Essential Mortgage Rate Lock Strategies

Real estate investors face constant uncertainty in today's market, but one area where you can gain control is through strategic mortgage interest rate lock decisions. Whether you're financing a DSCR loan for a rental property or securing bridge financing for your next fix and flip project, understanding how to effectively use rate locks can significantly impact your investment returns and cash flow projections.

The mortgage rate environment in 2026 presents unique opportunities for savvy investors who know when to lock in rates versus when to let them float. With rates projected to remain relatively stable around 6%, the timing of your rate lock decision could mean the difference between a profitable deal and one that barely breaks even.

Smart Timing Tips for Mortgage Interest Rate Lock Decisions

Smart timing tips for mortgage interest rate lock decisions can help you navigate the complex world of investor financing with confidence. The key lies in understanding market conditions and aligning your lock strategy with your investment timeline.

- Monitor Federal Reserve meeting schedules and economic indicators. Fed decisions often influence broader rate movements, so timing your lock around these announcements might help you secure more favorable terms for your investment properties.

- Consider your project timeline when deciding between locking and floating rates. Fix and flip projects with shorter timelines may benefit from immediate locks, while longer-term rental acquisitions might allow for strategic floating during favorable market conditions.

- Evaluate the cost-benefit ratio of rate lock extensions. If your closing gets delayed, understanding extension costs upfront helps you budget accurately and avoid unexpected expenses that could impact your deal profitability.

Float-Down Options That Protect Your Investment Returns

Float-down options that protect your investment returns offer a strategic middle ground between locking in rates and letting them float freely. These features typically allow you to capture better rates if they decline while maintaining protection against increases.

- Understand the costs and conditions of float-down provisions before committing. Many lenders offer these options for an additional fee, so calculate whether the potential savings justify the upfront cost based on your loan amount and market expectations.

- Know the timing restrictions and rate improvement thresholds required. Float-down options often require rates to drop by a minimum amount, such as 0.25% or 0.5%, and may only be exercised within specific timeframes during your lock period.

- Factor float-down costs into your overall financing strategy. While these options provide flexibility, they represent an additional expense that should be weighed against your projected returns and the likelihood of rate improvements during your lock period.

Strategic Lock Period Selection for Different Investment Types

Strategic lock period selection for different investment types requires matching your financing timeline with appropriate lock durations to minimize costs while ensuring rate protection. Different investment strategies benefit from tailored approaches to rate lock periods.

- Choose shorter lock periods for fix and flip projects with aggressive timelines. These investments typically close quickly, so 30 to 45-day locks might provide adequate protection while minimizing lock fees and reducing the risk of needing costly extensions.

- Consider longer lock periods for complex rental property acquisitions. DSCR loans and multi-unit properties often involve more extensive underwriting, making 60 to 90-day locks more appropriate despite higher costs, as they provide security during the longer approval process.

- Align lock periods with your due diligence timeline and contingency removal dates. Planning your lock duration around key milestones in your purchase contract helps ensure you're not paying for rate protection during periods when you might still cancel the transaction.

