For eligible veterans and service members, a VA loan is one of the most powerful home financing tools available. What many borrowers don't realize is that this benefit can extend beyond a single-family home. You can potentially use a VA loan to purchase a duplex — a two-unit property — and even generate rental income from the second unit while you live in one. However, this strategy comes with specific guidelines that every borrower should understand before moving forward. This article walks through the key requirements for VA loan on a duplex with owner-occupancy, so you can make an informed decision about whether this financing path is right for you.

What Makes a VA Loan Unique for Multi-Unit Properties

The VA loan program, backed by the U.S. Department of Veterans Affairs, offers several advantages that make it stand out from conventional and FHA financing options. These include no down payment requirement in many cases, no private mortgage insurance (PMI), and generally competitive interest rates. Importantly, VA loans can be used to purchase properties with up to four units — including duplexes — provided the borrower meets specific conditions.

When it comes to multi-unit properties, the VA loan program's flexibility may allow eligible veterans to become real estate investors while keeping their monthly housing costs more manageable. The rental income from the second unit of a duplex could help offset mortgage payments, which is an appealing prospect for many first-time homebuyers and experienced homeowners alike.

That said, the VA has clear rules governing how these properties must be used, and lenders are required to verify that those rules are met. Understanding the full picture upfront can help you avoid surprises during the loan approval process.

Core Requirements for VA Loan on a Duplex With Owner-Occupancy

The most fundamental rule when using a VA loan on a duplex is the owner-occupancy requirement. The VA requires that the borrower intend to occupy one of the units as their primary residence. This is a non-negotiable condition — you cannot use a VA loan to purchase a duplex solely as a pure investment property where you don't plan to live.

Here are the core requirements borrowers typically need to meet:

