For small business owners and entrepreneurs looking to grow, expand, or invest in commercial property, the U.S. Small Business Administration (SBA) offers two of the most powerful financing tools available: the SBA 7(a) loan and the SBA 504 loan. Both programs are designed to help businesses access capital that might otherwise be difficult to secure through conventional lenders — but they work in very different ways. If you've been wondering which option is right for your situation, you're not alone. Comparing SBA 7(a) and SBA 504 loan terms is one of the most common questions small business owners ask when exploring growth financing. This guide breaks down both programs clearly so you can move forward with confidence.

What Makes SBA Loans Different From Conventional Business Financing

Before diving into program-specific differences, it helps to understand what makes SBA loans stand apart from traditional bank loans. The SBA doesn't lend money directly to businesses. Instead, it partners with approved lenders — banks, credit unions, and non-bank financial institutions — and guarantees a portion of the loan. This government-backed guarantee reduces risk for lenders, which typically allows them to offer more favorable terms to borrowers who may not qualify for standard commercial financing.

SBA loans often come with longer repayment terms, lower down payment requirements, and competitive interest rates compared to many conventional alternatives. They're particularly well-suited for small business owners, startups with limited track records, and entrepreneurs looking to purchase equipment, real estate, or fund working capital. That said, SBA programs do come with eligibility requirements, documentation demands, and in some cases, longer approval timelines. Understanding the specific structure of each program is essential before you apply.