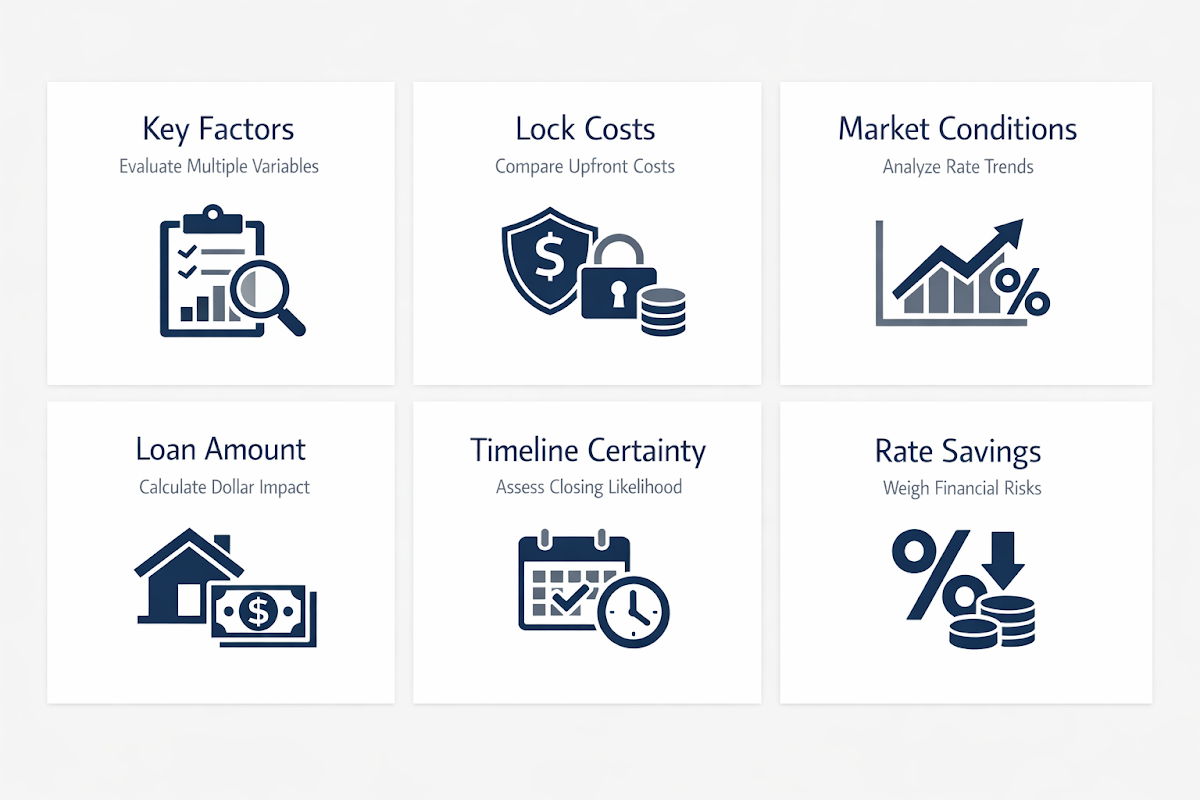

Key Factors to Consider When Locking Mortgage Rates

Key factors to consider when locking mortgage rates extend beyond simple rate comparisons and require careful evaluation of multiple variables that affect your investment success. Understanding these factors helps you make informed decisions that align with your investment goals.

- Current market conditions and rate trajectory predictions: Analyze whether rates appear to be trending upward or downward, and consider economic indicators that might influence future rate movements during your lock period.

- Your loan amount and the dollar impact of rate changes: Calculate how a quarter-point rate change affects your monthly payment and total interest cost over the loan term to determine if lock fees are justified by potential savings.

- Timeline certainty and potential closing delays: Assess the likelihood of your transaction closing on schedule, as delays can result in expensive lock extensions or the need to re-lock at potentially higher rates.

- Lock costs versus potential rate savings: Compare the upfront cost of locking against the financial risk of rates increasing, factoring in both the probability of rate changes and your risk tolerance as an investor.

Essential Steps for Extending Rate Locks During Delays

Essential steps for extending rate locks during delays can help you navigate unexpected timeline changes while minimizing additional costs and protecting your investment financing. Rate lock extensions are common in real estate transactions, and handling them properly is crucial for deal success.

- Contact your lender immediately when delays become apparent: Early communication about potential delays gives you more options and may help you secure better extension terms or avoid rush fees that could impact your deal economics.

- Understand extension fee structures and payment timing: Most lenders charge extension fees as a percentage of the loan amount, and knowing these costs upfront helps you budget appropriately and factor them into your investment calculations.

- Document the reasons for delays and explore alternatives: If delays are due to lender processing issues rather than borrower problems, you may have leverage to negotiate reduced extension fees or other concessions.

- Evaluate whether to extend or re-lock based on current market rates: Sometimes accepting a rate lock expiration and securing a new lock at current market rates could be more cost-effective than paying expensive extension fees, especially if rates have improved.

Common Mortgage Rate Lock Mistakes Investors Should Avoid

Common mortgage rate lock mistakes investors should avoid can save you thousands of dollars and prevent deals from falling apart due to preventable financing issues. Learning from these frequent errors helps you develop a more sophisticated approach to rate management.

- Failing to read and understand lock agreement terms and conditions: Many investors focus solely on the rate and miss important details about extension policies, float-down options, or circumstances that could void their lock, leading to unexpected costs or loss of rate protection.

- Choosing inappropriate lock periods based on unrealistic closing timelines: Overestimating your ability to close quickly or underestimating potential delays can result in expensive extensions or lost locks, both of which can significantly impact your investment returns and deal feasibility.

- Not factoring lock costs into investment property cash flow calculations: Lock fees, extension costs, and potential rate differences should be included in your initial deal analysis to ensure you're making decisions based on accurate financial projections rather than best-case scenarios.

- Making emotional rather than analytical decisions about rate movements: Trying to time the market perfectly or making lock decisions based on fear rather than data often leads to suboptimal outcomes and missed opportunities for better financing costs.

●Conclusion

Mastering mortgage interest rate lock strategies gives real estate investors a competitive edge in today's dynamic market environment. By understanding the nuances of lock periods, float-down options, and extension procedures, you can better protect your investment returns while maintaining the flexibility needed for successful deal execution.

The key to effective rate lock management lies in aligning your strategy with your specific investment goals, whether you're building a rental portfolio through DSCR loans or executing quick fix and flip projects with bridge financing. As market conditions continue to evolve, investors who take a strategic approach to rate locks will be better positioned to capitalize on opportunities while minimizing financing-related risks.

Remember that every investment scenario is unique, and working with experienced mortgage professionals who understand investor needs can help you navigate the complexities of rate locks and secure financing that supports your long-term wealth-building objectives.