Purchasing a high-value home in the United States while earning income from another country is more common than many people realize. Investors, executives, and professionals who receive compensation in a foreign currency often find themselves navigating a uniquely complex mortgage landscape — especially when they're pursuing a jumbo loan. Unlike conventional conforming mortgages, jumbo loans carry stricter eligibility requirements, and when you layer in income that fluctuates due to currency exchange rates, the approval process can feel overwhelming. That said, it's entirely possible to qualify. Understanding how to qualify for a jumbo loan with fluctuating foreign currency income begins with knowing what lenders are actually evaluating and how to present your financial profile in the strongest possible way.

What Makes Jumbo Loans Different From Conforming Mortgages

Jumbo loans are mortgage products that exceed the conforming loan limits set by the Federal Housing Finance Agency (FHFA). Because these loans can't be purchased by Fannie Mae or Freddie Mac, lenders assume the full credit risk themselves. That means they tend to apply more rigorous qualification standards than you'd find with a standard conforming loan.

For borrowers with straightforward W-2 income and domestic bank accounts, a jumbo mortgage application is already demanding. Lenders typically look for strong credit scores — often 700 or higher — meaningful cash reserves, and a low debt-to-income (DTI) ratio. Now, imagine adding income that's earned in euros, British pounds, Japanese yen, or another currency that shifts in value relative to the U.S. dollar on a daily basis. The challenge grows considerably.

The core issue is income stability. Lenders want to feel confident that a borrower can sustain their monthly payments over the long term. When income is denominated in a foreign currency income, exchange rate volatility can make it appear inconsistent — even if the borrower's actual financial position is quite secure in their home country. Recognizing this disconnect is the first step toward building a compelling loan application.

How Lenders Evaluate Foreign Currency Income for Jumbo Mortgages

Not all lenders handle foreign currency income the same way. Many traditional banks may decline these applications outright, while portfolio lenders and specialty mortgage companies often have established processes for evaluating non-U.S. income sources. Seeking out a lender experienced with international borrowers is a smart early move.

When lenders do accept foreign currency income, they typically convert it to U.S. dollars for underwriting purposes. Most will use a conservative exchange rate — sometimes an average over a set period rather than the current spot rate — to account for fluctuation risk. This means your qualifying income in USD may be lower than what you actually earn, which is an important planning consideration.

Lenders also look at the consistency of your income over time. Even if the currency value shifts, demonstrating a stable pattern of earnings in your home country's currency can help. Two or more years of income history is commonly expected, similar to how self-employed borrowers are evaluated. If your income has grown steadily, that trend may work in your favor during underwriting review.

Additionally, lenders may request a letter from your employer, a certified public accountant (CPA), or a financial professional in your home country to verify the nature and reliability of your income. For self-employed foreign-income earners, profit-and-loss statements, business licenses, and tax filings from your country of residence may also be required.

