For many veterans and active-duty service members, the dream of homeownership includes something a little different from the traditional cookie-cutter house. Straw-bale homes — known for their thick walls, natural insulation, and sustainable construction — have grown in popularity among eco-conscious buyers. But when it comes to financing, things can get complicated. Understanding VA loan eligibility for a straw-bale constructed home is an important first step for any veteran who wants to pursue this unique path to homeownership. The VA loan program offers remarkable benefits, including no down payment and competitive interest rates, but it also has specific property requirements that may create hurdles for non-traditional construction types. This article breaks down what you need to know before you apply.

What Makes a VA Loan Different From Other Mortgage Programs

The VA loan program is backed by the U.S. Department of Veterans Affairs and is designed exclusively for eligible veterans, active-duty service members, and qualifying surviving spouses. It's widely considered one of the most borrower-friendly mortgage programs available, and for good reason.

Some of the most notable benefits include:

- No down payment required in most cases

- No private mortgage insurance (PMI), which can save hundreds per month

- Competitive interest rates that are often lower than conventional loan averages

- Flexible credit qualification standards compared to many other loan types

- Limits on closing costs that lenders are allowed to charge

However, the VA loan program also comes with strict Minimum Property Requirements (MPRs). These standards exist to protect the veteran borrower by ensuring the home is safe, sound, and sanitary. It's these MPRs that often become the primary point of concern when financing alternative or non-traditional construction methods, like straw-bale building.

Unlike conventional loans, VA loans require a VA-approved appraiser to evaluate the property — not just for market value, but also for compliance with these minimum standards. That adds another layer of scrutiny that buyers of eco-friendly homes need to be prepared for.

What Is Straw-Bale Construction and Why It Matters for Financing

Straw-bale construction is a building method that uses compressed bales of straw — typically wheat, rice, or barley straw — as the primary structural or infill material for walls. Once stacked and secured, the bales are usually covered with plaster, stucco, or another protective coating that provides both weatherproofing and fire resistance.

This construction style has been used for over a century, particularly in areas where straw is abundant and energy efficiency is a priority. Today, it's attracting renewed interest among environmentally conscious homeowners because straw bales offer:

- Excellent natural insulation, often exceeding conventional wall assemblies

- Lower embodied carbon during construction compared to many traditional building materials

- A natural, aesthetically distinctive look that appeals to many buyers

- Potentially lower energy bills over the long term

Despite these advantages, straw-bale homes are considered non-standard construction by most lenders and appraisers. This classification can make it more challenging to secure any type of mortgage financing — not just a VA loan. Lenders may worry about resale value, structural longevity, moisture resistance, and the availability of comparable sales data, which are all factors that directly affect the appraisal and approval process.

That said, a VA loan straw bale house transaction isn't impossible. It simply requires more preparation, the right lender, and a property that genuinely meets established standards.

Understanding VA Loan Eligibility for a Straw-Bale Constructed Home: The Core Requirements

