Understanding Mortgage Points for Real Estate Investors

Understanding mortgage points represents a critical strategy for real estate investors looking to optimize their financing costs and maximize returns. When you're evaluating DSCR loans, fix and flip financing, or rental property mortgages, the decision to purchase discount points can significantly impact your long-term profitability. Mortgage points allow investors to buy down their interest rate by paying an upfront fee, potentially saving thousands of dollars over the life of the loan. For serious investors managing multiple properties or large loan amounts, this strategy might make the difference between a mediocre deal and an exceptional one.

What Are Mortgage Points and How They Work

What are mortgage points, exactly, and why should real estate investors care? Mortgage points, also called discount points, are fees you pay upfront to your lender to reduce your interest rate. Each point typically costs 1% of your total loan amount and generally reduces your interest rate by 0.25 percentage points, though this can vary by lender and market conditions.

- One point equals 1% of loan amount: On a $400,000 investment property loan, one point costs $4,000

- Rate reduction varies by lender: Most lenders offer 0.125% to 0.25% rate reduction per point purchased

- Points are tax deductible: Investment property mortgage points can often be deducted in the year paid

- Available on most loan types: DSCR loans, conventional investment mortgages, and bridge loans typically offer point options

Key Benefits for Investment Property Financing

The benefits of buying down your interest rate extend far beyond simple monthly payment reduction. For real estate investors, mortgage points can enhance cash flow, improve deal profitability, and provide significant tax advantages. The strategy becomes particularly powerful when you're holding properties long-term or working with larger loan amounts.

- Enhanced cash flow: Lower monthly payments increase net operating income from rental properties

- Improved loan qualification: Reduced debt service ratios might help you qualify for additional financing

- Long-term savings: Interest savings compound over time, potentially saving tens of thousands per property

- Competitive advantage: Lower carrying costs allow more aggressive bidding on profitable deals

When Points Make Financial Sense

Determining when to purchase mortgage points requires careful analysis of your investment timeline, available capital, and overall strategy. The decision isn't always straightforward, and several factors can influence whether paying points aligns with your investment goals.

- Long holding periods: Points typically pay for themselves within 2-5 years depending on rate reduction

- Sufficient liquid capital: Only buy points if it doesn't compromise your reserve funds or next deal

- Stable interest rate environment: Points make less sense if rates are expected to drop significantly

- High loan amounts: Larger loans amplify the absolute dollar savings from rate reductions

