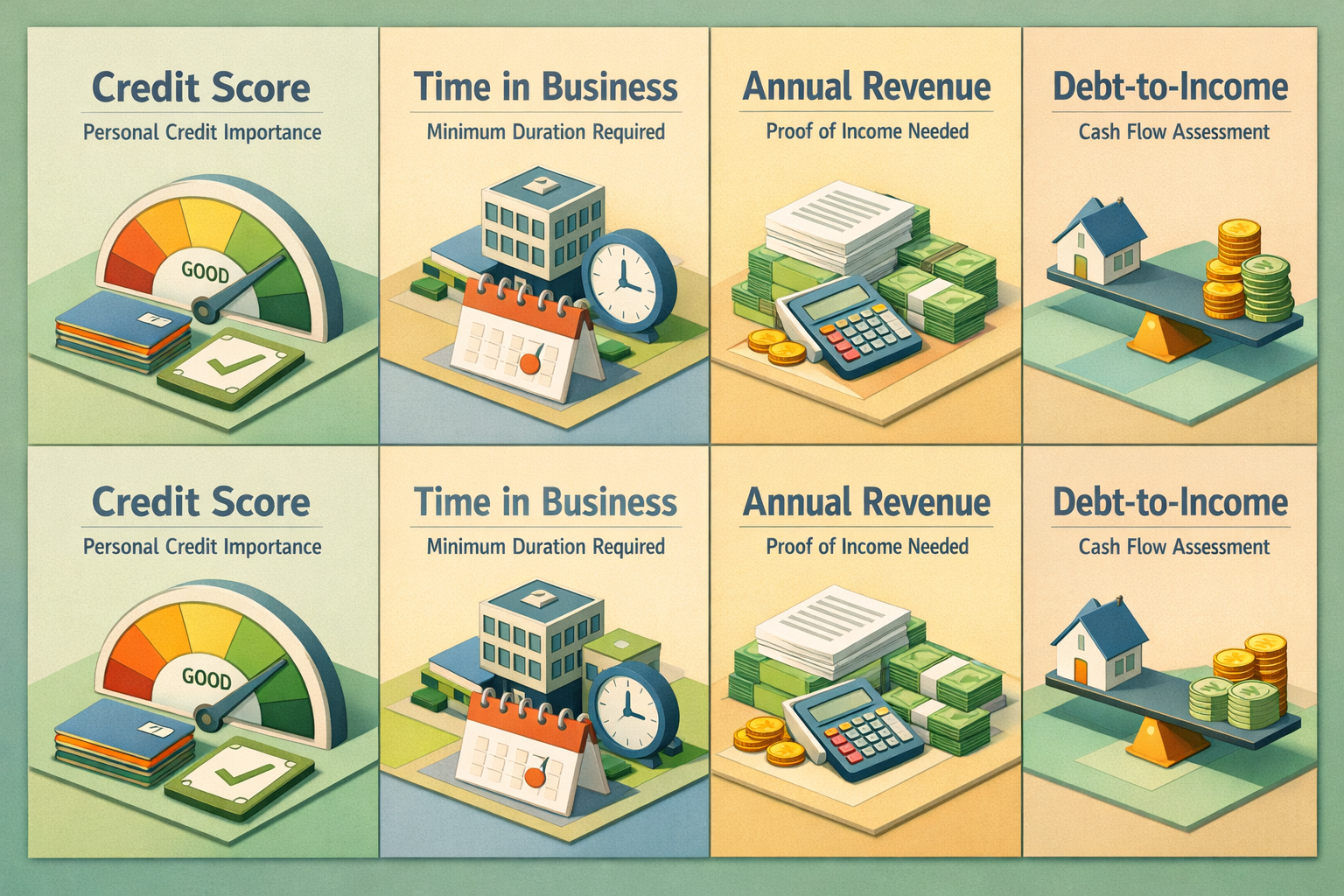

Credit Score and Credit History

Your personal credit score is typically one of the most important factors a lender will review — particularly if your business is young or doesn't yet have a separate business credit profile. Many traditional lenders may look for a minimum personal credit score in the mid-to-upper 600s, though some online and alternative lenders may work with lower scores. Building and maintaining a strong credit history shows lenders that you're a reliable borrower.

Time in Business

Lenders often want to see that your beekeeping business has been operating for at least six months to one year before extending a line of credit. Some traditional banks may require two or more years of business history. If you're just starting out, you may need to explore startup-focused lenders or look into microloans as an alternative first step.

Annual Revenue

Most lenders will ask for proof of your annual or monthly revenue to ensure you have the income necessary to service the credit line. For freelance beekeepers, this might mean presenting bank statements, Schedule F tax returns (used for farm income), invoices from pollination clients, or records of honey product sales. Revenue requirements vary widely — some online lenders may work with businesses earning as little as a few thousand dollars per month, while banks may set higher thresholds.

