The drone industry is growing fast, and so is the demand for skilled repair technicians who can service drones on location. If you're an entrepreneur looking to launch or grow a mobile drone repair business, one of your biggest challenges may be funding the specialized tools, diagnostic equipment, and spare parts inventory you need to operate. That's where equipment financing for a drone repair business comes in. Whether you're just getting started or looking to scale up, understanding your financing options could make a significant difference in your ability to compete and grow. In this guide, we'll walk you through everything you need to know about how to secure equipment financing for a mobile drone repair service — from the types of loans available to the steps you can take to strengthen your application.

Why Equipment Financing Makes Sense for Mobile Drone Repair Businesses

Running a mobile drone repair service means your business lives and breathes through the quality and reliability of your tools. Soldering stations, multimeters, oscilloscopes, drone-specific diagnostic software, replacement motors, and ESC testers aren't cheap — and that's before you factor in a properly outfitted service vehicle. Purchasing all of this equipment outright could strain your working capital at a time when you need that cash for operating expenses, marketing, and payroll.

Equipment financing is a lending solution specifically designed to help small business owners and entrepreneurs acquire the physical assets they need to run their operations. Unlike a general-purpose business loan, equipment financing typically uses the equipment itself as collateral. This means lenders may be more willing to approve funding even if your business is relatively new or your credit history is limited. For a mobile drone repair operator, this structure could be a real advantage.

Additionally, spreading the cost of equipment over monthly payments helps preserve cash flow — one of the most critical factors in keeping a small business healthy during its early stages. Rather than depleting your reserves on a single large purchase, you can invest those funds in building your client base and delivering excellent service.

Types of Financing Options Available to Drone Repair Entrepreneurs

When it comes to equipment financing for a drone repair business, there's more than one path you can take. Each option comes with its own set of terms, benefits, and considerations.