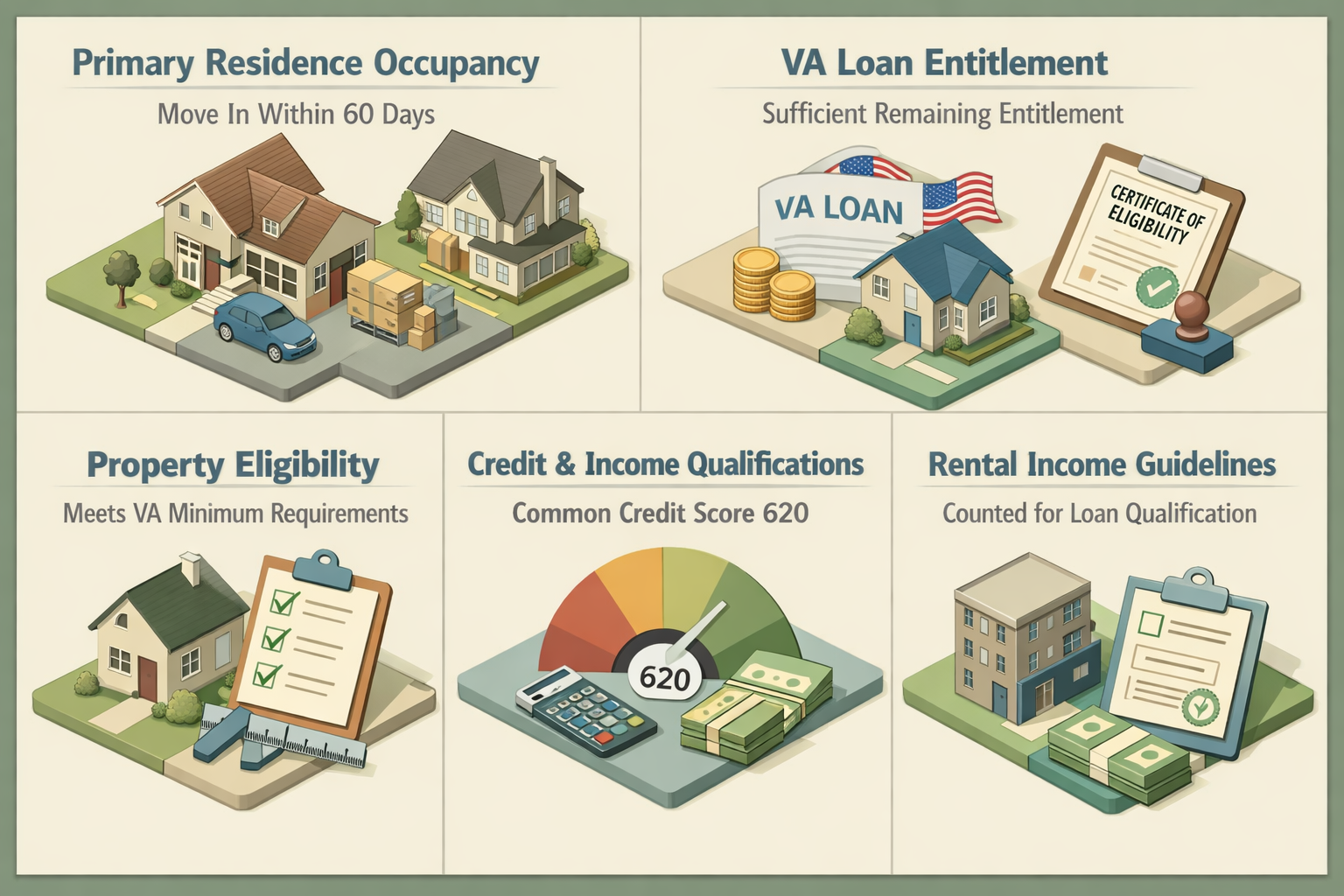

- Primary Residence Occupancy: You must move into one unit of the duplex as your primary residence, typically within 60 days of closing, though extensions may be possible in certain circumstances.

- VA Loan Entitlement: You must have sufficient VA loan entitlement remaining. If you've used your VA benefit before, a portion of your entitlement may be tied up, which could affect your borrowing power.

- Certificate of Eligibility (COE): You'll need a valid COE to confirm your eligibility based on your military service history.

- Property Eligibility: The duplex must meet VA Minimum Property Requirements (MPRs), ensuring it is safe, structurally sound, and sanitary.

- Credit and Income Qualifications: While the VA doesn't set a strict minimum credit score, most lenders impose their own credit overlays. A score of 620 or higher is common, though this can vary by lender.

Meeting these requirements positions you to take full advantage of the owner occupied duplex VA loan opportunity, combining the benefits of homeownership with potential rental income from the adjacent unit.

Understanding the VA's Minimum Property Requirements for Duplexes

Before a VA loan can be approved on any property, a VA-approved appraiser must evaluate it to confirm it meets the VA's Minimum Property Requirements (MPRs). These standards exist to protect both the borrower and the government's loan guarantee by ensuring the property is a sound investment and a livable home.

For a duplex, the MPR inspection may cover both units, not just the one you plan to occupy. Some areas the appraiser typically evaluates include:

- Roof condition and expected remaining life

- Plumbing, electrical, and HVAC systems in working order

- Absence of hazardous materials such as lead paint or asbestos exposure risks

- Adequate heating for both units

- Proper water supply and sewage disposal

- No evidence of wood-destroying insects or pest damage

If the duplex fails to meet any of these requirements, the seller may need to make repairs before the loan can close — or the purchase price may be renegotiated to account for necessary work. It's a good idea to have a general home inspection done in addition to the VA appraisal, since the MPR inspection is not a substitute for a comprehensive property evaluation.

How Rental Income From the Second Unit Can Affect Loan Qualification

One of the most attractive aspects of buying an owner occupied duplex VA loan is the potential to use rental income from the second unit to help qualify for a larger loan amount or offset your debt-to-income (DTI) ratio. However, lenders handle this income in specific ways, and the rules can be more restrictive than many borrowers expect.