Jumbo Loan Foreign Income Documentation You'll Likely Need

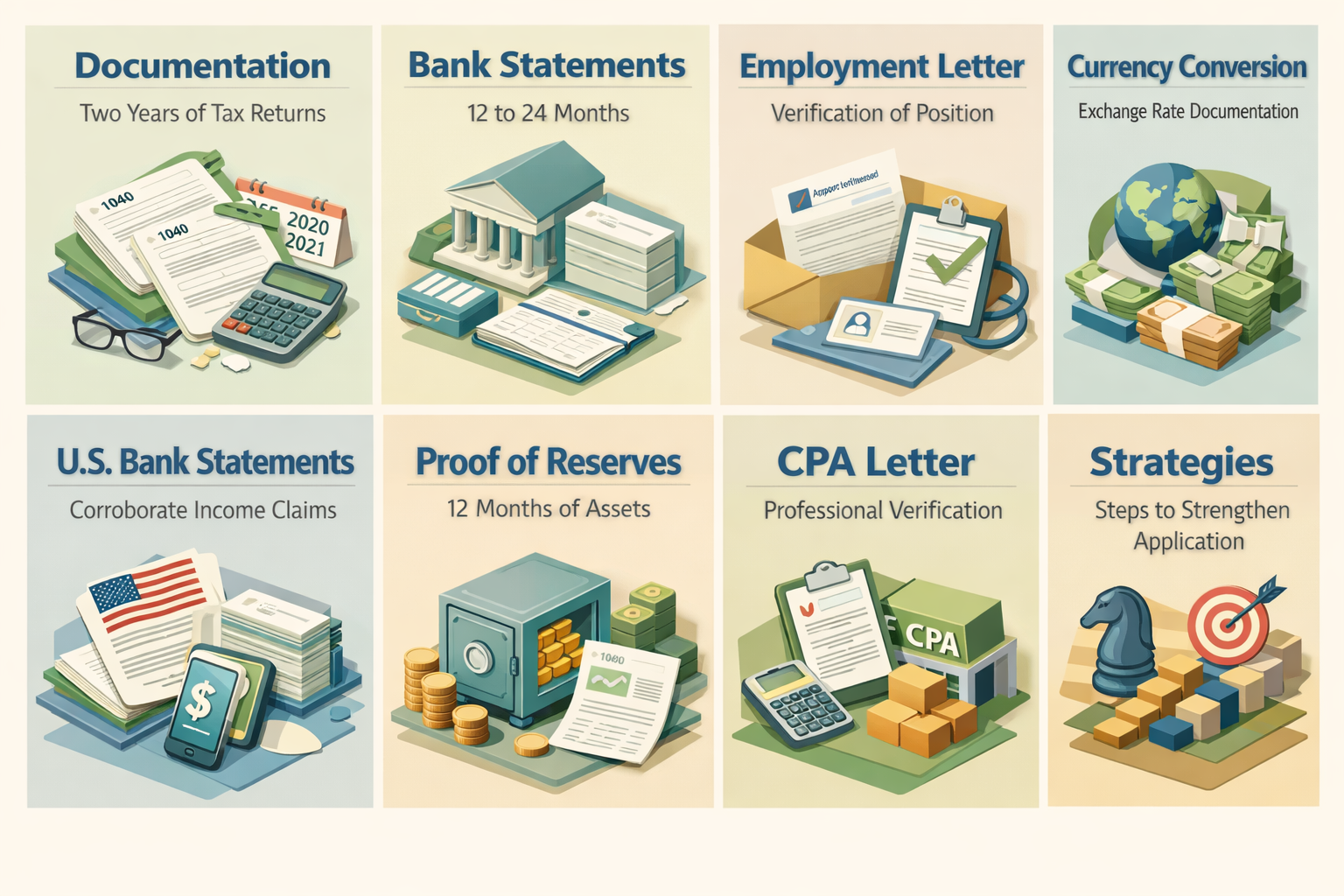

One of the most critical aspects of how to qualify for a jumbo loan with fluctuating foreign currency income is gathering the right documentation. Lenders use these materials to verify your income, assess its stability, and determine how to convert it reliably into U.S. dollar equivalents. Being organized and proactive with paperwork can significantly improve your chances of a smooth approval process.

Here's what lenders commonly request for jumbo loan foreign income documentation:

- Two years of foreign tax returns: These should ideally be translated into English and may need to be accompanied by a certified translation.

- Bank statements (12 to 24 months): Statements from your foreign bank accounts showing consistent deposits help demonstrate income flow and reliability.

- Employment verification letter: A formal letter from your employer written in English, or with a certified translation, confirming your position, salary, and employment terms.

- Currency conversion documentation: Some lenders want to see how exchange rates were calculated and may require documentation from a licensed currency exchange service.

- U.S. bank account statements: If you transfer earnings to a U.S. account, those statements can corroborate your income claims.

- Proof of asset reserves: Jumbo lenders often require 12 months or more of reserves. These assets may need to be in accessible, verifiable accounts.

- CPA letter or financial advisor statement: A professional who can attest to the nature of your income and its continuity adds credibility to your application.

It's worth noting that documentation requirements can vary meaningfully from lender to lender. Working with a mortgage broker who specializes in international borrowers may help you identify which lenders have the most accommodating documentation guidelines for your specific situation.

Strategies to Strengthen Your Jumbo Loan Application as a Foreign-Income Borrower

Beyond gathering the right paperwork, there are several strategic steps you can take to improve your chances of approval. Lenders are ultimately trying to assess risk, and anything you can do to reduce the perceived risk in your file works in your favor.

