When cash flow tightens and traditional loans feel out of reach, many small business owners turn to a merchant cash advance for quick relief. It's one of the more accessible forms of short-term business financing available today — but it's also one of the most misunderstood. Before you sign on the dotted line, it's worth understanding exactly how this funding option works, what it costs, and whether it's the right move for your business. This guide breaks it all down in plain language so you can make a confident, informed decision.

What Is a Merchant Cash Advance and How Does It Work

A merchant cash advance (MCA) is a type of revenue-based financing where a lender provides a lump sum of capital to a business upfront. In return, the business agrees to repay that amount — plus fees — by surrendering a fixed percentage of its daily or weekly sales over time.

It's important to understand that an MCA is technically not a loan. It's a purchase of future receivables. That distinction matters because MCAs aren't subject to the same lending regulations as traditional loans, which can affect your rights as a borrower.

Here's a simplified example of how repayment typically works:

- Advance amount: The funder provides capital, say $20,000, to your business upfront.

- Factor rate: Instead of an interest rate, MCAs use a factor rate (often expressed as 1.2 to 1.5 or higher). If your factor rate is 1.3, you'd repay $26,000 total.

- Holdback percentage: The funder collects a set percentage — called the holdback — from your daily credit or debit card sales until the balance is paid off.

Because repayment is tied to your actual revenue, slower sales months mean smaller daily payments, and stronger months mean faster repayment. This flexibility is one of the reasons MCAs appeal to businesses with fluctuating income, like restaurants, retailers, and seasonal operations.

Who Typically Qualifies for a Merchant Cash Advance

One of the biggest draws of a merchant cash advance is its relatively lenient qualification standards compared to traditional bank loans or SBA financing. small business owners seeking fast capital who may struggle to meet conventional credit requirements often find MCAs more accessible.

Funders typically look at the following factors when evaluating an application:

- Monthly credit card or debit card sales volume: Since repayment is drawn from daily sales, providers want to see consistent revenue. Many require a minimum monthly volume, which can vary by funder.

- Time in business: Most MCA providers prefer businesses that have been operating for at least six months to one year, though some may work with newer businesses.

- Credit score: While some funders check personal credit, MCA approval is often less dependent on credit scores than traditional lending. Owners with less-than-perfect credit may still qualify.

- Bank statements: Funders typically review several months of bank statements to assess cash flow health and consistency.

This makes MCAs particularly relevant for entrepreneurs in retail, food service, e-commerce, and service industries where card-based sales are common. If your business processes a steady volume of card transactions, you may find it relatively straightforward to qualify — even if your financial history isn't perfect.

Understanding the True Cost of a Merchant Cash Advance

Here's where many small business owners get caught off guard: the cost of a merchant cash advance can be significantly higher than it appears on the surface. Because MCAs use factor rates rather than annual percentage rates (APRs), it's easy to underestimate how much you're actually paying to borrow.

Let's break it down. A factor rate of 1.3 on a $20,000 advance means you repay $26,000 — a $6,000 cost of capital. But depending on how quickly you repay (which depends on your sales volume), that $6,000 fee could translate to an effective APR well above what you'd pay on a traditional small business loan or line of credit.

