The craft beverage industry has seen remarkable growth over the past decade, and small-batch kombucha breweries are no exception. Whether you're a seasoned entrepreneur looking to expand your portfolio or a first-time business owner passionate about fermented beverages, acquiring an existing kombucha operation could be a smart move. But like most business acquisitions, it takes capital — and knowing your business loan options for acquiring a small-batch kombucha brewery is the first step toward making that vision a reality. In this guide, we'll walk through the financing paths most likely to help you close the deal, from government-backed programs to specialized asset-based lending.

Why Kombucha Brewery Acquisitions Require Specialized Financing

Acquiring a small-batch kombucha brewery isn't quite like buying a standard retail business. These operations involve a unique mix of specialized equipment, inventory with active fermentation timelines, health and food safety licensing, and often a loyal but niche customer base. All of these factors affect how lenders evaluate your loan application.

Most traditional banks may view food and beverage manufacturing as a moderate-to-higher risk sector, which means you might face more scrutiny than a borrower in a more conventional industry. That said, lenders who specialize in small business or food production financing tend to have a better understanding of how brewery businesses generate revenue and manage operating cycles.

Before approaching any lender, it helps to have a clear picture of what you're acquiring. This typically includes:

- The business's current revenue and profit margins

- The value and condition of brewing and bottling equipment

- Existing lease agreements or commercial property ownership

- Brand value, recipes, and intellectual property

- Any outstanding liabilities or regulatory compliance issues

Having this information organized not only helps you understand what you're paying for — it also strengthens your loan application considerably.