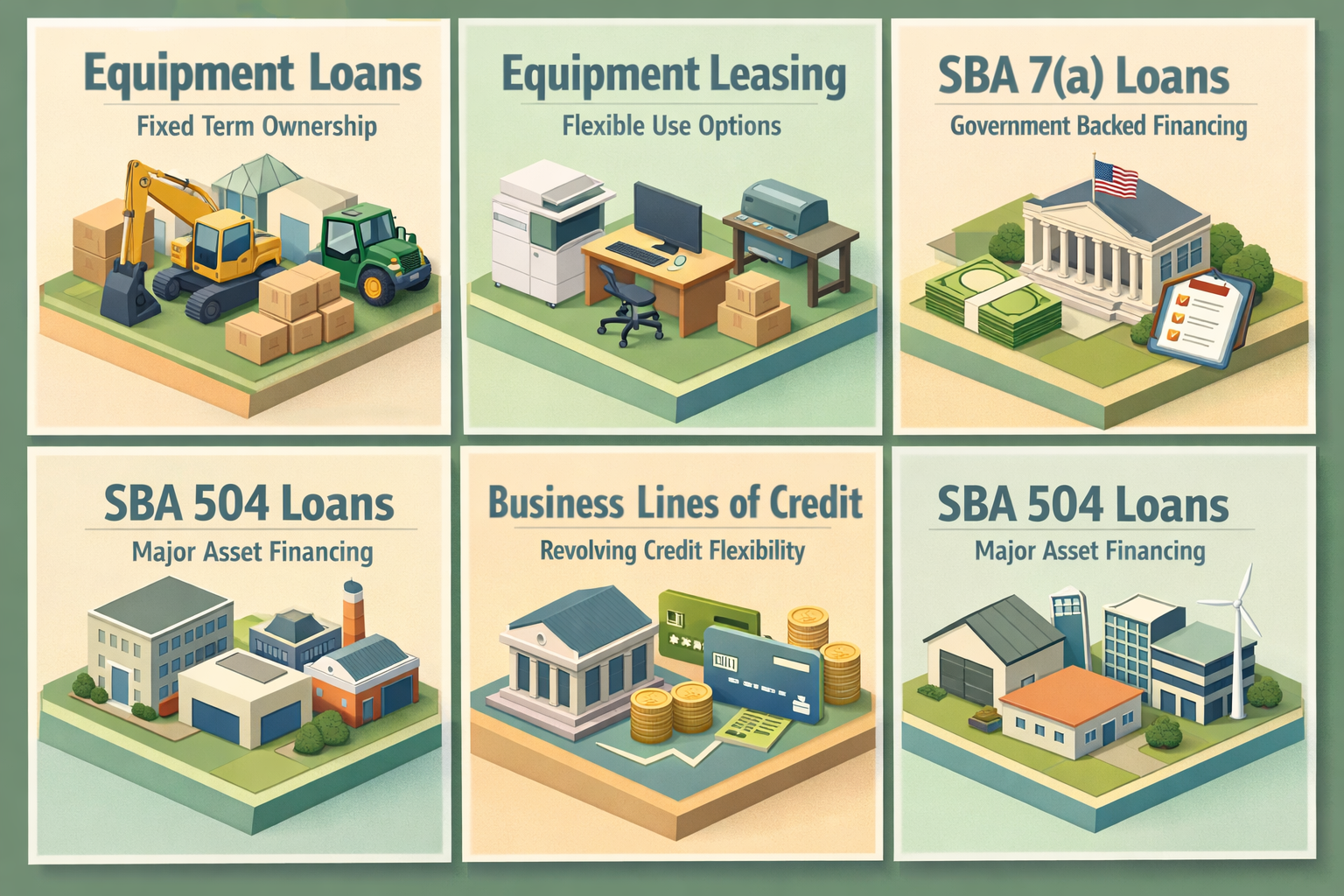

- Equipment Loans: With a traditional equipment loan, you borrow a lump sum to purchase the equipment and repay it with interest over a fixed term. At the end of the loan, you own the equipment outright. This is often a good fit for high-value items like diagnostic systems or specialized repair workstations that you plan to use long-term.

- Equipment Leasing: Leasing allows you to use equipment for a set period by making regular payments, without taking ownership. At the end of the lease, you may have the option to buy the equipment, return it, or upgrade to newer models. For rapidly evolving drone technology, leasing could offer useful flexibility.

- SBA 7(a) Loans: The Small Business Administration's 7(a) loan program can be used for a wide range of business purposes, including equipment purchases. These loans may offer competitive interest rates and longer repayment terms, though they typically involve more documentation and a longer approval process.

- SBA 504 Loans: Primarily designed for major fixed assets, SBA 504 loans might be useful if you're investing in larger equipment purchases or even a dedicated service vehicle for your mobile operations.

- Business Lines of Credit: A revolving line of credit can offer flexibility for purchasing smaller equipment items or restocking parts inventory as needed. This option may work well alongside a primary equipment loan.

Choosing the right financing structure depends on your business's age, credit profile, cash flow, and the specific equipment you need. Speaking with a knowledgeable lender can help you identify the most suitable option for your situation.

Key Eligibility Factors Lenders Look for in Your Application

Before you apply for equipment financing, it helps to understand what lenders typically evaluate. While requirements can vary by lender and loan type, most will look at a combination of the following factors when assessing your application.

Personal and Business Credit Scores

Your credit score is often one of the first things a lender reviews. A stronger credit score generally improves your chances of approval and may result in more favorable interest rates. If your personal credit score needs improvement, consider taking steps to pay down existing debt and correct any errors on your credit report before applying.

Time in Business

Many lenders prefer businesses that have been operating for at least one to two years, as this demonstrates some track record of stability. However, some equipment financing providers may work with newer businesses, particularly when the equipment itself serves as solid collateral. If you're a startup, you may face higher interest rates or be required to make a larger down payment.

Annual Revenue and Cash Flow

Lenders want to see that your business generates enough income to cover loan repayments comfortably. Be prepared to provide bank statements, tax returns, and profit-and-loss statements. Even if your mobile drone repair service is still building its client base, demonstrating consistent and growing revenue can strengthen your application considerably.

Business Plan and Projections

For newer businesses especially, a clear and well-organized business plan can help reassure lenders. Outline your target market, pricing strategy, competitive advantages, and realistic revenue projections. Showing that you understand your industry and have a plan for sustainable growth could tip the scales in your favor.

