Geodesic dome homes are unlike anything most lenders see every day. Their striking spherical shapes, energy-efficient designs, and unconventional floor plans make them a fascinating housing option — but they also raise a common question among veterans: how to get a VA loan for a geodesic dome home? The short answer is that it may be possible, but it comes with a few extra steps compared to financing a traditional single-family house. Understanding the VA's property requirements, the appraisal process, and how to work with the right lender can make a meaningful difference in whether your loan gets approved. Let's walk through everything you need to know.

What Makes Geodesic Dome Homes Unique in the Eyes of a Lender

Geodesic dome homes are built around a series of interlocking triangular panels that form a roughly spherical or hemispherical structure. This design tends to offer excellent structural strength, energy efficiency, and a smaller environmental footprint. However, from a mortgage lender's standpoint, unique doesn't always mean easy to finance.

Lenders — including VA-approved lenders — typically evaluate a home's value by comparing it to similar recently sold properties in the area, known as comparable sales or "comps." For a geodesic dome, finding reliable comps can be difficult because there simply aren't many of them on the market. This can make the appraisal process more complex and, in some cases, may lead to a lower-than-expected appraised value.

Beyond valuation, lenders also assess whether a property meets minimum habitability and safety standards. A geodesic dome that's been built to code, has proper utilities, and functions as a permanent residence may still qualify — but lenders will look closely at every detail.

VA Loan Eligibility for Unique Home Structures: The Core Rules

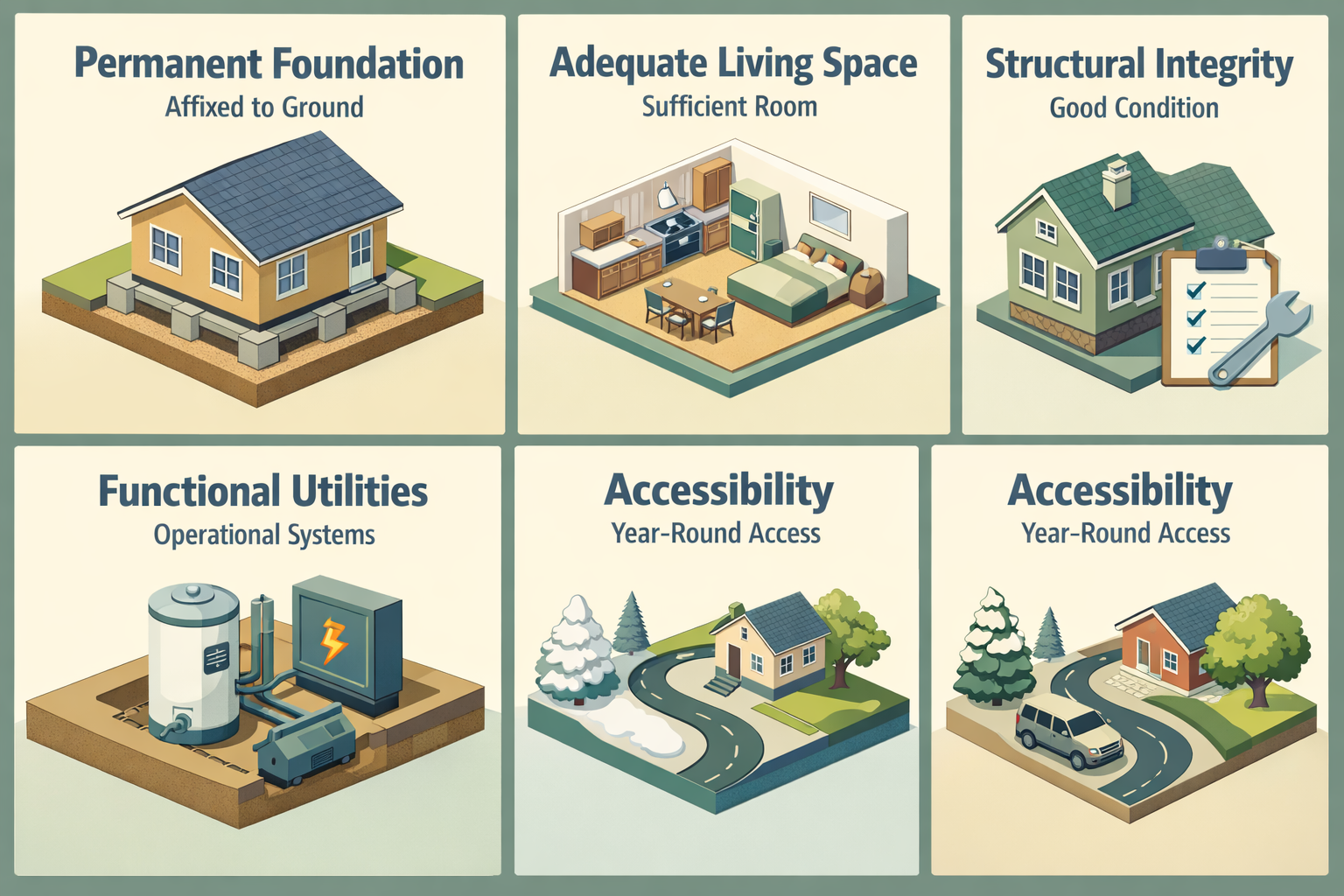

The Department of Veterans Affairs does not explicitly prohibit financing for geodesic dome homes. However, VA loan eligibility for unique home structures hinges on whether the property meets the VA's Minimum Property Requirements (MPRs). These requirements are designed to ensure that the home is safe, structurally sound, and sanitary for the veteran and their family.

For a geodesic dome to meet VA MPRs, it typically needs to satisfy conditions such as:

- Permanent foundation: The home must be affixed to a permanent foundation and classified as real property under local law.