Debt-to-Income and Cash Flow

Lenders want to see that your business generates enough cash flow to cover repayments without strain. They may calculate your debt service coverage ratio, comparing your income against your existing obligations. For seasonal operations like apiaries, demonstrating consistent annual income — even if it fluctuates month to month — can help support your application.

Documentation You Should Prepare Before Applying

Being organized and prepared with the right paperwork can make your application process much smoother. Lenders will generally request a combination of personal and business financial documents. Here's what most freelance beekeepers should be ready to provide:

- Personal tax returns — typically the last two years, showing total personal income

- Business tax returns or Schedule F filings — demonstrating farm or agricultural business income

- Bank statements — usually three to six months of business account statements showing regular deposits and activity

- Profit and loss statement — a simple summary of your income and expenses, which you may be able to create yourself or with an accountant's help

- Business formation documents — such as your LLC operating agreement, DBA filing, or sole proprietorship registration

- Proof of licenses or permits — any state or county-required beekeeping or agricultural business registrations

- Collateral information — if the lender requires secured credit, you may need to list assets such as equipment, vehicles, or inventory

Having these documents organized before you begin applying can reduce delays and demonstrate to lenders that your operation is professionally managed. It's worth consulting with an accountant who has experience in agricultural businesses, as farm income reporting can have its own nuances that affect how lenders interpret your financials.

Exploring the Right Lenders for Apiary Financing

Not every lender is equally well-suited for freelance beekeepers seeking a line of credit for apiaries. Knowing where to look can save you time and improve your chances of approval.

Community Banks and Credit Unions

Local financial institutions often have a stronger understanding of agricultural businesses in their region. A community bank or credit union that serves rural areas may be more familiar with beekeeping operations and more willing to consider the seasonal nature of your income. Building a relationship with your local bank before applying could also work in your favor.

Online Business Lenders

Alternative online lenders tend to have more flexible eligibility criteria and faster application processes. Many specialize in working capital products for small businesses and self-employed individuals. While interest rates from online lenders may be higher than those from traditional banks, they can be a practical option for freelance beekeepers who are still building their business credit or who need funds quickly.

SBA Microloans

The U.S. Small Business Administration's Microloan Program offers loans of up to $50,000 through nonprofit intermediary lenders. These loans are specifically designed for small and startup businesses, including agricultural freelancers. While SBA microloans are structured as term loans rather than revolving lines of credit, they could serve as a stepping stone to building the credit history and financial track record needed to qualify for a line of credit later.

USDA Farm Service Agency Programs

Freelance beekeepers may also benefit from exploring USDA Farm Service Agency (FSA) loan programs, which are tailored specifically to agricultural producers. The FSA offers operating loans that function similarly to a working capital line of credit, providing funds for farm-related operating expenses. These programs often have more favorable terms for small and beginning agricultural operators.

Tips to Strengthen Your Application as a Freelance Agricultural Business Owner

If you're not quite ready to apply or want to improve your chances of approval, there are several practical steps you can take to position your beekeeping business more favorably with lenders.

- Open a dedicated business bank account if you haven't already. Mixing personal and business finances is a red flag for lenders and makes it harder to document your business income clearly.

- Build your business credit profile by applying for a small business credit card or a trade account with a supplier. Paying these on time helps establish a separate credit history for your business entity.

- Keep detailed financial records throughout the year. Use bookkeeping software or work with an accountant to track income, expenses, and profitability in a format lenders can easily review.

- Register your business formally if you haven't yet. Even a simple sole proprietorship registration or DBA filing can lend legitimacy to your operation in a lender's eyes.

- Diversify your revenue streams where possible. Beekeepers who earn income from multiple sources — honey sales, pollination contracts, beeswax candles, educational workshops — may appear less risky to lenders than those with a single revenue channel.

- Write a simple business plan. Some lenders, especially community banks and SBA intermediaries, appreciate seeing a brief overview of your business model, revenue history, and how you plan to use the credit line.

Taking these steps over time can meaningfully improve your creditworthiness and make the process of securing a working capital loan for agricultural freelancers much more achievable.

●Conclusion

Freelance beekeeping is a genuinely unique agricultural business — and while lenders may not encounter it every day, that doesn't mean financing is out of reach. Understanding the requirements for a business line of credit for a freelance beekeeper puts you ahead of the curve. From establishing your business identity and organizing your financial documents to choosing the right type of lender for your situation, each step you take brings you closer to the flexible working capital your apiary needs to thrive. At LoanWise, we're here to help small business owners and agricultural entrepreneurs navigate their financing options with confidence. Reach out to explore what lending solutions may be available for your beekeeping business today.