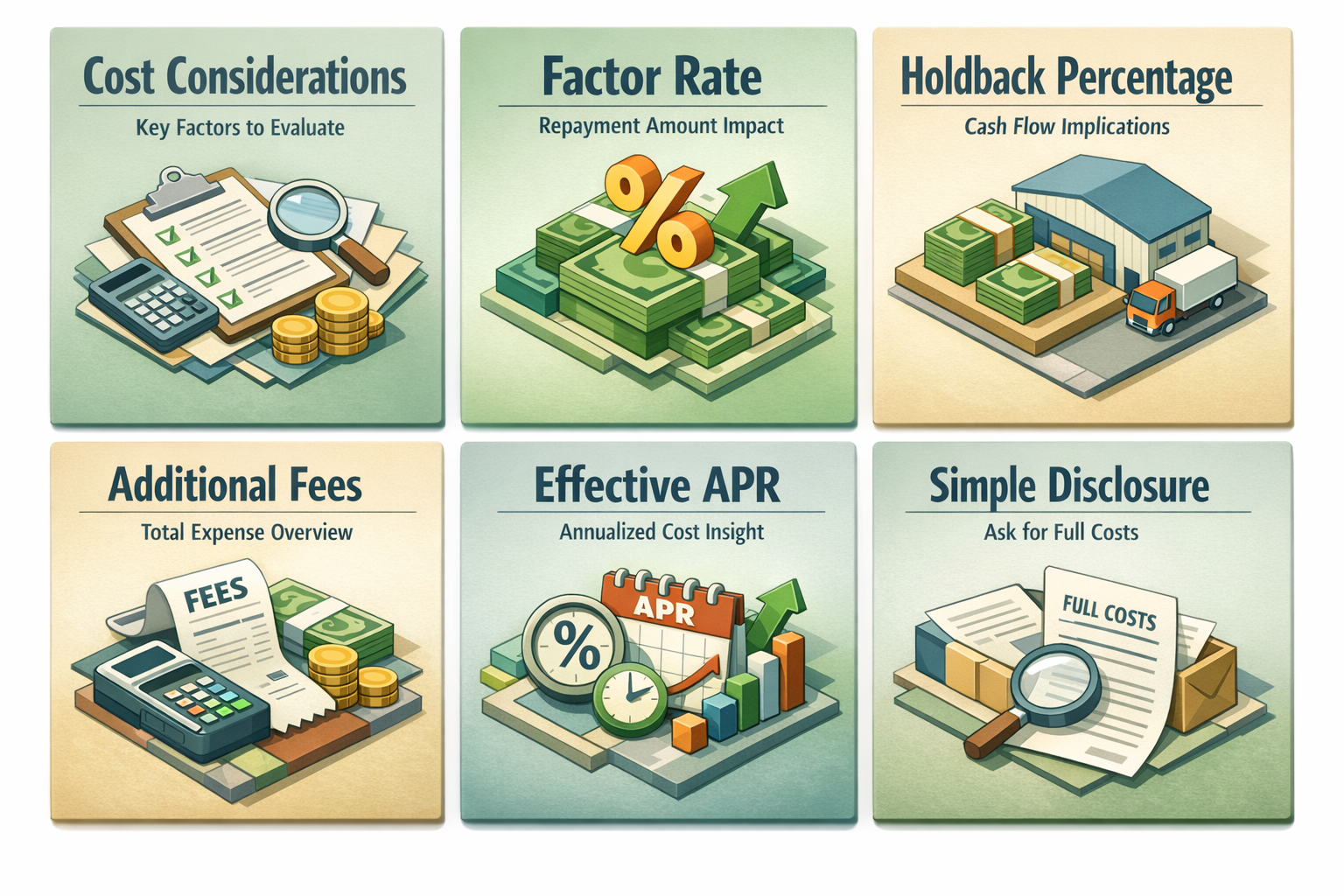

Key cost considerations to evaluate include:

- Factor rate: Typically ranges from 1.1 to 1.5 or higher, depending on the funder and your business profile. A higher factor rate means a greater total repayment amount.

- Holdback percentage: Usually falls between 10% and 20% of daily sales. A higher holdback speeds up repayment but reduces your daily cash flow in the short term.

- Additional fees: Some providers charge origination fees, administrative fees, or other costs that add to the total expense.

- Effective APR: When repayment happens quickly, the annualized cost can be substantial — sometimes exceeding rates associated with other short-term financing options.

It's strongly advisable to ask any MCA provider for a full disclosure of all costs before accepting an offer. Comparing the true cost of borrowing across multiple providers — not just the factor rate — gives you a clearer picture of the real cost.

Advantages That Make MCAs Attractive to Small Business Owners

Despite the higher cost of capital, merchant cash advances offer several genuine benefits that can make them a practical choice for certain business situations. Understanding these advantages helps you assess whether the tradeoff makes sense for your circumstances.

