Investment Property Renovation Loan Guide

Real estate investors often face a common challenge: finding the right financing to purchase and renovate properties simultaneously. Home renovation loans might offer a strategic solution that consolidates both purchase and improvement costs into a single financing package. These specialized loan products could streamline your investment process while potentially reducing overall borrowing costs and administrative complexity.

Understanding the landscape of renovation financing becomes crucial when you're evaluating fix and flip opportunities or planning to add value to rental properties. The right loan structure may determine whether a deal pencils out profitably or becomes a financial burden that drains your investment capital.

Essential Home Renovation Loan Requirements

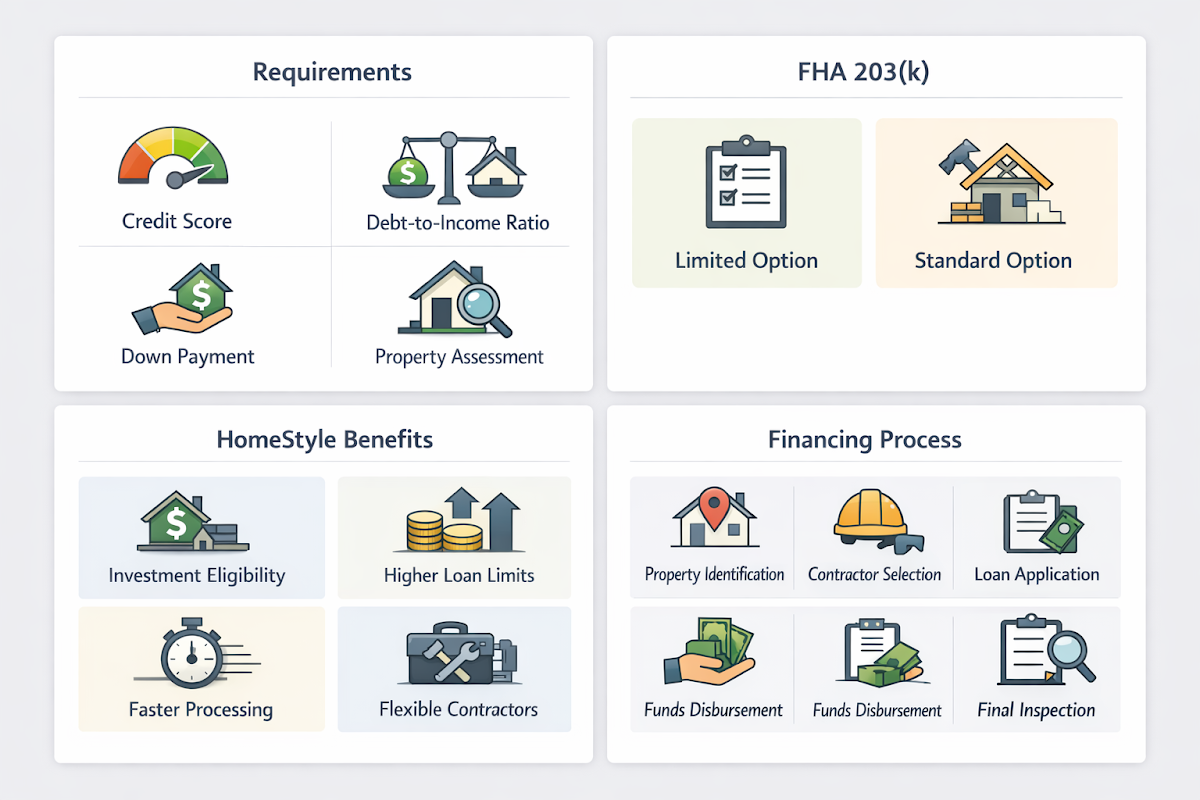

Essential home renovation loan requirements typically vary by program, but understanding these basics helps investors prepare their applications more effectively. Most renovation loan programs have specific qualification criteria that differ from traditional mortgage products.

