Straw bale homes have been gaining attention among eco-conscious homebuyers who want energy efficiency, natural aesthetics, and lower utility costs. But if you're hoping to finance one of these unique properties, you may have already discovered that the path isn't always simple. Many buyers find themselves asking the same question: how to get a conventional loan for a straw bale home. The good news is that it's possible — it just requires a clear understanding of how lenders evaluate alternative construction, what documentation you'll need, and how to find the right financing partner. This guide walks you through everything you need to know.

What Makes Straw Bale Homes Different From Standard Construction

Straw bale construction uses tightly compressed bales of straw as the primary building material, typically stacked and covered with plaster or stucco on both sides. The result is a home with exceptionally thick walls — often 18 to 24 inches — that provide outstanding insulation and a distinctly natural look and feel.

From a lender's perspective, straw bale homes are considered non-standard or alternative construction. This matters because conventional mortgage programs backed by Fannie Mae and Freddie Mac were largely designed around traditional stick-frame or masonry construction. When a property falls outside those norms, lenders must take extra steps to assess its value, durability, and marketability.

That said, straw bale construction is not inherently flawed or inferior. In fact, research and building science literature suggest that properly built straw bale structures can be highly durable, fire-resistant, and weather-tight. The challenge isn't the construction method itself — it's demonstrating to a lender that the home meets conventional loan standards for safety, soundness, and long-term value.

Why Conventional Mortgage Lenders Hesitate With Alternative Construction

Conventional mortgage lenders — those offering loans that conform to Fannie Mae and Freddie Mac guidelines — rely heavily on comparable sales data when evaluating a property. Appraisers use recent sales of similar homes in the area to determine market value, and this is where straw bale house financing can hit a roadblock.

In many markets, especially suburban or urban areas, there simply aren't enough sold straw bale homes nearby to generate reliable comparable sales. Without solid comps, it's difficult for an appraiser to assign a confident market value, and without a supportable appraisal, lenders may decline the loan or reduce the amount they're willing to finance.

Additional concerns lenders may raise include:

- Marketability: Will future buyers be interested in purchasing the home if the current owner defaults?

- Insurability: Can the borrower obtain standard homeowners insurance on the property?

- Code compliance: Was the home built to local building codes, and is it permitted properly?

- Appraiser familiarity: Does the appraiser have experience valuing non-traditional construction types?

None of these issues are insurmountable, but they do mean that borrowers seeking a conventional mortgage for alternative construction need to be more prepared than a typical homebuyer.

Steps to Qualify: How to Get a Conventional Loan for a Straw Bale Home

Understanding how to get a conventional loan for a straw bale home starts with preparation. Here's a step-by-step breakdown of what the process typically looks like:

