For small business owners in the timber, woodworking, and rural land management industries, a portable sawmill can be a game-changing investment. These machines allow entrepreneurs to mill their own lumber on-site, reduce material costs, and open up new revenue streams. But purchasing one outright isn't always financially practical. That's where knowing how to secure equipment financing for a portable sawmill becomes essential. Whether you're a seasoned sawyer or just launching your woodworking venture, the right financing strategy could help you acquire the equipment you need without draining your working capital.

Understanding What Portable Sawmill Financing Actually Covers

Before exploring your financing options, it helps to understand exactly what an equipment loan for woodworking machinery typically covers. Lenders who specialize in equipment financing generally allow borrowers to fund the full purchase price of the equipment itself — including the sawmill unit, hydraulic attachments, blade systems, and in many cases, delivery and installation costs.

Portable sawmills can range from entry-level band mills priced around a few thousand dollars to heavy-duty hydraulic models that cost well over $50,000. The scope of your loan will depend heavily on the type of machine you're targeting and the lender's guidelines. Some financing programs may also cover related accessories or trailer systems used to transport the sawmill between job sites.

It's important to note that equipment financing is asset-based lending — meaning the sawmill itself typically serves as collateral for the loan. This structure can make approval more accessible for small business owners who might not qualify for unsecured business loans, since the lender has a tangible asset backing the debt.

Loan Types Best Suited for Financing Mobile Sawmills

When it comes to financing mobile sawmills, there are several loan structures worth considering. Each comes with its own advantages depending on your business stage, creditworthiness, and cash flow situation.