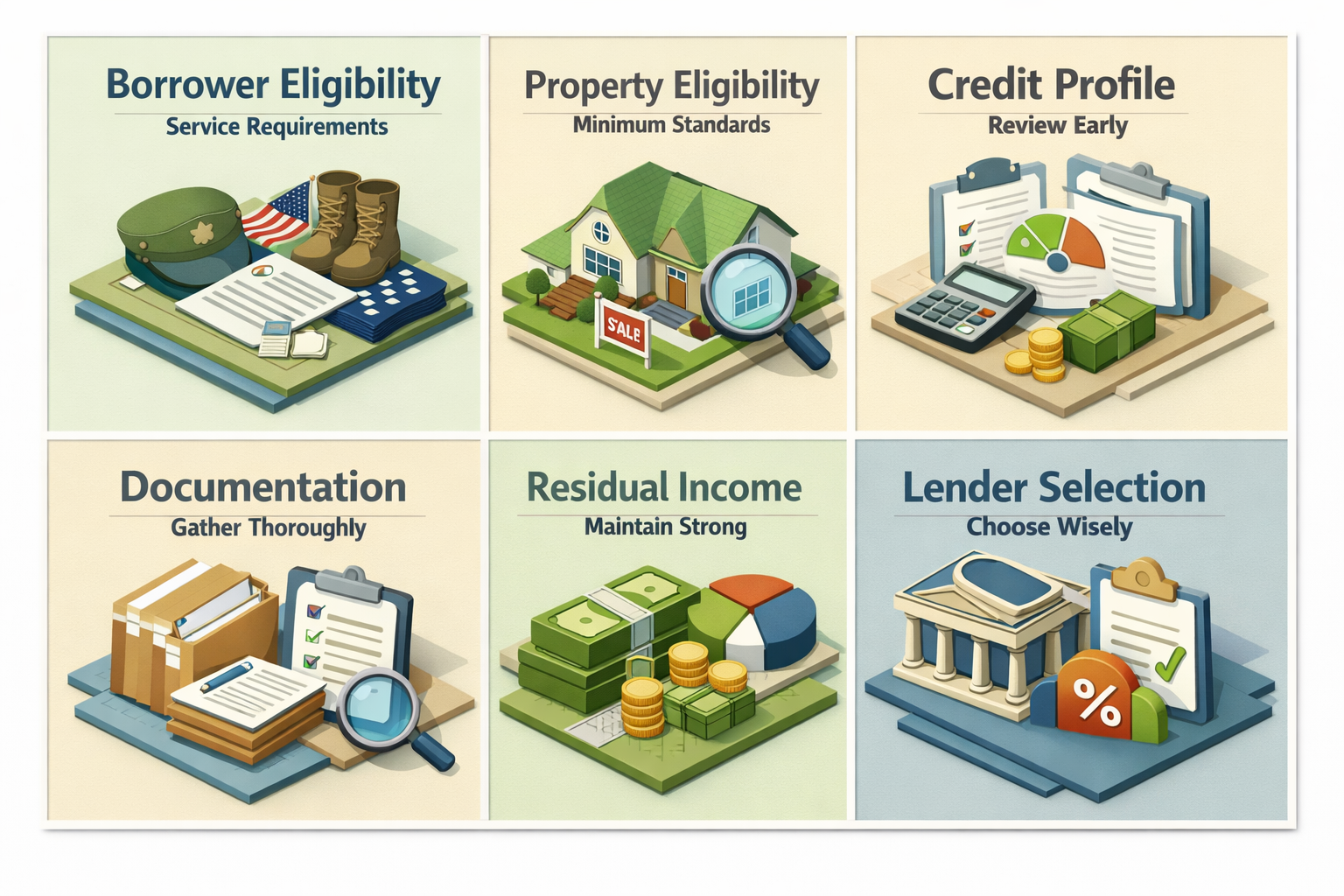

When you're pursuing understanding VA loan eligibility for a straw-bale constructed home, it helps to think in two separate categories: borrower eligibility and property eligibility. Both must be satisfied for a VA loan to move forward.

Borrower Eligibility

On the borrower side, you'll need to meet the VA's standard service requirements. This typically means meeting one of the following criteria:

- Served at least 90 consecutive days of active duty during wartime

- Served at least 181 days of active duty during peacetime

- Served more than 6 years in the National Guard or Reserves

- Are the surviving spouse of a service member who died in the line of duty or from a service-related disability

You'll also need a valid Certificate of Eligibility (COE), which confirms your entitlement to the VA loan eligibility benefit. Most lenders can request this on your behalf through the VA's online system.

From a financial standpoint, VA lenders will review your credit score, debt-to-income (DTI) ratio, and residual income — the amount of money left over after paying monthly obligations. While the VA doesn't set a hard minimum credit score, most lenders impose their own overlays, often requiring a score of at least 580 to 620.

Property Eligibility

This is where the straw-bale element becomes particularly significant. The VA's Minimum Property Requirements cover a broad range of conditions, including structural integrity, roofing, utilities, ventilation, and freedom from hazards. For a straw-bale home to qualify, it would typically need to demonstrate:

- Structural soundness, with walls that are stable and properly supported

- Adequate moisture protection, since straw is vulnerable to rot if water infiltrates the wall assembly

- Compliance with local building codes and permits

- A protective exterior finish, such as stucco or plaster, that is intact and in good condition

- No evidence of pest infestation within the bale walls

A VA-approved appraiser will assess the home against these standards. If the home was built with proper permits, inspected during construction, and meets local building codes, it has a much stronger chance of passing appraisal. Homes built without permits or using experimental techniques that deviate from accepted building practices may face significant challenges.

The Appraisal Challenge: Finding Comparable Sales for Eco-Friendly Homes

One of the biggest practical hurdles in financing a unique construction VA loan is the appraisal. VA appraisers must establish the market value of a property using comparable sales — recently sold homes with similar characteristics in the same area. With straw-bale homes, this can be genuinely difficult.