SBA 7(a) Loan Terms: Flexible Financing for a Wide Range of Needs

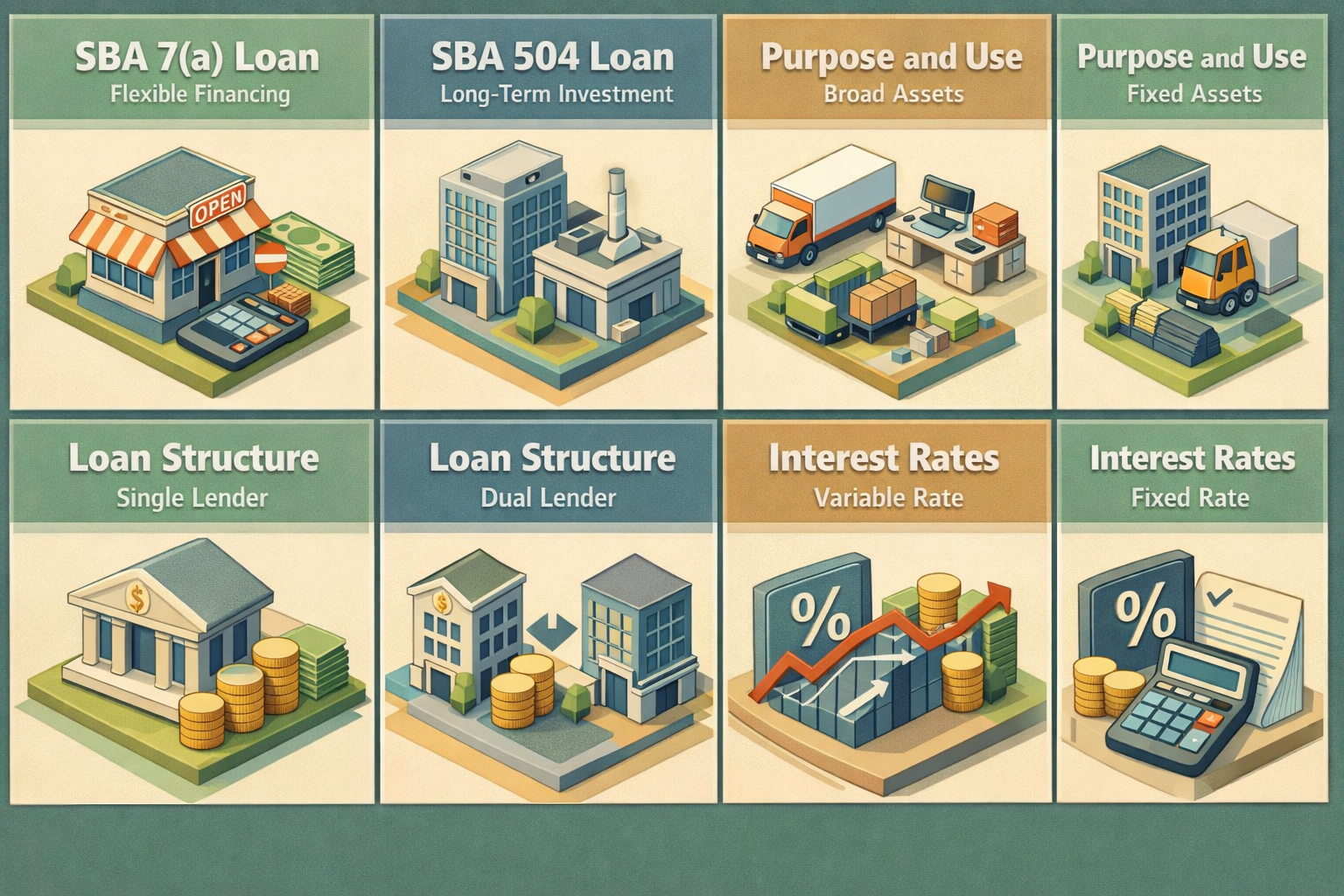

The SBA 7(a) loan is the SBA's flagship and most widely used program. It's designed to be flexible, covering a broad range of business financing needs. Loan amounts may go up to $5 million, and funds can typically be used for working capital, equipment purchases, inventory, business acquisitions, refinancing existing debt, and commercial real estate purchases.

Repayment terms vary based on how the funds are used. Working capital loans may have repayment terms of up to 10 years, while real estate purchases could qualify for terms of up to 25 years. Interest rates on SBA 7(a) loans are generally variable and tied to a base rate — such as the prime rate — plus a lender spread. Fixed-rate options may be available in some cases, though they're less common.

One of the key strengths of the 7(a) program is its versatility. Because it can fund so many different business needs under one loan, it's often the go-to choice for small business owners who need a combination of financing — for example, purchasing a building while also funding working capital. Down payment requirements typically start around 10%, though lenders may require more depending on the borrower's financial profile and the nature of the project.

- Loan amount: Up to $5 million

- Use of funds: Working capital, equipment, real estate, acquisitions, debt refinancing

- Repayment terms: Up to 10 years (working capital), up to 25 years (real estate)

- Interest rates: Typically variable, tied to prime rate plus a spread

- Down payment: Generally starting around 10%

SBA 504 Loan Terms: Built for Long-Term Asset Investment

The SBA 504 loan terms program is structured quite differently from the 7(a). It's specifically designed for the purchase of major fixed assets — primarily owner-occupied commercial real estate and large equipment. If your goal is to buy a building, construct a facility, or acquire heavy machinery that will anchor your operations for years to come, the 504 program may be worth a close look.

The SBA 504 loan works through a three-party structure. A conventional lender (typically a bank) provides approximately 50% of the project cost, a Certified Development Company (CDC) — a nonprofit intermediary authorized by the SBA — provides about 40% backed by an SBA debenture, and the borrower contributes the remaining 10% as a down payment. In some cases, the borrower's contribution may be higher for special-use properties or newer businesses.

One of the most attractive features of the 504 program is its long-term fixed interest rate on the CDC portion. This rate is tied to U.S. Treasury rates and is set at the time of funding, which can offer meaningful protection against rate fluctuations over time. Repayment terms on the 504 are typically 10, 20, or 25 years for real estate, and 10 years for equipment. Total project financing through the 504 can reach up to $5.5 million per project in standard cases, and potentially higher for qualifying manufacturing businesses or energy-efficiency projects.

- Loan structure: 50% bank / 40% CDC (SBA-backed) / 10% borrower

- Use of funds: Owner-occupied commercial real estate, large equipment, construction

- Repayment terms: 10, 20, or 25 years (real estate); 10 years (equipment)

- Interest rates: Fixed rate on CDC portion, tied to U.S. Treasury rates

- Maximum SBA debenture: Generally up to $5.5 million (standard projects)

Key Differences: SBA 7(a) vs 504 Loan Program Comparison

When you put these two programs side by side, the differences become clearer — and so does the decision-making process. Here's a direct SBA loan program comparison across several important dimensions:

Purpose and Use of Funds

The most fundamental difference is in how the funds can be used. The SBA 7(a) is broadly flexible — it can fund working capital, equipment, business acquisitions, and real estate all under one loan. The SBA 504, by contrast, is narrowly focused on long-term fixed assets. You cannot use a 504 loan for working capital, inventory, or debt refinancing. If your financing needs go beyond real estate or major equipment, the 7(a) is likely the more practical choice.