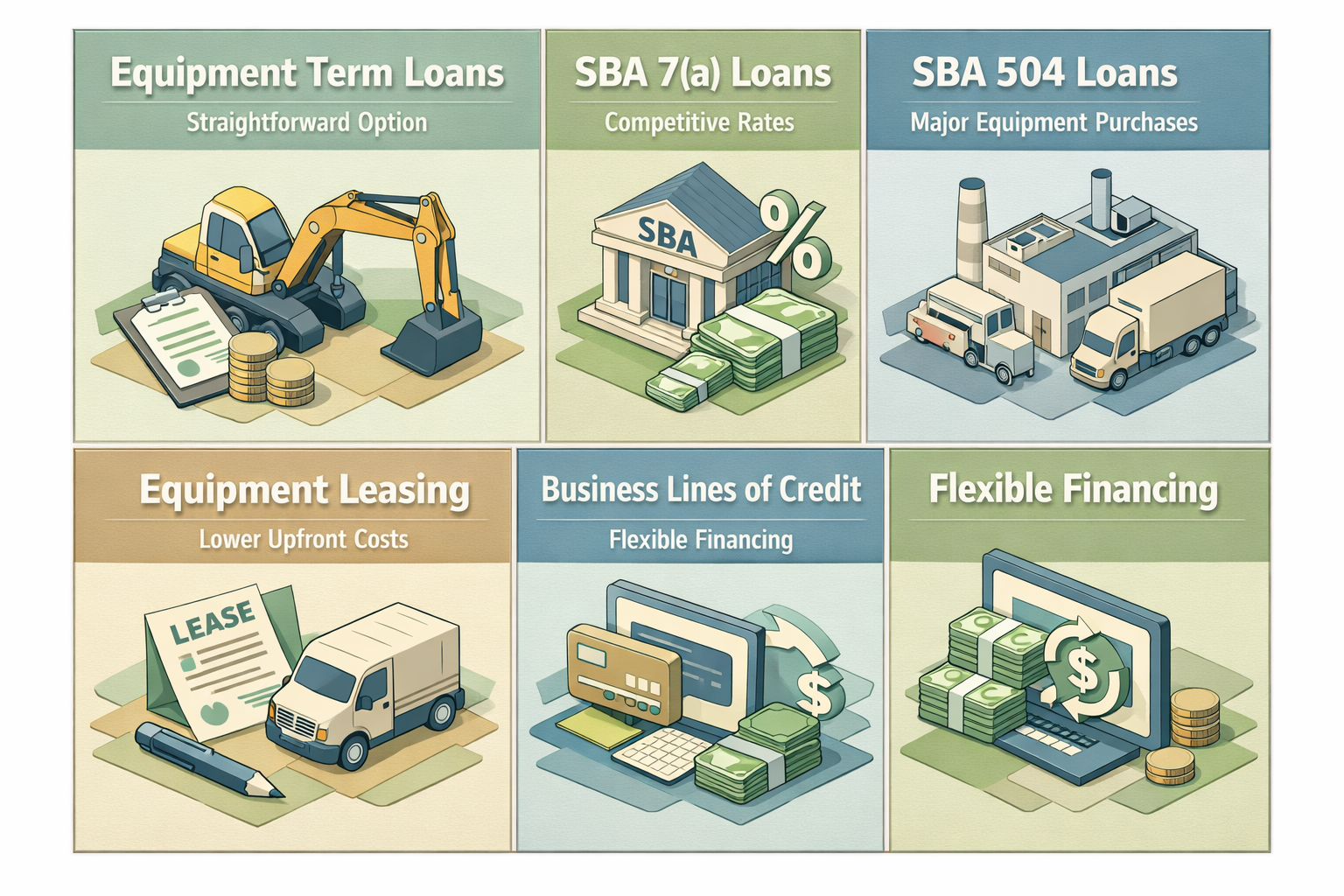

- Equipment Term Loans: These are the most straightforward option. You borrow a lump sum, purchase the sawmill, and repay the loan over a fixed term — often ranging from two to seven years. Interest rates and monthly payments are predictable, which makes budgeting simpler.

- SBA 7(a) Loans: The Small Business Administration's 7(a) program may be used to finance equipment purchases, including woodworking machinery. These loans typically offer competitive rates and longer repayment terms, though the application process can be more involved and time-consuming.

- SBA 504 Loans: While the SBA 504 program is most commonly associated with real estate and large fixed assets, it may also apply to major equipment purchases depending on the lender and loan structure. This option could be worth exploring for higher-cost sawmill systems.

- Equipment Leasing: Rather than owning the equipment outright, some business owners opt to lease a portable sawmill. Leasing typically requires lower upfront costs and may offer tax advantages, though you won't build equity in the asset. At the end of the lease term, you might have the option to purchase the equipment at a residual value.

- Business Lines of Credit: For smaller sawmill purchases or used equipment, a business line of credit could offer flexibility. You draw only what you need and repay as your cash flow allows, though interest rates may be higher than dedicated equipment loans.

Each of these options serves a different type of borrower. A startup woodworking business might lean toward equipment leasing or a microloan, while an established operation with strong revenue could qualify for a conventional equipment term loan or SBA program.

Key Lender Requirements You Should Prepare For

Understanding lender expectations is a critical step when learning how to secure equipment financing for a portable sawmill. While requirements vary by lender and loan type, there are several common factors that commercial lenders typically evaluate.

Business and Personal Credit Scores

Most equipment lenders will review both your business credit profile and your personal credit score. A stronger credit history generally translates into better loan terms and lower interest rates. Borrowers with credit scores in the mid-600s or above may find it easier to qualify, though some lenders specialize in working with those who have less-than-perfect credit. If your score needs improvement, taking a few months to pay down existing debts and correct any errors on your credit report could make a meaningful difference before applying.

Time in Business and Revenue Documentation

Lenders typically want to see that your business has been operating for at least one to two years, though some startup-friendly lenders may work with newer businesses. You'll likely need to provide recent bank statements, tax returns, and profit-and-loss statements to demonstrate consistent revenue and the ability to repay the loan. For seasonal businesses — such as those in the timber or rural land sectors — lenders may also look at annualized income to account for fluctuating cash flow.

Down Payment Expectations

Many equipment loans require a down payment, often in the range of 10% to 20% of the equipment's purchase price, though this can vary. Having a down payment ready not only increases your chances of approval but may also help you secure a lower interest rate and reduce your monthly obligation.

