Owning a home that carries a historic landmark designation is something many homeowners treasure. These properties tell a story, often featuring irreplaceable architectural details and deep community roots. But when it comes time to access the equity built up in that home, things can get a little more complicated than a standard home equity line of credit. The requirements for a HELOC on a property with a historic landmark designation differ in meaningful ways from what a conventional homeowner might expect. Lenders, appraisers, and preservation authorities all play a role in the process — and understanding each layer can make the difference between a smooth approval and a frustrating dead end.

What Makes a Historic Landmark Property Different From a Standard Home

Before diving into the lending specifics, it helps to understand what sets these properties apart. A historic landmark designation may come from a local municipality, a state historical society, or a federal registry such as the National Register of Historic Places. Each level of designation carries its own set of rules and restrictions.

For homeowners, the most practical implication is that changes to the property — including renovations, additions, or even certain cosmetic updates — may require approval from a historic preservation board or similar governing body. This oversight exists to protect the architectural and cultural integrity of the structure.

From a lender's perspective, these restrictions introduce a layer of complexity. A property that cannot be freely modified may carry different risk considerations than a conventional home, which is why the HELOC historic property process tends to involve more scrutiny and documentation than a typical equity loan application.

How Lenders Evaluate Equity in a Historically Designated Home

At its core, a HELOC is a revolving line of credit secured by the equity in your home. The more equity you have, the more borrowing power you typically hold. But determining the market value of a historic property is rarely straightforward.

Standard appraisals rely heavily on comparable sales — recent home sales in the area with similar features. For historically designated properties, finding true comparables can be challenging. There may be very few homes with similar designations nearby, and those that do exist might have sold under unique circumstances. As a result, appraisers often need specialized experience in valuing historic properties to produce a credible report.

Some lenders may require an appraiser who holds specific credentials in historic property valuation. The appraisal itself might account for both the premium that buyers sometimes pay for historic character and the discount some buyers apply due to renovation restrictions. These two forces can pull in opposite directions, making the final valuation somewhat unpredictable.

Homeowners pursuing a landmark property equity loan should be prepared for an appraisal process that takes longer and potentially costs more than a standard home appraisal. Gathering documentation about the property's history, prior improvements made in compliance with preservation guidelines, and any formal designation certificates can help support a stronger valuation.

Core Borrower Qualification Standards That Still Apply

Despite the added complexity tied to the property's designation, the fundamental borrower qualifications for a HELOC remain largely consistent with standard lending criteria. Lenders will still evaluate the following:

