Understanding Mortgage Loan Amortization Schedules for Real Estate Investors

Every successful real estate investor knows that understanding your mortgage loan amortization schedule isn't just about tracking payments. It's about unlocking strategic advantages that can dramatically impact your portfolio's cash flow and long-term profitability. Whether you're evaluating DSCR loans for rental properties or considering extended amortization periods for improved monthly cash flow, mastering these fundamentals separates experienced investors from those still learning the ropes.

The mortgage payment breakdown you receive each month tells a story about your investment's financial trajectory. As property values continue rising and loan limits expand, savvy investors are leveraging amortization knowledge to make more informed financing decisions and optimize their investment strategies.

Essential Components of Your Amortization Schedule

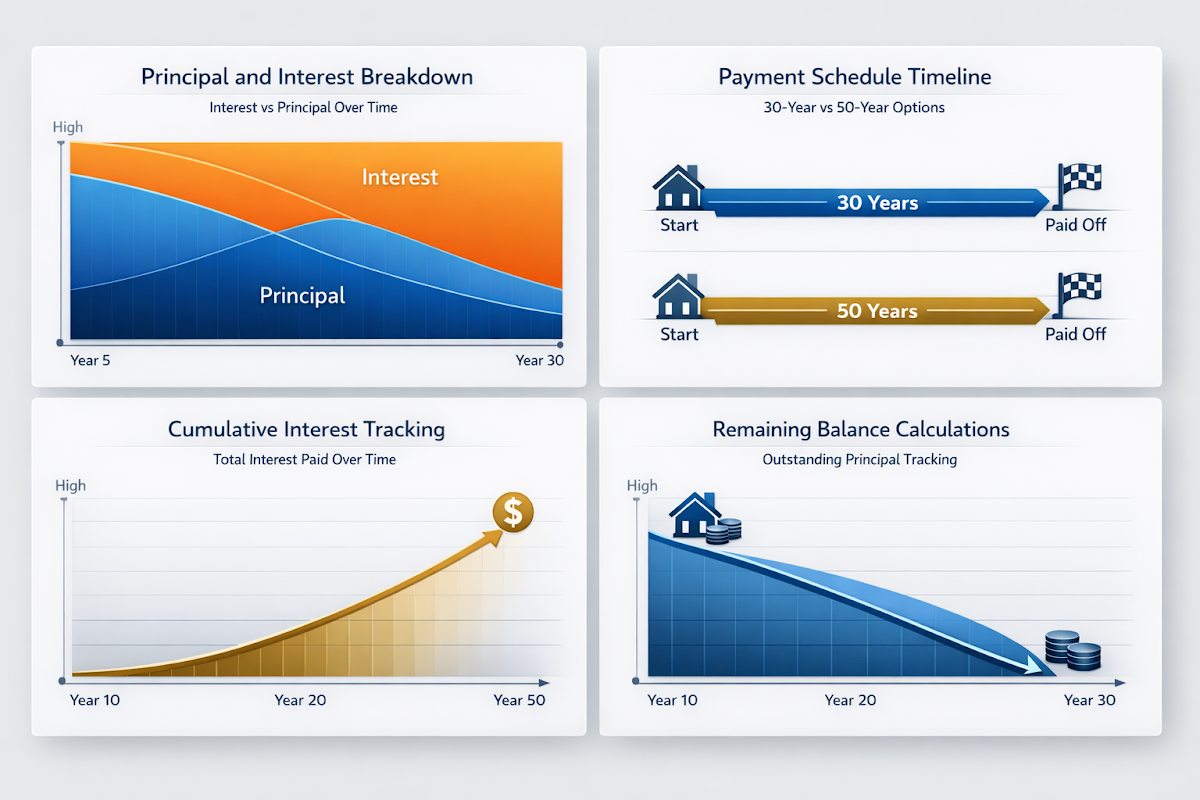

Essential components of your amortization schedule reveal the financial mechanics behind every investment property payment. Understanding these elements helps investors make strategic decisions about financing options and cash flow optimization.