Loan Structure and Lender Involvement

With an SBA 7(a) loan, you're dealing primarily with a single lender. With an SBA loan program comparison perspective, the 504 has you coordinating between a bank and a CDC, which adds a layer of complexity but also unlocks certain benefits — particularly the fixed-rate structure on the CDC portion. Some borrowers find the dual-lender coordination a manageable trade-off for the rate certainty the 504 provides.

Interest Rate Structure

This is one of the most significant differences. SBA 7(a) rates are generally variable, meaning your monthly payments could change over time as interest rates shift. The SBA 504 program offers a fixed rate on the CDC portion, which can make long-term budgeting more predictable. For business owners making a 20 or 25-year commitment to a commercial property, rate stability can be a compelling advantage.

Down Payment Requirements

Both programs may allow down payments starting around 10%, which is lower than what many conventional commercial lenders require. However, the 504's structured contribution model means the borrower's equity injection is embedded into the deal structure from the start. Some scenarios — such as special-use properties or businesses in operation for less than two years — may require higher contributions under both programs.

SBA Loan Eligibility for Each Program: What Borrowers Need to Know

Understanding SBA loan eligibility for each program is a critical step before applying. While both programs share some baseline SBA eligibility requirements, there are important distinctions worth noting.

General SBA Eligibility Requirements

For both programs, your business must operate for profit, be based in the United States, and meet SBA size standards — which vary by industry but are generally defined by annual revenue or number of employees. Businesses in certain industries, such as gambling, lending, and some real estate ventures, may be ineligible. You'll also need to demonstrate that you've sought financing through other means and were unable to secure it on reasonable terms without SBA assistance.

SBA 7(a) Eligibility Highlights

The 7(a) program has relatively broad eligibility, which contributes to its popularity. Startups and established businesses may qualify, though lenders will typically look closely at your credit history, business cash flow, and personal financial background. A credit score of at least 680 is commonly cited as a baseline for consideration, though individual lenders may have their own standards. Collateral requirements vary — smaller loans may require less, while larger amounts typically require business or personal assets as security.

SBA 504 Eligibility Highlights

The 504 program has a few more specific requirements. Your business must have a tangible net worth of less than $20 million and average net income of less than $6.5 million after federal taxes for the preceding two years. Additionally, the project must meet a job creation or community development goal — for example, creating or retaining one job for every $75,000 of SBA loan eligibility financing provided (or $120,000 for manufacturers). These public policy requirements reflect the 504's mission to drive economic development, not just facilitate real estate transactions.

When to Use SBA 7(a) vs 504: Matching the Program to Your Goals

Knowing when to use SBA 7(a) vs 504 often comes down to what you're trying to accomplish and how your financing needs are structured. Here are some common scenarios to help guide your thinking:

Choose SBA 7(a) If You Need:

- A flexible loan that covers multiple business needs at once

- Working capital alongside a property or equipment purchase

- Financing for a business acquisition

- A simpler single-lender structure

- Faster access to funds in some cases through SBA Express or Preferred Lender programs

Consider SBA 504 If You Are:

- Purchasing or constructing owner-occupied commercial real estate

- Investing in major equipment with a long useful life

- Prioritizing long-term rate certainty on a fixed-rate structure

- Comfortable coordinating with both a bank and a CDC

- A business that can meet the job creation or public policy goals of the program

It's also worth noting that in some cases, businesses use both programs in tandem for different aspects of a larger project — though this is less common and requires careful coordination with your lenders and advisors. Consulting with an SBA-approved lender or a financial advisor who specializes in small business financing can help you map the right program to your specific situation.

●Conclusion

Choosing between these two programs is one of the most impactful financing decisions a small business owner can make. Comparing SBA 7(a) and SBA 504 loan terms reveals that both offer meaningful advantages — but they're built for different purposes, different borrowers, and different stages of business growth. The 7(a) shines for its flexibility and broad applicability, while the 504 delivers powerful long-term value for businesses committed to owning their physical assets with rate stability. The best starting point is always a candid conversation with a qualified SBA lender who can evaluate your financials, your goals, and the specific program requirements that apply to your situation. At LoanWise, we're here to help small business owners and entrepreneurs navigate the lending landscape with clarity and confidence. Ready to explore your SBA loan options? Connect with our team today and take the next step toward building the business you've envisioned.