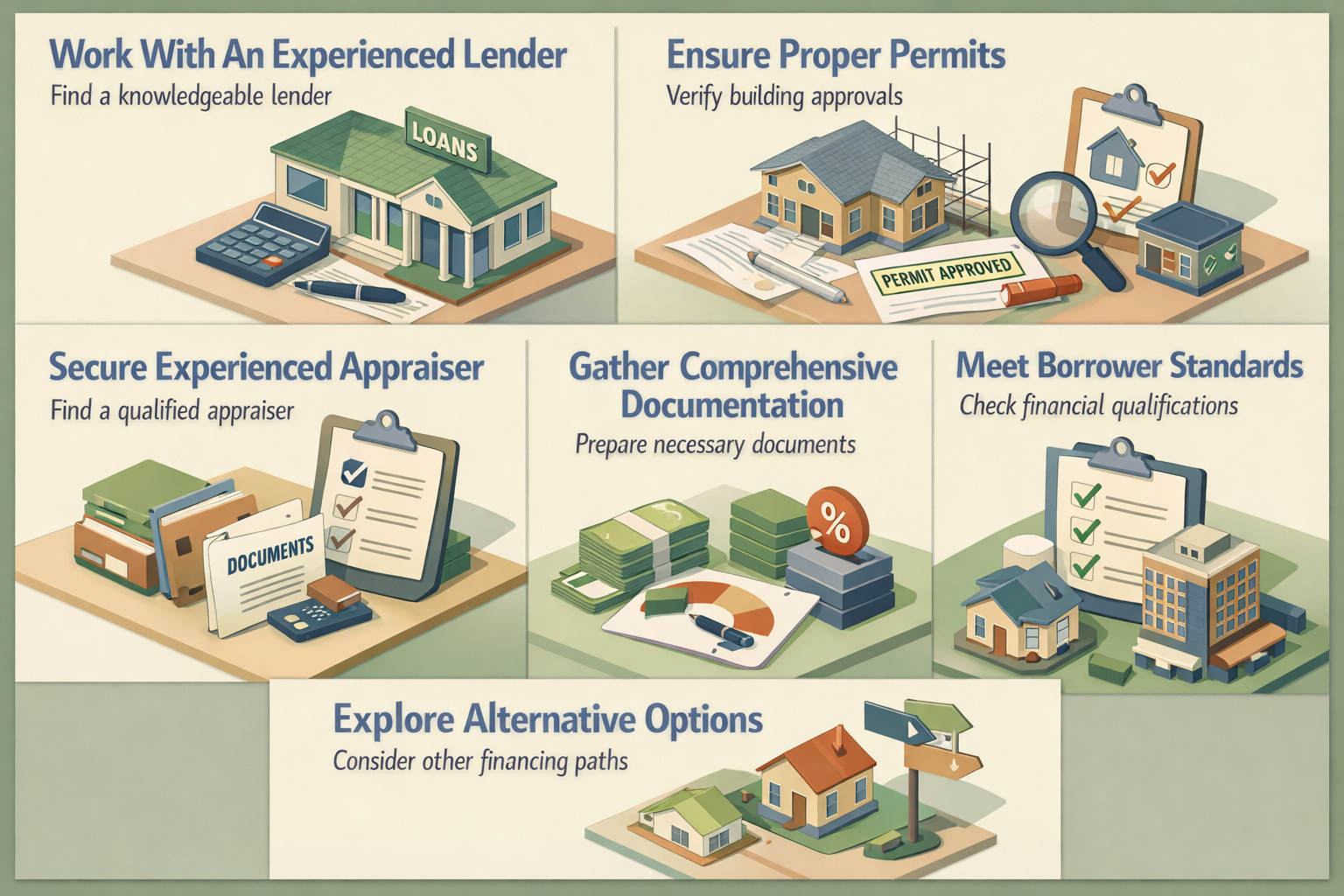

1. Work With an Experienced Lender

Not every mortgage lender has experience with alternative construction. Your first priority should be finding a lender who has previously financed non-traditional homes. Ask directly whether they've worked with straw bale, cob, rammed earth, or other natural building types. A lender with relevant experience will know what documentation to request and how to navigate the appraisal process more effectively.

2. Ensure the Home Is Properly Permitted and Code-Compliant

Conventional loan guidelines typically require that a property meet local building codes and have all required permits. For a straw bale home, this means verifying that the structure was built with the proper approvals and that any inspections were completed. If you're purchasing an existing straw bale home, request a full history of permits and inspections before proceeding.

3. Secure an Appraiser With Alternative Construction Experience

The appraisal is often the most critical hurdle in straw bale house financing. Work with your lender to find a certified appraiser who has experience with alternative or owner-built construction. This appraiser should be comfortable using cost approach valuation methods when comparable sales are limited, and ideally should have documented experience with non-standard building types.

4. Gather Comprehensive Documentation

Lenders may request more documentation than they would for a standard home purchase. Be prepared to provide building plans, material specifications, energy certifications, warranty information from the builder, and any third-party inspections. The goal is to give the lender and appraiser every tool they need to feel confident about the property.

5. Meet Conventional Borrower Qualification Standards

Your personal financial profile matters just as much as the property itself. Conventional loan requirements typically include a credit score of at least 620, a manageable debt-to-income ratio, verifiable income and employment history, and a down payment — often starting at 3% to 5% for primary residences, though a larger down payment may strengthen your application when the property is non-standard.

The Role of the Appraisal in Unique Home Loans

For unique home loans like those involving straw bale construction, the appraisal process deserves special attention. Appraisers have several methods available to them when determining value, and knowing which approach applies to your situation can help you set realistic expectations.

The sales comparison approach — comparing the subject property to recently sold similar homes — is the most common method and carries the most weight in conventional lending. When comparable straw bale sales aren't available in the area, appraisers may need to expand their search radius or use properties with similar energy efficiency and custom features as proxies.

The cost approach estimates value by calculating what it would cost to rebuild the home from scratch, minus depreciation, plus the land value. This method can be very useful for straw bale homes because it reflects the actual construction quality and materials rather than relying on scarce market data. Appraisers experienced in alternative construction are often more comfortable applying this method accurately.

