Real estate investors seeking financing for rental properties often discover that traditional mortgage qualification methods don't align with their investment strategies. DSCR loan requirements offer a solution by focusing on property cash flow rather than personal income verification. Understanding these requirements can help investors access capital for expanding their rental property portfolios while navigating the unique qualification criteria that make DSCR loans attractive for investment properties.

Understanding DSCR Loan Requirements and Benefits

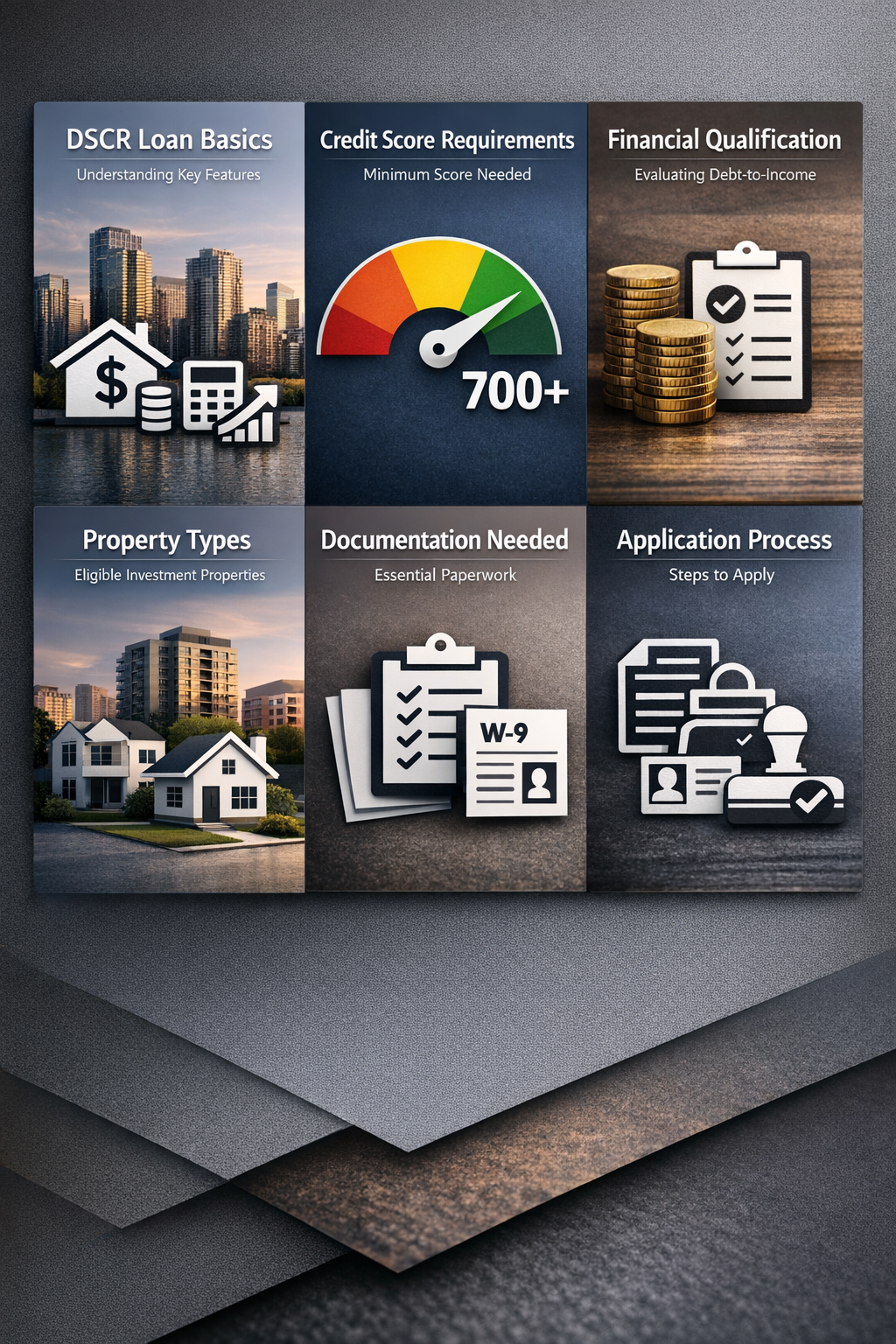

Debt Service Coverage Ratio loans represent a specialized financing approach that evaluates borrowers based on investment property performance rather than traditional income documentation. These loans typically require a minimum credit score of 640, though some lenders may accept scores as low as 620 with compensating factors.

The primary advantage lies in the qualification process, which doesn't require tax returns, W-2s, or employment verification. Instead, lenders focus on the property's rental income potential and the borrower's overall financial stability. This approach particularly benefits self-employed investors, those with complex income structures, or investors seeking to rapidly expand their portfolios.