- Fast funding: MCA approvals and funding can often happen within a few business days — sometimes even within 24 hours. For businesses facing urgent cash flow gaps or time-sensitive opportunities, this speed can be invaluable.

- Flexible repayment: Because payments are tied to a percentage of sales, you're not locked into a fixed monthly payment. During slower periods, your payments naturally decrease, which can ease financial pressure.

- Minimal collateral requirements: Most MCAs are unsecured, meaning you typically don't need to pledge business assets or personal property to qualify.

- Accessible for imperfect credit: Entrepreneurs who've faced past financial challenges may still access funding when traditional lenders decline their applications.

- Simple application process: Compared to the documentation-heavy process of bank loans or SBA loans, MCA applications are often streamlined and straightforward.

For a seasonal business needing to stock up on inventory before a peak sales period, or a restaurant covering unexpected equipment repairs, the speed and flexibility of a merchant cash advance may outweigh its higher cost — at least in the short term.

The Risks and Drawbacks You Should Carefully Consider

A balanced view of merchant cash advances requires an honest look at the risks. While they serve a real need in the small business lending market, they're not without significant drawbacks that every borrower should weigh carefully.

- High cost of capital: As discussed, the effective cost of an MCA can be considerably higher than traditional financing options. Over-reliance on MCAs can erode profit margins over time.

- Daily cash flow impact: The holdback mechanism means a portion of every day's sales goes directly to the funder. During challenging periods, this can put additional strain on operational cash flow.

- Risk of stacking: Some businesses take out multiple MCAs simultaneously — known as stacking — to cover cash shortfalls. This practice can quickly become financially dangerous and lead to a debt spiral.

- Limited regulatory protection: Because MCAs are structured as commercial transactions rather than loans, they may not carry the same consumer or borrower protections that apply to traditional lending products.

- No benefit to credit building: Unlike small business loans or credit cards, MCA repayment typically doesn't get reported to business credit bureaus, so it won't help build your business credit profile.

It's wise to consult with a financial advisor or a trusted lending professional before committing to a merchant cash advance, especially if you're considering it as a recurring funding strategy rather than a one-time solution.

Smart Alternatives to Explore Before Choosing an MCA

A merchant cash advance may be the right tool in specific situations, but it's always worth exploring other financing options first. Depending on your business profile and needs, one of these alternatives may offer better terms at a lower overall cost.

- SBA 7(a) loans: The Small Business Administration's flagship loan program offers competitive rates and longer repayment terms for qualifying businesses. The application process takes longer, but the cost savings can be significant.

- Business line of credit: A revolving line of credit gives you flexible access to funds when you need them, and you only pay interest on what you draw. This is often more cost-effective for managing ongoing cash flow needs.

- Term loans: Traditional or online lender term loans provide a lump sum with predictable fixed payments, often at lower rates than MCAs — particularly for businesses with solid financials.

- Invoice financing: If your business invoices commercial clients, invoice financing or factoring lets you unlock capital tied up in unpaid invoices without taking on additional debt in the traditional sense.

- Equipment financing: For businesses needing to purchase or upgrade equipment, dedicated equipment loans may offer favorable terms since the equipment itself serves as collateral.

- Business credit cards: For smaller, recurring expenses, a business credit card with a competitive rate or rewards program may be more practical than a cash advance.

The best financing choice depends on your business's age, revenue, credit profile, and the purpose of the funds. Working with an experienced business lending advisor can help you identify the most cost-effective path forward.

●Conclusion

A merchant cash advance can be a lifeline for small business owners who need fast capital and may not qualify for conventional financing. Its speed, accessibility, and flexible repayment structure make it a genuinely useful tool — but only when used strategically and with a clear understanding of the costs involved. Before moving forward, take time to compare your options, read all terms carefully, and consider speaking with a qualified lending professional who can help you evaluate the full picture. At LoanWise, we're committed to helping small business owners and entrepreneurs find financing solutions that truly fit their needs. Reach out today to explore your options with confidence.