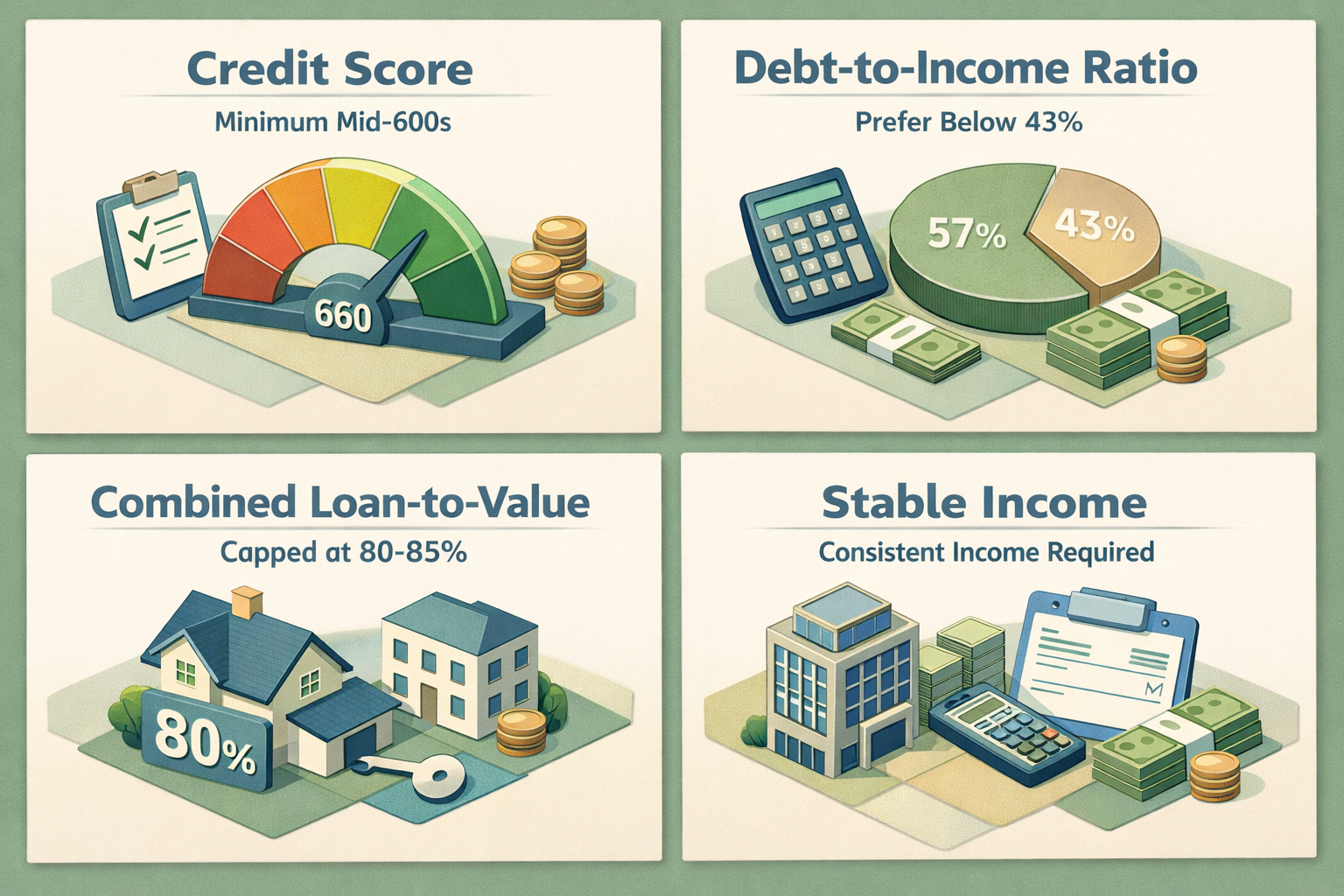

- Credit score: Most lenders typically look for a minimum credit score in the mid-600s, though competitive rates are often reserved for borrowers with scores above 700. A stronger credit profile may help offset some of the perceived risk associated with a non-standard property.

- Debt-to-income ratio (DTI): Lenders generally prefer a DTI below 43%, though some portfolio lenders may extend flexibility depending on the overall strength of the application.

- Combined loan-to-value ratio (CLTV): Most lenders cap the combined balance of all mortgages and the HELOC at around 80% to 85% of the property's appraised value. Given the appraisal challenges noted above, borrowers may find their available equity line is more conservative than expected.

- Stable income and employment history: Lenders want to see consistent income sufficient to cover the new line of credit alongside existing obligations.

These criteria apply regardless of the property type, but borrowers with historically designated homes may find that fewer lenders are willing to underwrite the loan at all, making it important to seek out institutions with experience in specialty or niche lending.

Preservation Rules and How They Affect Your Borrowing Plans

One of the most important — and often overlooked — aspects of the requirements for a HELOC on a property with a historic landmark designation is understanding how preservation rules interact with your intended use of funds. A HELOC is commonly used for home improvements, and this is where things can become particularly nuanced for historic property owners.

If you plan to use the equity line for renovations, those projects will likely need to comply with preservation standards set by the overseeing authority. This could mean using period-appropriate materials, maintaining original architectural features, or avoiding structural changes that alter the property's historic character. Some improvements that would be routine on a standard home — like replacing windows with modern double-pane units or updating exterior siding — may require special approval or may not be permitted at all.

Lenders who understand historic properties will often ask about intended use during the underwriting process. If the proposed improvements conflict with preservation requirements, it could raise concerns about the borrower's ability to complete the work and maintain the property's value. Being transparent about your renovation plans and demonstrating familiarity with applicable preservation guidelines can strengthen your application.

It's also worth noting that some preservation programs offer grants or low-interest loans specifically for approved restoration work. These options might complement or even replace a HELOC depending on the scope of your project.

Finding the Right Lender for a Unique Property HELOC

Not every lender is equipped to handle a unique property HELOC application involving a historically designated home. Large national banks often rely on automated underwriting systems that may flag non-standard properties or simply decline to lend on them. Community banks, credit unions, and portfolio lenders — those who keep loans on their own books rather than selling them on the secondary market — tend to offer more flexibility and personalized underwriting for complex property types.

When shopping for a lender, consider asking the following questions:

- Does your institution have experience lending on historically designated or landmark properties?

- Will you require a specialized appraiser familiar with historic property valuation?

- Are there any additional documentation requirements specific to the property's designation status?

- What is your maximum CLTV for non-standard or unique property HELOC specialty properties?

Working with a mortgage broker who has experience in specialty lending could also be a valuable step. Brokers with access to a wide network of lenders may be better positioned to match your situation with a lender who is comfortable with the nuances involved.

Documentation You Should Gather Before Applying

Preparation is everything when applying for a HELOC on a historically designated property. Beyond the standard income and credit documents, you'll likely need to compile a more robust file that addresses the property's unique status. Here's a helpful checklist of what to consider gathering:

- Official designation certificate: Documentation confirming the property's historic status from the relevant authority, whether local, state, or federal.

- Preservation guidelines: The specific rules and restrictions that apply to the property, ideally in written form from the overseeing body.

- Prior renovation permits and approvals: Records showing that any past improvements were completed in compliance with preservation standards.

- Property history documentation: Information about the property's age, architectural significance, and any notable features that may influence its value.

- Comparable sales data: If you can identify any recent sales of similarly designated properties in your region, this information may help support the appraisal.

- Title insurance information: Some lenders may want confirmation that the historic designation does not cloud the title or restrict transferability in ways that could affect their collateral position.

Having this documentation organized and ready before you submit your application can help reduce delays and demonstrate to the lender that you're a well-prepared, knowledgeable borrower.

●Conclusion

Tapping into the equity of a historically designated home is entirely possible, but it does require more groundwork than a standard HELOC application. From navigating specialized appraisals to ensuring your renovation plans align with preservation requirements, each step calls for a bit more attention and preparation. The good news is that with the right lender, solid documentation, and a clear understanding of what's involved, homeowners can successfully access the equity they've built in these remarkable properties. If you're ready to explore your options, speaking with a lending specialist who understands the requirements for a HELOC on a property with a historic landmark designation is a smart first move. At LoanWise, we're here to help you find the right path forward.