How the Equipment Loan Application Process Typically Works

Once you understand the requirements, the actual application process for an equipment loan for woodworking machinery is relatively straightforward compared to other commercial lending products. Here's a general overview of what to expect.

Step 1 – Identify the Sawmill You Want to Purchase. Lenders will want to know exactly what equipment you're financing. Have the make, model, year, and purchase price ready. If you're buying from a dealer, a formal quote or invoice will strengthen your application.

Step 2 – Gather Your Financial Documents. Pull together at least two years of business and personal tax returns, recent bank statements (typically three to six months), a current profit-and-loss statement, and your business license or formation documents. Being organized at this stage speeds up the approval timeline considerably.

Step 3 – Compare Multiple Lenders. Don't settle for the first offer you receive. Banks, credit unions, online lenders, and SBA-approved lenders all have different products, rates, and underwriting criteria. Comparing at least two to three offers gives you negotiating leverage and helps ensure you're getting competitive terms.

Step 4 – Submit Your Application. Most lenders now offer online applications, and some equipment financing companies can provide decisions within 24 to 48 hours for straightforward requests. More complex loans, like SBA programs, may take several weeks.

Step 5 – Review the Loan Agreement Carefully. Before signing, review the interest rate (fixed vs. variable), repayment term, prepayment penalties, and any fees. Understanding the total cost of the loan — not just the monthly payment — helps you make a truly informed decision.

Smart Strategies to Strengthen Your Financing Application

If you want to maximize your chances of approval and secure favorable terms, a few proactive strategies can go a long way when financing mobile sawmills or any commercial equipment.

- Build a clear business case: Lenders feel more confident when they understand how the sawmill will generate revenue. A brief written summary — or even a simple business plan — explaining your customer base, projected income, and how the equipment fits into your operations can be surprisingly persuasive.

- Separate your business and personal finances: If you haven't already, open a dedicated business bank account and establish a business credit profile. Lenders view this as a sign of operational maturity and financial discipline.

- Consider a co-signer or guarantor: If your credit history is limited or your business is relatively new, having a creditworthy co-signer could open doors that might otherwise be closed. This is particularly useful for startup woodworking operations.

- Look into manufacturer or dealer financing: Some portable sawmill manufacturers or dealers offer in-house financing programs or have relationships with preferred lenders. These programs can sometimes offer promotional rates or flexible terms that aren't available through traditional channels.

- Explore grants and rural business programs: Depending on your location and business type, there may be state or federal grants, USDA rural business development resources, or agricultural lending programs that could supplement or replace traditional equipment financing.

Understanding Interest Rates and Total Loan Costs

Interest rates on equipment loans can vary widely based on your credit profile, loan term, lender type, and current market conditions. Generally speaking, equipment loans may carry rates that range from the mid-single digits to the low-to-mid teens on an annual percentage basis, though these figures can shift depending on the economic environment and your specific qualifications. It's wise to approach any rate quote with a clear understanding of whether it's a fixed or variable rate.

Beyond the interest rate, watch out for origination fees, documentation fees, late payment penalties, and early payoff charges. Some lenders roll these costs into the loan balance, which can inflate the total amount you repay over time. Always ask for a full breakdown of fees before committing to any financing agreement.

Using a simple loan calculator can help you model different scenarios — comparing a shorter term with higher payments against a longer term with lower monthly costs. While a longer term eases cash flow pressure, it typically means paying more interest overall. Finding the right balance depends on your business's revenue cycle and financial goals.

●Conclusion

Knowing how to secure equipment financing for a portable sawmill puts you in a much stronger position to grow your woodworking or timber business without overextending your cash reserves. From traditional equipment term loans and SBA programs to leasing and dealer financing, there are genuinely multiple paths to getting the machinery you need. The key is doing your homework — understanding lender requirements, comparing loan products, and presenting your business as a creditworthy borrower. At LoanWise, we're here to help small business owners and entrepreneurs navigate the lending landscape with clarity and confidence. Reach out to our team today to explore equipment financing options tailored to your unique business needs.