Straw-bale construction is still relatively rare in most housing markets. If there aren't enough recent sales of similar homes nearby, the appraiser may struggle to assign a confident market value. In some cases, appraisers may expand the search area or look to alternative construction types for comparison, but this introduces additional uncertainty.

There are a few strategies that may help address the appraisal gap:

- Work with an appraiser who has experience with alternative construction. Not all VA-approved appraisers are equally familiar with non-standard materials. Requesting one with relevant experience could lead to a more accurate and favorable valuation.

- Gather documentation on the home's build quality. Construction records, engineer certifications, energy audits, and inspection reports can all support the appraiser's analysis.

- Highlight the home's energy efficiency features. Some appraisers and lenders may give weight to documented energy savings when assessing long-term value.

- Price the property competitively. Sellers of straw-bale homes may need to price with the appraisal challenge in mind to avoid a gap between the agreed purchase price and the appraised value.

It's also worth noting that if the appraiser identifies repairs required by the VA's MPRs, those must typically be completed before the loan can close. This is true for any VA loan, but it can be a more common occurrence with non-standard properties.

Choosing the Right Lender for a Non-Traditional Home Purchase

Not all VA-approved lenders have experience with non-traditional construction types. Many lenders operate within a narrow band of property types and may decline a straw-bale home application simply because it falls outside their typical portfolio. Finding the right lending partner is, therefore, one of the most important steps in this process.

When shopping for a lender, consider asking the following questions:

- Have you previously financed straw-bale or other alternative construction homes?

- Do you have relationships with VA-approved appraisers who specialize in non-standard properties?

- What are your internal overlays beyond the VA's minimum requirements?

- How do you handle MPR repair conditions, and what's your typical timeline?

A lender who is familiar with eco-friendly home mortgage scenarios will be better positioned to guide you through underwriting, communicate realistic expectations, and problem-solve if issues arise during the appraisal or inspection phases.

It's also advisable to get pre-approved before making an offer on a straw-bale property. While pre-approval doesn't guarantee final loan approval — since that depends heavily on the property appraisal — it does confirm your financial eligibility and demonstrates seriousness to sellers.

Some veterans may also want to explore whether a VA construction loan is an option if they're planning to build a new straw-bale home rather than purchase an existing one. VA construction loans are available but can be harder to find among lenders, and they come with their own set of requirements around licensed builders, construction timelines, and inspections.

Steps to Strengthen Your Application Before You Apply

Whether you're buying an existing straw-bale home or planning to build one, there are several proactive steps you can take to improve your chances of a smooth loan process.

Review Your Credit Profile Early

Pull your credit reports from all three major bureaus and address any errors, collections, or derogatory marks before applying. Even a modest improvement in your credit score could open up better lender options and interest rates.

Document the Property Thoroughly

If you're purchasing an existing straw-bale home, gather as much documentation as possible about its construction. This might include:

- Original building permits and inspection records

- Structural engineer reports

- Pest inspection certifications

- Energy efficiency ratings or audits

- Any warranties on the exterior finish or waterproofing systems

This documentation not only supports the appraisal but also helps underwriters feel confident about the property's condition and longevity.

Maintain a Healthy Residual Income

The VA places particular emphasis on residual income — the funds remaining after all debts and housing expenses are paid. Ensuring you have strong residual income can compensate for other areas of financial concern and may reduce lender hesitation around a non-standard property.

Work With a Real Estate Agent Who Knows Alternative Homes

An agent experienced with eco-friendly or non-traditional properties can help you identify homes that are more likely to meet VA standards, negotiate repair conditions, and avoid properties with known financing challenges.

●Conclusion

Pursuing a VA loan for a straw-bale home is absolutely possible, but it does require more groundwork than a standard home purchase. Understanding VA loan eligibility for a straw-bale constructed home means recognizing that both your personal qualifications and the property itself must meet specific standards — and that non-traditional construction adds real complexity to the appraisal and underwriting process.

The good news is that veterans who do their homework, choose the right lender, and select a well-built, code-compliant property are in a much stronger position to succeed. Straw-bale homes can offer genuine long-term value through energy efficiency, sustainability, and distinctive character — qualities that may increasingly appeal to future buyers as eco-conscious living continues to grow.

If you're a veteran interested in financing an alternative or eco-friendly home, LoanWise is here to help you explore your options. Our team understands the nuances of specialty lending and can connect you with VA loan specialists who have experience with non-standard construction. Reach out today to start the conversation and take the next step toward your unique homeownership goal.