- Adequate living space: The property must have sufficient space for living, sleeping, cooking, and sanitary facilities.

- Structural integrity: The roof, walls, and foundation must be in good condition and free of significant defects.

- Functional utilities: Electrical, plumbing, heating, and cooling systems must be operational and meet local building codes.

- Accessibility: The home must be accessible by a public or private road year-round.

If a geodesic dome meets all of these criteria, it may be considered an eligible property under VA guidelines. That said, individual lenders sometimes impose additional overlay requirements — their own internal policies that go beyond VA minimums — which could present additional hurdles.

How the VA Appraisal Process Works for Non-Traditional Properties

One of the most critical steps in learning how to get a VA loan for a geodesic dome home is understanding the VA appraisal process. Unlike a standard home inspection, a VA appraisal serves two purposes: it verifies that the property meets the VA's MPRs, and it establishes the property's fair market value.

For geodesic domes, VA appraisers may face challenges in determining an accurate market value. Because dome homes are rare, an appraiser might need to cast a wider geographic net to find comparable sales, or they may use alternative valuation methods such as the cost approach — estimating what it would cost to rebuild the home from scratch minus depreciation.

Here are a few things veterans can do to support a smoother appraisal:

- Gather documentation: Collect any building permits, blueprints, engineering certifications, and warranties that confirm the dome was built to code.

- Highlight energy efficiency: Energy-saving features like the dome's natural insulation properties may add value and support a higher appraisal.

- Research local sales: If any similar or non-traditional homes have sold in the area, share that information with the appraiser as potential comparables.

- Be patient: VA appraisals on unique properties may take longer than standard ones, so plan your timeline accordingly.

If the appraisal comes in lower than the purchase price, you'll have options — including negotiating with the seller, paying the difference out of pocket, or walking away from the deal while retaining your VA loan entitlement.

Finding a VA-Approved Lender Experienced with Specialty Properties

Not all VA-approved lenders are equally comfortable with non-traditional home types. Some lenders may decline to finance a geodesic dome based on internal overlays or a lack of experience with unique property types. That's why finding the right lender could be one of the most important steps in your process.

When searching for a lender, consider asking these key questions:

- Have you financed a geodesic dome or other non-traditional home before?

- Do you impose any additional property type restrictions beyond VA guidelines?

- How do you handle appraisals for properties where comps are difficult to find?

- What documentation will you require for an unconventional structure?

Working with a mortgage broker or a lender that specializes in niche and specialty lending may improve your chances. These professionals often have relationships with multiple VA-approved lenders and can match you with one that's more receptive to unique property types.

It's also worth noting that your personal financial profile still plays a major role. Strong credit, stable income, and a solid debt-to-income ratio may help offset lender hesitation around the property type. VA loans don't require a minimum credit score at the federal level, though most lenders set their own minimum — often around 580 to 620 — so keeping your credit in good shape remains important.

Understanding VA Loan Benefits That Apply Regardless of Home Type

Even when financing a unique property, the core benefits of a VA loan still apply to eligible veterans, active-duty service members, and qualifying surviving spouses. These benefits are worth reviewing as you weigh your options:

- No down payment required: Qualified borrowers may finance up to 100% of the appraised value, which could significantly reduce upfront costs.

- No private mortgage insurance (PMI): Unlike conventional and FHA loans, VA loans don't require PMI, which can lower your monthly payment.

- Competitive interest rates: VA loans often carry competitive rates compared to other loan types, thanks to the government guarantee behind them.

- Limits on closing costs: The VA restricts certain fees that lenders can charge, helping to keep borrowing costs in check.

- VA Funding Fee: Most borrowers pay a one-time VA funding fee, which helps sustain the program. The fee varies based on factors such as down payment amount, military category, and whether it's a first or subsequent use of the benefit. Some veterans may be exempt due to service-connected disability.

These benefits don't disappear just because the home has an unusual shape. As long as the property meets VA MPRs and a lender is willing to move forward, eligible veterans can take full advantage of their hard-earned VA benefit.

Common Reasons a Geodesic Dome May Be Declined — and How to Respond

Even with careful preparation, a VA loan application for a geodesic dome could face rejection. Understanding the most common reasons — and how to respond — can help you adapt your strategy.

Appraisal shortfall: If the home appraises for less than the purchase price, you may need to renegotiate with the seller. Sellers are sometimes willing to lower the price when presented with a VA appraisal, especially if alternative financing options for the property are limited.

Lender overlays: Some lenders simply won't finance unusual structures regardless of VA guidelines. In this case, shopping with multiple lenders or working with a broker is your best path forward.

Property condition issues: If the appraiser identifies deferred maintenance or safety concerns, the seller may be required to make repairs before closing. In some cases, this can be negotiated into the purchase agreement.

Zoning or classification problems: If the dome is located in an area zoned for agricultural or recreational use only, or if it's classified as personal property rather than real property, VA financing may not be available. Verifying the property's legal classification before making an offer could save time and money.

Exploring alternative financing — such as a conventional loan with a larger down payment or a portfolio loan through a local bank — may also be worth considering if VA financing proves unavailable for a specific property.

●Conclusion

Purchasing a geodesic dome home with a VA loan is not impossible, but it does require more legwork than a conventional purchase. From navigating VA loan eligibility for unique home structures to finding a lender comfortable with non-traditional properties, veterans who pursue this path benefit from thorough preparation and patience. The key is understanding the VA's property standards, working with an experienced lender, and being ready to advocate for the home's value during the appraisal process. If you're ready to explore your VA loan options for a geodesic dome or any other specialty property, speaking with a knowledgeable mortgage professional is a great first step. Your VA benefit is a powerful tool — and with the right guidance, it may be able to help you finance the uniquely shaped home you've been dreaming of.