Here are a few things to keep in mind about rental income and VA duplex loans:

- Documented Rental History Helps: If the second unit has an established rental history, lenders may be more willing to count a portion of that income. This is typically verified through lease agreements and prior tax returns showing rental income.

- New Rentals May Be Treated Differently: If there's no rental history — for example, on a newly constructed or recently vacant unit — lenders may not count the rental income at all, or may apply a significant vacancy discount.

- Net Rental Income Guidelines: VA guidelines and individual lender policies may allow only a percentage of the gross rental income to be counted, often somewhere in the range of 75%, to account for vacancy and maintenance expenses. However, lenders vary in how they apply this.

- Landlord Experience May Matter: Some lenders prefer or require borrowers to have prior property management or landlord experience before they'll count rental income as qualifying income.

It's worth speaking directly with a VA-approved lender to understand exactly how rental income will be treated in your specific scenario before you make an offer on a property.

VA Loan Entitlement and Loan Limits for Duplex Purchases

VA loan entitlement is the dollar amount the VA guarantees on your behalf. For borrowers with full entitlement — meaning they haven't used their VA benefit before or have had a previous VA loan fully paid off — there's technically no VA-imposed loan limit. This means you could finance a duplex above the conforming loan limits without a down payment, as long as you qualify income-wise.

However, if you have remaining entitlement rather than full entitlement, county loan limits may apply. In that case, you might need to make a down payment if the purchase price exceeds a certain threshold tied to your remaining entitlement and the local conforming limit.

Here's a brief breakdown of how entitlement affects duplex financing:

- Full Entitlement: No down payment required up to what you can qualify for, regardless of loan amount in most cases.

- Partial Entitlement: A down payment may be required if the loan amount exceeds the limit supported by your remaining entitlement.

- Bonus or Tier 2 Entitlement: Many veterans have access to additional entitlement that allows them to purchase higher-priced properties. Your COE and lender can help clarify your available entitlement.

Because duplexes often carry higher price tags than single-family homes, understanding your entitlement status before house hunting can prevent unexpected surprises at the closing table.

Tips for Successfully Securing a VA Duplex Loan

Navigating the requirements for VA loan on a duplex with owner-occupancy can feel complex, but with the right preparation, the process becomes much more manageable. Here are practical tips to help you move toward approval with confidence:

- Work With a VA-Experienced Lender: Not all lenders are equally familiar with VA multi-unit property guidelines. Choosing a lender with specific VA loan expertise can make a significant difference in how smoothly your application progresses.

- Get Your COE Early: Obtaining your Certificate of Eligibility upfront eliminates one potential delay and confirms your eligibility before you invest time in a property search.

- Review Your Credit Profile: While the VA doesn't set a hard minimum score, improving your credit before applying could help you access better interest rates and increase your chances of approval with more lenders.

- Prepare for the MPR Inspection: If you find a duplex you like, consider having a pre-inspection done before making an offer to identify any potential MPR issues that might delay or derail your loan.

- Document Everything: Gather proof of income, military service records, and any existing rental history for the property. Strong documentation can speed up the underwriting process considerably.

- Understand Your DTI Limits: VA lenders typically prefer a DTI ratio below 41%, though some flexibility exists. Make sure your combined housing and debt payments fall within acceptable ranges.

●Conclusion

Purchasing a duplex with a VA loan is a genuinely compelling opportunity for eligible veterans and service members. The combination of zero down payment potential, no PMI, and the ability to generate rental income from the second unit makes this strategy worth exploring seriously. However, success depends on meeting the specific requirements for VA loan on a duplex with owner-occupancy — from living in one unit as your primary residence to ensuring the property passes the VA's Minimum Property Requirements. By working with a knowledgeable VA lender, preparing your financial profile carefully, and understanding how rental income is evaluated, you'll be in a much stronger position to close on a property that serves as both your home and a smart financial asset. Ready to explore your VA loan options? Connect with a LoanWise lending specialist today to get started.