Make a Larger Down Payment

One of the most effective levers foreign-income borrowers can pull is offering a larger down payment. While many jumbo loans may accept 10 to 20 percent down, putting 25 to 30 percent or more on the table reduces the lender's exposure and may make them more flexible about income verification complexities. A lower loan-to-value (LTV) ratio signals financial strength and reduces underwriting risk.

Build and Demonstrate Substantial Cash Reserves

Jumbo lenders pay close attention to reserves — funds you'll have left over after closing. Foreign-income borrowers may find it helpful to maintain large, verifiable reserves in a U.S.-based account well ahead of the application. This gives lenders a domestic, easily verified cushion and may offset concerns about currency fluctuation impacting monthly payment capacity.

Establish or Strengthen Your U.S. Credit Profile

Some foreign nationals or recent immigrants may have limited U.S. credit history even if they have excellent credit standing abroad. Building a U.S. credit profile — through secured credit cards, U.S. bank accounts, or authorized user status on existing accounts — can take time, but it's worth starting early. A strong credit score helps your entire application.

Consider a Non-QM Jumbo Loan Product

Non-qualified mortgage (Non-QM) loan programs are designed for borrowers who don't fit the standard underwriting mold. Many Non-QM lenders specialize in exactly the kinds of scenarios foreign-income borrowers face. These programs may allow for bank statement qualifying, asset depletion methods, or foreign income acceptance with more flexible documentation standards. Rates may be somewhat higher than traditional jumbo rates, but the access to financing can be well worth it depending on your situation.

The Role of Exchange Rate Volatility in Lender Decision-Making

Currency fluctuation is one of the central challenges in how to qualify for a jumbo loan with fluctuating foreign currency income. Even if your income in your home country is perfectly consistent, a weakening foreign currency can reduce your effective qualifying income in U.S. dollar terms — sometimes significantly.

Lenders typically handle this in one of a few ways. Some may use a historical average exchange rate over a 12- or 24-month period, which smooths out short-term volatility. Others may apply a conservative discount to the current rate to build in a buffer. Still others may evaluate your income across multiple time frames to identify a sustainable baseline.

As a borrower, you can work with this reality by choosing a period to apply when exchange rates are relatively favorable and by presenting multi-year income data that shows consistency despite currency movement. If your income in your home currency has increased over time, lenders may look more favorably on the overall trend even if the converted USD figure has fluctuated.

It's also worth noting that some borrowers in this situation choose to convert a portion of their savings into USD well in advance and park those funds in a U.S. account. This creates a verifiable domestic asset base that lenders can evaluate with more confidence.

Choosing the Right Lender for a Cross-Border Jumbo Mortgage

Not every mortgage lender is equipped to handle the nuances of foreign-income jumbo loan applications. Traditional retail banks with rigid underwriting guidelines may be a poor fit. Instead, consider focusing your search on lenders and mortgage companies that have experience serving international borrowers, foreign nationals, or non-resident aliens.

Portfolio lenders — institutions that hold loans on their own books rather than selling them to the secondary market — often have more flexibility in setting their own underwriting standards. This means they may be more willing to evaluate foreign income on a case-by-case basis rather than forcing your situation into a standard checklist.

Working with a knowledgeable mortgage broker can also be a significant advantage. A broker who regularly places loans for international borrowers will know which lenders are receptive, what documentation formats are preferred, and how to position your income narrative in the most favorable light. This kind of specialized guidance could be the difference between a declined application and a successful closing.

When evaluating lenders, ask directly about their experience with foreign-income borrowers. Inquire whether they've successfully closed jumbo loans for clients earning in specific currencies relevant to your situation. These conversations can quickly reveal whether a lender has genuine expertise or is simply expressing openness without the infrastructure to follow through.

●Conclusion

Understanding how to qualify for a jumbo loan with fluctuating foreign currency income requires patience, preparation, and the right team around you. The path to approval may involve more documentation than a standard mortgage, a larger down payment, and careful lender selection — but it's a path many international borrowers have successfully traveled. By organizing your jumbo loan foreign income documentation thoughtfully, demonstrating income consistency across time, building domestic financial reserves, and partnering with lenders experienced in cross-border lending, you can position yourself as a credible and capable borrower. At LoanWise, we're here to help you navigate the complexity and find a financing solution that fits your unique situation. Reach out to one of our specialists to discuss your jumbo loan options today.