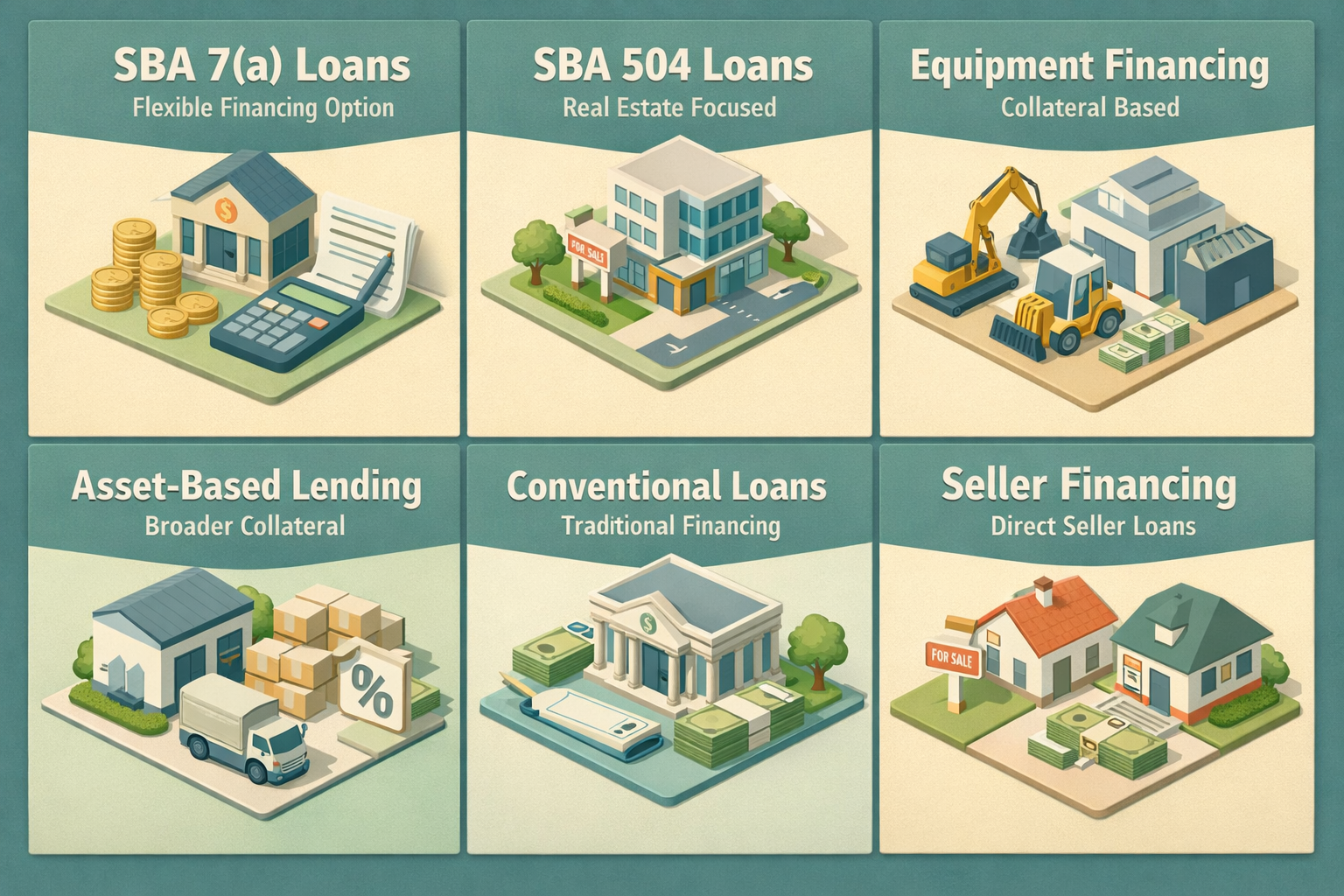

SBA 7(a) Loans: A Popular Path for Business Acquisitions

For many small business owners pursuing an acquisition, the SBA 7(a) loan program is often one of the most accessible and flexible options available. Backed by the U.S. Small Business Administration, these loans are partially guaranteed by the federal government, which reduces the risk for participating lenders and can make it easier for borrowers to qualify.

SBA 7(a) loans may be used for a wide range of purposes, including purchasing an existing business, acquiring commercial real estate, buying equipment, and covering working capital needs — all of which could apply in a brewery acquisition scenario. Loan amounts can potentially reach up to $5 million, which may be more than enough to cover the purchase price of a small-batch kombucha operation, depending on its size and assets.

Some key features of SBA 7(a) loans that make them appealing for acquisition financing include:

- Longer repayment terms — often up to 10 years for business acquisitions, and longer for real estate

- Lower down payment requirements compared to conventional business loans

- Competitive interest rates tied to the prime rate with SBA-set caps

- Flexible use of proceeds covering multiple acquisition costs at once

It's worth noting that SBA loans do come with documentation requirements and a more involved underwriting process. You'll likely need to provide business financial statements, a purchase agreement, a business plan, and personal financial information. Working with an SBA-preferred lender can help streamline this process.

SBA 504 Loans: Best When Real Estate or Heavy Equipment Is Involved

If the kombucha brewery you're acquiring includes the physical building or significant fixed assets like large-scale fermentation tanks, a SBA 504 loan might be worth exploring. This program is specifically designed to help small businesses purchase major fixed assets, and it's structured as a partnership between a Certified Development Company (CDC), a traditional lender, and the borrower.

The typical structure involves the lender financing around 50% of the project cost, the CDC covering up to 40% through a debenture, and the borrower contributing a down payment of roughly 10%. This structure could allow you to acquire significant hard assets with a relatively modest upfront investment.

For a brewery acquisition that involves purchasing commercial real estate — such as the production facility itself — the SBA programs can be particularly advantageous. It may offer below-market, fixed interest rates on the CDC portion of the loan, which can help with long-term cash flow predictability.

Keep in mind that SBA 504 loans are not designed to cover working capital or inventory, so you may need to pair this financing with another loan product if those needs are part of your acquisition plan.

Equipment and Asset-Based Lending for Brewery Acquisitions

Kombucha brewing relies heavily on specialized equipment — fermentation vessels, filtration systems, bottling lines, refrigeration units, and more. In many acquisitions, this equipment represents a substantial portion of the total purchase price. That's where equipment financing and asset-based lending can play a valuable role.

With equipment financing, the equipment itself typically serves as collateral for the loan. This can make it easier to qualify, especially if you have limited business credit history. The loan is generally structured to align with the useful life of the equipment, which means repayment terms could range from a few years to over a decade depending on what's being financed.