- Credit score requirements often range from 580 to 620 for government-backed programs, though some conventional options may require higher scores

- Debt-to-income ratios usually need to stay below 43% to 50%, depending on the specific loan product and lender guidelines

- Down payment requirements might be as low as 3.5% for FHA programs, though investment properties typically require higher down payments

- Property condition assessments and contractor estimates are generally required before loan approval to determine renovation scope and costs

FHA 203(k) Loan Details for Investors

FHA 203(k) loan details reveal a government-backed financing option that could benefit certain investment scenarios, though these loans come with specific limitations for investor use. The program offers two main variations that serve different renovation needs and budgets.

- Limited 203(k) loans typically cover smaller renovations up to enhanced limits, making them suitable for cosmetic improvements and minor structural work

- Standard 203(k) loans may accommodate major renovations including room additions, structural changes, and comprehensive property overhauls

- Owner-occupancy requirements generally apply to FHA programs, limiting their direct use for pure investment properties unless investors plan to live in the property initially

- Loan limits vary by geographic area, with higher limits available in expensive markets that could affect your investment strategy

HomeStyle Renovation Mortgage Benefits

HomeStyle renovation mortgage options might provide more flexibility for real estate investors compared to government-backed alternatives. These conventional loan products often allow investment property financing with different terms and conditions.

- Investment property eligibility makes HomeStyle loans potentially more suitable for traditional real estate investors who don't plan to occupy the property

- Higher loan limits compared to FHA programs could accommodate more expensive properties and extensive renovation projects

- Faster processing times might occur since these loans don't require government oversight and approval processes

- Flexible contractor requirements often allow investors to work with their preferred renovation teams rather than being restricted to approved contractor lists

Financing Home Improvements: Step-by-Step Process

Financing home improvements through renovation loans typically follows a structured process that investors should understand before committing to a project. This systematic approach helps ensure successful loan approval and project completion.

- Property identification and purchase contract negotiation, including renovation contingencies that protect your investment if loan approval fails

- Contractor selection and detailed cost estimates that meet lender requirements for scope of work and material specifications

- Loan application submission with all required documentation, including property appraisals, renovation plans, and financial statements

- Funds disbursement in stages as work progresses, with inspections required before each payment to ensure quality and compliance

- Final inspection and loan conversion to permanent financing once all renovation work meets approved specifications and local building codes

Construction Loan vs. Renovation Loan Comparison

Construction loan vs. renovation loan differences could significantly impact your investment strategy and cash flow management. Understanding these distinctions helps investors choose the most appropriate financing structure for their specific projects.

- Construction loans typically require higher down payments and shorter terms, often converting to permanent financing after project completion

- Renovation loans generally combine purchase and improvement financing from the start, potentially reducing closing costs and administrative complexity

- Interest payment structures differ, with construction loans often requiring interest-only payments during the building phase

- Property requirements vary, as renovation loans work with existing structures while construction loans may finance ground-up development projects

Maximizing Investment Returns Through Strategic Renovation Financing

Maximizing investment returns through strategic renovation financing requires careful analysis of loan terms, renovation costs, and projected property values. Smart investors typically evaluate multiple financing scenarios to determine which approach offers the best risk-adjusted returns. The consolidation of purchase and renovation costs into a single loan might reduce overall interest expenses while simplifying the investment process. However, the success of this strategy often depends on accurate cost estimates, realistic timelines, and thorough market analysis to ensure the finished property meets your target return requirements.

●Conclusion

Home renovation loans represent a potentially powerful tool for real estate investors seeking to streamline their property improvement strategies. While these financing options might not suit every investment scenario, they could offer significant advantages for investors who understand their requirements and limitations.

The key to success often lies in matching the right loan product to your specific investment goals and property type. Whether you're considering FHA 203(k) programs for owner-occupied investments or exploring HomeStyle renovation mortgages for pure investment properties, thorough research and professional guidance typically prove essential.

As you evaluate renovation financing options, consider consulting with experienced mortgage professionals who understand investment property lending. The right financing structure could mean the difference between a profitable renovation project and a costly mistake that impacts your long-term investment success.