How to Strengthen Your Loan Application Before You Apply

If you're serious about learning how to secure equipment financing for a mobile drone repair service, preparation is everything. Taking the time to organize your financial documents and address any weaknesses in your credit profile can dramatically improve your chances of approval — and help you qualify for better terms.

- Check your credit reports: Review both your personal and business credit reports for errors or outdated information. Disputing inaccuracies before you apply can give your score a quick boost.

- Separate your business finances: If you haven't already, open a dedicated business bank account and obtain a business credit card. This helps establish a clear financial identity for your business and makes it easier for lenders to assess your cash flow.

- Gather your documentation early: Typical documents include recent bank statements, business and personal tax returns, a profit-and-loss statement, a balance sheet, and your business license. Having these ready can speed up the application process significantly.

- Consider a larger down payment: Offering a down payment — even a modest one — can reduce the lender's risk and may improve your approval odds, particularly if your credit score is not ideal.

- Research multiple lenders: Don't apply with the first lender you find. Compare rates, terms, and eligibility requirements from banks, credit unions, online lenders, and SBA-approved institutions. A small difference in interest rates can add up to meaningful savings over the life of the loan.

Understanding Loan Terms and Total Cost of Borrowing

When evaluating equipment financing offers, it's important to look beyond the monthly payment and understand the full cost of borrowing. Several factors will influence how much you ultimately pay over the life of your loan.

Interest Rate: Equipment loan interest rates can vary widely depending on your creditworthiness, the lender, and the loan structure. Fixed rates offer predictability, while variable rates may start lower but could increase over time. Always clarify whether the rate you're quoted is fixed or variable.

Loan Term: Equipment financing terms typically range from one to seven years, though this can vary. Shorter terms often mean higher monthly payments but less total interest paid. Longer terms reduce your monthly burden but may cost more overall.

Fees and Origination Costs: Some lenders charge origination fees, documentation fees, or prepayment penalties. These costs can add up, so be sure to ask about all fees before signing any agreement.

Residual Value Considerations: If you're leasing equipment, pay attention to the residual value — the estimated worth of the equipment at the end of the lease. This will affect your buyout price if you choose to purchase the equipment later.

Taking the time to calculate the total cost of borrowing — not just the monthly payment — helps you make a truly informed decision. A loan with a lower monthly payment isn't necessarily the best deal if it comes with high fees or a much longer repayment period.

Working with the Right Lender for Your Drone Repair Business

Not every lender will be familiar with the drone repair industry, and that's okay. What matters most is finding a lender that understands small business equipment financing and is willing to work with businesses in emerging or niche technology sectors. Here are a few types of lenders worth considering.

Community Banks and Credit Unions

Smaller financial institutions often take a more personalized approach to lending. They may be more willing to consider the full picture of your business rather than relying solely on automated credit scoring. Building a relationship with a local bank or credit union could pay off, especially as your business grows and your financing needs evolve.

Online Business Lenders

Online lending platforms have made it faster and easier for small business owners to access financing. Many offer streamlined applications, quick approval decisions, and flexible eligibility requirements. While interest rates from online lenders may sometimes be higher than traditional banks, the speed and convenience can be worth it for businesses that need funding quickly.

SBA-Approved Lenders

If you qualify for an SBA loan, working with an SBA-approved lender gives you access to government-backed financing with potentially lower rates and longer repayment terms. The process may take longer, but the financial benefits could be significant for a business making substantial equipment investments.

Regardless of which type of lender you approach, come prepared with your documentation, a clear explanation of how the equipment will support your business operations, and a realistic repayment plan. Demonstrating professionalism and preparation builds lender confidence.

●Conclusion

Learning how to secure equipment financing for a mobile drone repair service doesn't have to be overwhelming. With the right preparation, a clear understanding of your financing options, and a lender that supports small business growth, you can acquire the tools you need to build a thriving mobile drone repair operation. Start by reviewing your credit profile, organizing your financial documents, and comparing lenders to find the best fit for your business. The drone repair market is full of opportunity — and the right financing could be the foundation that helps your business take flight. Ready to explore your equipment financing options? Reach out to a LoanWise lending specialist today and take the first step toward funding your business's future.