It's worth noting that Fannie Mae guidelines do allow appraisers to use multiple approaches and apply professional judgment when standard comps are limited. Encourage your appraiser to document the construction quality, energy performance, and unique features of the home thoroughly. A well-supported appraisal report can make the difference between loan approval and denial.

Insuring a Straw Bale Home: What Lenders Require

One factor that's sometimes overlooked in the straw bale house financing process is homeowners insurance. Conventional lenders require that the property be insurable before they'll approve a mortgage. For alternative construction homes, obtaining adequate coverage can occasionally be more challenging than for standard homes.

Some mainstream insurance carriers may be unfamiliar with straw bale construction and may decline to cover the property or quote very high premiums. However, specialty insurers and certain regional carriers do offer policies for non-traditional homes. It's wise to research insurance options before you're deep into the mortgage process — discovering an insurance problem late in the closing timeline can cause significant delays.

When shopping for insurance, be prepared to provide documentation about your home's construction method, fire resistance ratings, and any third-party inspections or certifications. Many straw bale homeowners find that the fire resistance of properly plastered straw bale walls actually works in their favor when negotiating with insurers.

Alternative Financing Paths When Conventional Loans Fall Short

Even with the best preparation, some straw bale home purchases may not qualify for a standard conventional mortgage. In those cases, there are other financing options worth exploring.

Portfolio Lenders

Portfolio lenders keep loans on their own books rather than selling them to Fannie Mae or Freddie Mac. Because they're not bound by secondary market guidelines, they often have more flexibility to evaluate unusual properties on a case-by-case basis. Credit unions and community banks are common examples of portfolio lenders who may be willing to finance unique home loans that don't fit conventional molds.

Construction-to-Permanent Loans

If you're building a new straw bale home rather than purchasing an existing one, a construction-to-permanent loan may be worth considering. This type of financing covers the construction phase and then converts into a standard mortgage once the home is complete. Lenders offering these products will still evaluate the finished property's value and your qualifications, but the process may allow for more flexibility during construction.

Owner Financing

In some cases, the seller of a straw bale property may be willing to carry the financing directly. Owner financing arrangements bypass traditional lender requirements entirely, though they typically involve shorter terms and higher interest rates. This can serve as a bridge strategy while the borrower builds equity or waits for the market to generate more comparable sales data.

FHA and USDA Loans

While FHA and USDA loan programs also have property condition requirements, some borrowers have successfully used these government-backed products for alternative construction homes. The key is finding lenders within those programs who are willing to work with non-standard properties. USDA loans in particular may be relevant if the straw bale home is located in a qualifying rural area.

Tips for Strengthening Your Application for Straw Bale Home Financing

Whether you're pursuing a conventional mortgage or an alternative financing path, there are several practical steps that can improve your chances of success when financing a straw bale home.

- Improve your credit profile: A higher credit score gives lenders more confidence in your ability to repay, which can offset some of the uncertainty around a non-standard property.

- Make a larger down payment: Offering 20% or more reduces the lender's risk and may make them more willing to work with a unique property type.

- Get the home professionally inspected: A thorough inspection report from a qualified professional can address concerns about structural integrity, moisture management, and code compliance before the lender asks.

- Document energy performance: If the home has HERS ratings, energy audits, or other certifications, include these in your application package. Energy efficiency can be a selling point that supports value.

- Research your local market: If there are other straw bale or alternative construction homes in your area that have sold recently, gather that data and share it with your appraiser and lender.

- Connect with advocacy groups: Organizations focused on natural building and straw bale construction sometimes maintain resources or lender referrals specifically for buyers of alternative homes.

Being proactive and thorough in your preparation signals to lenders that you're a serious, informed borrower — and that goes a long way when you're working with a property type that falls outside the ordinary.

●Conclusion

Learning how to get a conventional loan for a straw bale home takes more effort than financing a standard property, but it's a goal that many motivated homebuyers have achieved. The keys are finding the right lender, ensuring the property is properly permitted and documented, and working with an experienced appraiser who understands alternative construction. With thorough preparation and a strong personal financial profile, straw bale house financing is well within reach. If conventional options don't fit your situation, portfolio lenders and other creative financing paths may offer the flexibility you need. At LoanWise, we're here to help you explore every option and connect with lenders who understand your vision for a unique, sustainable home.