Down payment requirements generally range from 20% to 25% for most investment properties, with some lenders requiring 30% for certain property types. The loan-to-value ratios typically max out at 75% to 80%, depending on the specific lender and property characteristics.

Credit Score and Financial Qualification Standards

Most lenders establish minimum credit score thresholds between 640 and 680 for DSCR loan approval. Higher credit scores often result in better interest rates and more favorable loan terms, making it worthwhile for investors to optimize their credit profiles before applying.

Beyond credit scores, lenders evaluate debt-to-income ratios, though these calculations differ from traditional mortgages. Many DSCR lenders focus on existing debt obligations rather than employment income, creating opportunities for investors whose rental income isn't easily documented through conventional methods.

Cash reserves play a crucial role in qualification, with most lenders requiring two to six months of mortgage payments in reserve funds. These reserves demonstrate financial stability and the ability to handle potential vacancy periods or unexpected maintenance costs that could impact cash flow.

Property Types and Investment Criteria

DSCR loans accommodate various investment property types, including single-family rentals, condominiums, townhomes, and multi-unit properties up to four units. Some lenders extend financing to larger apartment buildings, though requirements may become more stringent for commercial-sized properties.

Property condition requirements vary by lender, but most require properties to be in rentable condition at closing. Fix-and-flip projects or properties requiring substantial rehabilitation typically don't qualify for standard DSCR loans, though specialized bridge loan products might serve these purposes.

Location restrictions may apply, with some lenders focusing on specific geographic markets or avoiding certain rural areas. Urban and suburban rental markets generally receive more favorable consideration due to stronger rental demand and property value stability.

Debt Service Coverage Ratio Calculations

The debt service coverage ratio calculation forms the cornerstone of loan qualification, measuring the property's ability to generate sufficient income to cover mortgage payments. Most lenders require a minimum DSCR of 1.0, though many prefer ratios of 1.25 or higher for optimal approval odds.

Rental income calculations typically use market rent analysis or existing lease agreements to determine monthly rental income. Lenders may apply vacancy factors ranging from 5% to 10% to account for potential rental interruptions, creating more conservative cash flow projections.

The calculation divides net rental income by total debt service, including principal, interest, taxes, and insurance. Properties generating higher rental yields relative to their debt obligations receive more favorable consideration and may qualify for better interest rates or loan terms.

Documentation and Application Process

The streamlined documentation requirements distinguish DSCR loans from conventional mortgages. Typical documentation includes bank statements showing cash reserves, credit reports, property purchase contracts, and rental property financing analysis or existing lease agreements.

Asset verification becomes particularly important since employment income isn't considered. Lenders may require two to three months of bank statements demonstrating adequate liquidity and financial stability. Investment property experience, while not always required, can strengthen applications and potentially improve loan terms.

The application timeline often moves faster than conventional mortgages due to reduced income verification requirements. Most DSCR loans can close within 30 to 45 days, making them attractive for competitive real estate markets where quick closings provide advantages.

Interest Rates and Loan Terms Structure

DSCR loan interest rates typically run 0.5% to 1.5% higher than conventional mortgage rates, reflecting the increased risk profile of investment property financing. However, these rates often remain competitive compared to other investor loan products, particularly when considering the reduced documentation requirements.

Loan terms commonly include 30-year amortization schedules, though some lenders offer 15-year or interest-only options. Many DSCR loans feature prepayment penalties during the initial years, typically ranging from two to five years, which helps lenders recoup origination costs.

Rate structures may include both fixed and adjustable options, with fixed rates providing payment predictability for long-term rental property strategies. Adjustable rates might offer lower initial rates but introduce interest rate risk that investors must carefully evaluate against their investment timelines.

Strategies for Meeting DSCR Loan Requirements

Investors can improve their qualification odds by focusing on properties with strong rental income potential relative to purchase price. Researching comparable rents and selecting properties in stable rental markets helps ensure adequate debt service coverage ratios.

Building cash reserves before applying strengthens applications significantly. Many successful investors maintain separate accounts for investment property reserves, demonstrating financial preparedness for property management challenges and unexpected expenses.

Working with experienced mortgage professionals who specialize in investor financing can provide valuable guidance through the application process. These professionals understand lender preferences and can help structure deals to meet specific qualification criteria while optimizing terms for long-term investment success.

●Conclusion

DSCR loan requirements offer real estate investors a practical path to financing rental properties without traditional income verification hurdles. By understanding credit score minimums, cash reserve needs, and debt service coverage calculations, investors can position themselves for successful loan approval. The streamlined documentation process and focus on property performance make DSCR loans particularly valuable for building rental property portfolios efficiently. As you consider your next investment property acquisition, evaluating whether you meet these requirements can help determine if DSCR financing aligns with your investment strategy and financial capabilities.