Step-by-Step Point Calculation Process

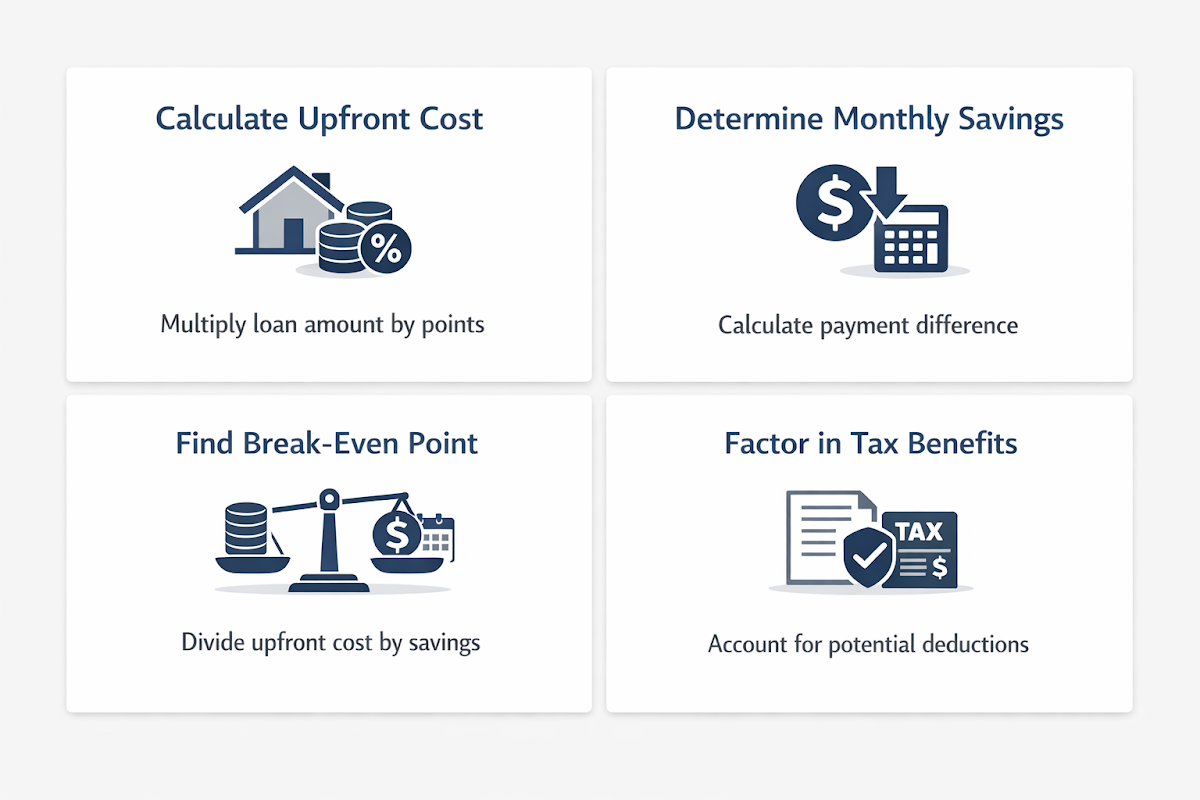

Calculating the cost of mortgage points and determining your break-even timeline requires a systematic approach. Understanding these calculations helps you make informed decisions about whether points align with your investment strategy and timeline.

- Calculate upfront cost: Multiply loan amount by number of points (1 point = 1% of loan amount)

- Determine monthly savings: Calculate payment difference between original rate and reduced rate

- Find break-even point: Divide upfront cost by monthly savings to get break-even period in months

- Consider opportunity cost: Evaluate what else you could do with the upfront point payment

- Factor in tax benefits: Account for potential tax deductions on points paid for investment properties

Strategies for Different Property Types

Different investment strategies require different approaches to mortgage points. How do points affect interest rates across various property types and investment approaches? The answer depends on your specific situation, loan type, and investment timeline.

- Buy-and-hold rentals: Points often make sense due to long holding periods and steady cash flow benefits

- Fix and flip projects: Generally avoid points on short-term bridge loans unless refinancing into permanent financing

- BRRRR strategy properties: Consider points on the permanent financing phase after renovation and refinancing

- Commercial multifamily: Points frequently justify themselves due to large loan amounts and long-term holds

- Vacation rental investments: Evaluate based on seasonal cash flows and expected holding period

Common Mistakes to Avoid

Many real estate investors make costly errors when deciding whether to purchase mortgage points. Understanding these pitfalls can help you make better financing decisions and avoid strategies that might hurt rather than help your investment returns.

- Buying points without sufficient holding period: Don't pay points if you plan to refinance or sell within two years

- Depleting cash reserves: Never compromise your ability to handle repairs, vacancies, or new opportunities

- Ignoring opportunity cost: Consider whether the point payment could generate better returns elsewhere

- Failing to shop around: Different lenders offer varying point costs and rate reductions

- Overlooking loan program differences: Some programs offer better point values than others

Making the Right Decision

The decision to purchase mortgage points should align with your overall investment strategy and financial position. For most successful real estate investors, points make sense on long-term holds with sufficient cash reserves and large enough loan amounts to generate meaningful savings. The key lies in running the numbers for your specific situation and considering all factors, including opportunity costs, tax implications, and your investment timeline. Remember that every deal is different, and what works for one property might not work for another.

●Conclusion

Understanding mortgage points gives real estate investors a powerful tool for optimizing financing costs and improving investment returns. Whether you're financing rental properties through DSCR loans, securing bridge financing for fix and flip projects, or expanding your portfolio, the strategic use of discount points can significantly impact your bottom line. Take time to calculate the costs and benefits for each deal, consider your holding period and available capital, and work with experienced lenders who understand investment property financing. When used correctly, mortgage points can be the difference between good deals and great ones.