- Principal and Interest Breakdown: Early payments typically consist of more interest than principal, gradually shifting over the loan term to favor principal reduction

- Payment Schedule Timeline: Traditional 30-year schedules differ significantly from extended 50-year options, which may offer lower monthly payments but extend interest payment periods

- Cumulative Interest Tracking: Monitor total interest paid over time to evaluate the true cost of your investment financing

- Remaining Balance Calculations: Track outstanding principal to understand equity building and refinancing opportunities

Key Factors That Impact Your Payment Structure

Key factors that impact your payment structure extend beyond simple interest rates and loan amounts. Modern investors must consider multiple variables that influence their mortgage loan amortization schedule effectiveness.

- Interest Rate Environment: Current DSCR loan rates ranging from 5.875% to 7.375% significantly affect your amortization pattern and cash flow projections

- Loan Term Selection: Choosing between traditional 30-year terms and emerging 50-year options fundamentally alters your monthly payment obligations and total interest costs

- Property Cash Flow Requirements: DSCR ratios of 1.25 or higher influence loan approval and may affect amortization terms offered by lenders

- Conforming Loan Limits: The increased limit of $832,750 for 2026 allows investors to access better amortization terms without requiring jumbo loan pricing

Strategic Benefits of Extended Amortization Periods

Strategic benefits of extended amortization periods are gaining attention among real estate investors seeking improved cash flow management. The proposed 50-year mortgage option represents a significant shift in how investors might structure their financing.

- Enhanced Monthly Cash Flow: Lower monthly payments free up capital for additional investments or property improvements that increase rental income potential

- Portfolio Expansion Opportunities: Reduced payment obligations may qualify investors for additional properties by improving debt-to-income ratios on subsequent acquisitions

- Market Timing Flexibility: Lower carrying costs provide more time to optimize rental rates and property performance before considering refinancing or sale strategies

Step-by-Step Process for Analyzing Investment Returns

A step-by-step process for analyzing investment returns using your mortgage loan amortization schedule helps investors make data-driven financing decisions. This systematic approach ensures you're maximizing the financial potential of each property acquisition.

- Calculate True Cash-on-Cash Returns: Compare your actual monthly payments against rental income to determine if your amortization schedule supports positive cash flow targets

- Project Long-Term Equity Building: Analyze principal reduction over 5, 10, and 20-year periods to understand how amortization contributes to wealth building alongside property appreciation

- Evaluate Refinancing Opportunities: Monitor interest rate environments and remaining balances to identify optimal timing for rate improvements or cash-out refinancing

- Compare Financing Alternatives: Assess how different amortization periods affect your investment's internal rate of return and overall portfolio performance

Optimizing DSCR Loan Performance Through Smart Scheduling

Optimizing DSCR loan performance through smart scheduling requires understanding how amortization affects your debt service coverage ratio over time. Since these loans focus on property cash flow rather than personal income, the payment structure directly impacts qualification and terms.

- Maintain Minimum DSCR Requirements: Ensure your amortization schedule supports the 1.25 minimum ratio needed for optimal rates, accounting for potential rental income fluctuations

- Plan for Rate Environment Changes: Structure your amortization to accommodate potential rate increases while maintaining positive cash flow and DSCR compliance

- Leverage Simplified Qualification Process: Take advantage of DSCR loans' streamlined requirements by choosing amortization periods that maximize property-level returns without tax return complications

The Bottom Line on Amortization Strategy

The bottom line on amortization strategy is that informed investors use these schedules as powerful tools for portfolio optimization. Understanding how amortization affects your mortgage loan performance enables better decision-making across your entire investment strategy. Whether you're considering extended payment periods for improved cash flow or traditional schedules for faster equity building, the key lies in aligning your financing structure with your investment goals. Smart investors recognize that mastering amortization schedules isn't just about making payments but about creating sustainable wealth through strategic real estate financing.

●Conclusion

Mastering your mortgage loan amortization schedule transforms you from a passive property owner into a strategic real estate investor. The financial insights gained from understanding payment breakdowns, exploring extended amortization options, and optimizing DSCR loan performance create competitive advantages that compound over time. As lending environments evolve and new financing products emerge, investors who thoroughly understand amortization principles will consistently identify better opportunities and structure more profitable deals.

Your next investment property acquisition should begin with careful amortization analysis. Consider how different payment structures align with your cash flow goals, evaluate the long-term implications of various loan terms, and remember that the right amortization strategy can significantly impact your investment's success trajectory.