Asset-based lending, on the other hand, uses a broader range of business assets — including inventory, accounts receivable, and equipment — as collateral for a line of credit or term loan. For a brewery acquisition, this approach might offer more flexibility in how funds are used across the deal.

Some practical considerations when evaluating these options:

- Get an independent appraisal of the brewing equipment before closing

- Confirm whether the equipment is leased or owned by the current business

- Understand depreciation timelines, as older equipment may limit borrowing capacity

- Ask lenders whether they have experience financing food and beverage manufacturing assets

Conventional Term Loans and Alternative Lenders to Consider

Beyond government-backed programs, conventional term loans from banks, credit unions, and online lenders remain a viable option for brewery acquisition financing. These loans typically offer a lump sum that's repaid over a fixed schedule with interest, and they can be faster to obtain than SBA loans in some cases.

If you have strong personal credit, a solid business track record, and a well-documented acquisition plan, a conventional term loan could give you the capital you need without the additional red tape associated with government programs. However, interest rates and terms will vary significantly between lenders, so comparison shopping is essential.

Online and alternative lenders have also expanded access to business acquisition financing, particularly for borrowers who may not meet the strict requirements of traditional banks. These lenders often move faster and may have more flexible eligibility criteria, though their rates can be higher and repayment terms shorter.

When weighing these options, consider the following:

- What is the total cost of the loan over its full term, not just the interest rate?

- Are there prepayment penalties if you want to pay off the loan early?

- Does the lender have experience with food manufacturing or beverage businesses?

- How quickly do you need to close, and can the lender meet that timeline?

Seller Financing: A Creative Option in Brewery Deals

One often-overlooked option in small business acquisitions is seller financing, where the current owner of the kombucha brewery agrees to carry a portion of the purchase price as a loan. This arrangement can be particularly helpful when buyers have difficulty qualifying for the full amount through traditional channels, or when both parties want to close quickly without waiting for bank approval.

In a seller-financed deal, the buyer makes regular payments directly to the seller over an agreed-upon period, often at a negotiated interest rate. The seller essentially becomes the lender, which means the terms can be more flexible than those offered by institutional lenders.

This structure is sometimes combined with a bank or SBA loan — where the lender covers the majority of the purchase price and the seller carries a smaller note for the remainder. Some SBA programs even allow seller financing as part of the equity injection, under certain conditions.

Of course, seller financing depends entirely on the seller's willingness and financial position. Not every seller will be open to this arrangement, but it's worth raising as part of your negotiation if traditional financing leaves a gap in your funding stack.

Preparing a Strong Loan Application for a Brewery Acquisition Loan

Understanding the business loan options for acquiring a small-batch kombucha brewery is one thing — but getting approved requires preparation. Lenders will want to see that you understand the business you're buying and that you have the financial standing to support repayment.

Here's what a strong brewery acquisition loan application typically includes:

- A detailed business plan — outlining your operational strategy, target market, revenue projections, and how you plan to grow or maintain the acquired business

- Historical financials from the seller — at least two to three years of tax returns, profit and loss statements, and balance sheets

- Personal financial statements — including your credit score, net worth, and any existing liabilities

- A signed letter of intent or purchase agreement — showing the lender that a deal is in progress

- Collateral documentation — especially if the acquisition includes real estate or significant equipment

It's also worth consulting with a business attorney and a CPA experienced in acquisitions before you submit any loan application. Their guidance can help you structure the deal in a way that's both financially sound and lender-friendly.

Finally, don't overlook the importance of your own industry experience. Lenders often feel more confident financing buyers who have a background in food production, beverage manufacturing, or business management. If you're newer to the industry, partnering with an experienced operator or hiring a strong management team could help offset any concerns.

●Conclusion

Acquiring a small-batch kombucha brewery is an exciting opportunity, but it requires careful financial planning and the right lending partner. From SBA 7(a) and 504 loans to equipment financing, conventional term loans, and seller financing, there are several viable paths worth exploring. The best approach will depend on the size and structure of the deal, your personal financial profile, and how quickly you need to move. By understanding your business loan options for acquiring a small-batch kombucha brewery and preparing a thorough application, you'll be in a much stronger position to secure the funding you need and start brewing your next chapter. Ready to explore your options? Connect with a LoanWise lending specialist today to get started.