For small business owners and entrepreneurs, few challenges are as predictable — yet as stressful — as managing inventory ahead of peak season. Whether you run a retail shop, an e-commerce store, or a product-based business, the pressure to stock up before demand surges can stretch your cash flow to its limits. That's where business loan options for seasonal inventory needs come in. The right financing strategy could mean the difference between capturing holiday revenue and missing out entirely. In this guide, we'll walk through the most practical loan solutions available, how they work, and what you should consider before applying.

Why Seasonal Inventory Financing Matters for Small Businesses

Most businesses experience some level of seasonal fluctuation, but for retailers, wholesalers, and product-driven companies, those swings can be dramatic. A toy store might generate the majority of its annual revenue in the fourth quarter. A garden supply shop may see its busiest months in spring. A swimwear brand could peak sharply in early summer.

The challenge is that inventory must be purchased before the revenue arrives. Suppliers typically require payment weeks or even months in advance, which means businesses often face a cash flow gap right when they need resources the most. Without adequate financing, a business might understock, miss sales opportunities, and fall behind competitors who were better prepared.

Financing retail inventory fluctuations isn't just about survival — it's a growth strategy. When you have the capital to stock confidently, you can negotiate better bulk pricing with suppliers, offer a wider product selection, and build customer loyalty during high-traffic periods. Understanding your financing options well in advance is one of the smartest moves a seasonal business owner can make.

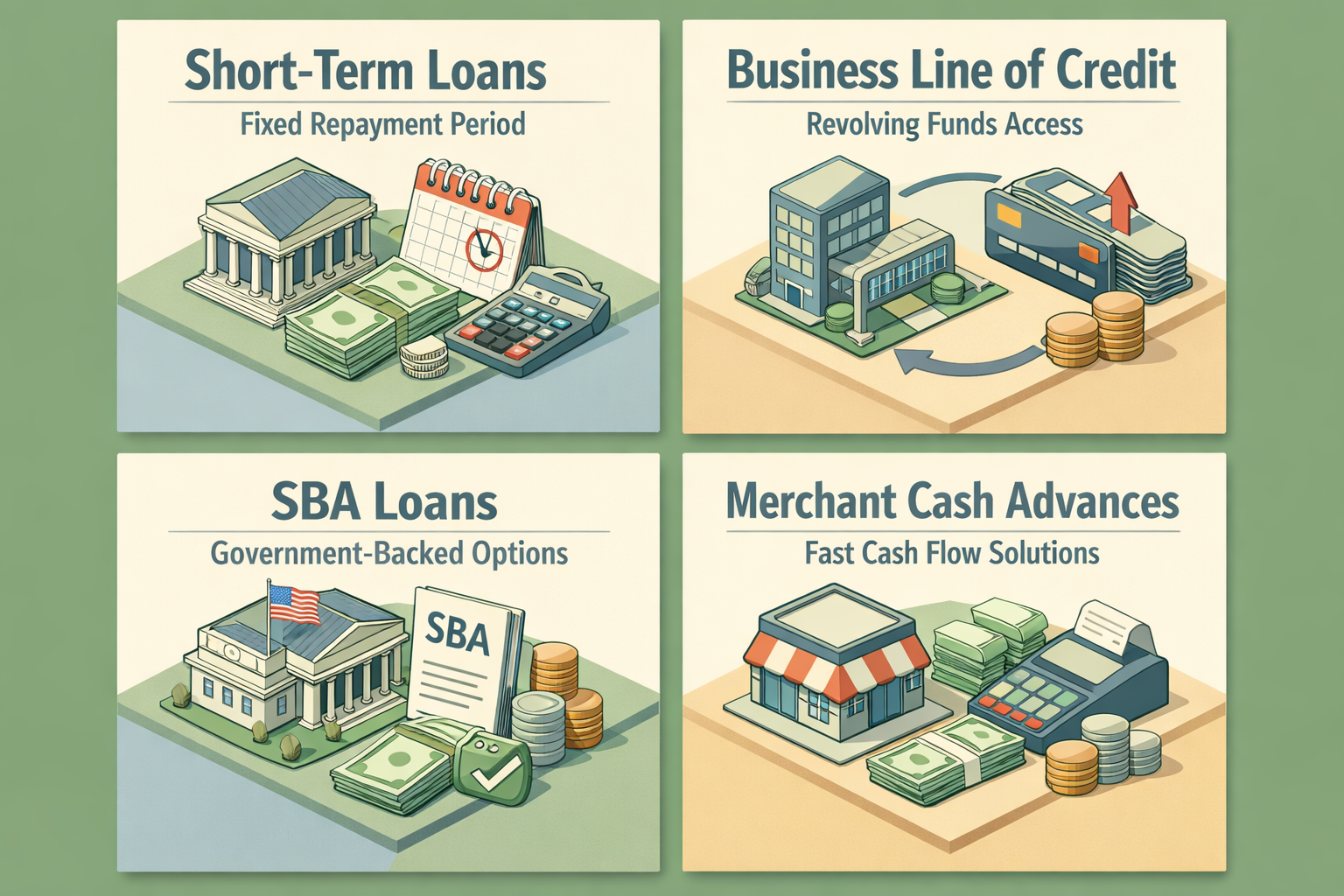

Short-Term Loans: A Direct Path to Peak Season Inventory Capital

Short-term loans for seasonal stock are among the most straightforward financing tools available to small business owners. These loans typically offer a lump sum of capital that you repay over a fixed period — often ranging from three to eighteen months — making them well-suited for inventory purchases tied to a specific selling window.

Many online lenders and community banks offer short-term business loans with relatively fast approval timelines. If you need capital quickly before a peak season begins, this speed can be a significant advantage. Approval may depend on your business's revenue history, credit profile, and time in operation.

Keep in mind that short-term loans often carry higher interest rates than longer-term products. That said, if your seasonal sales are strong enough to cover the cost of borrowing and still generate profit, the math may work well in your favor. It's worth running the numbers carefully with a financial advisor or lending specialist before committing.

What to Look for in a Short-Term Seasonal Loan

- Flexible repayment schedules that align with your revenue cycle

- Fast funding timelines so capital arrives before your busy season begins

- Transparent fee structures with no hidden origination or prepayment penalties

- Loan amounts that match your actual inventory purchasing needs

Business Lines of Credit: Flexible Seasonal Working Capital Loans

A business line of credit is one of the most versatile tools for managing seasonal working capital loans needs. Unlike a term loan, a line of credit gives you access to a revolving pool of funds that you can draw from as needed and repay over time. You only pay interest on what you actually use, which makes it an efficient option for businesses with unpredictable inventory timing.

For seasonal businesses, a line of credit could act as a financial safety net. You might draw funds in October to stock up for the holiday rush, repay most of it by January using holiday revenues, and then let the credit line sit dormant until the next cycle begins. This revolving structure can save money compared to taking out a new loan each season.

Qualifying for a business line of credit typically requires a solid credit history, demonstrated revenue, and some time in business. Lenders may also look at your accounts receivable and overall financial health. If you're just starting out, securing a smaller line and building a track record over time might be the most practical approach.

SBA Loans and Their Role in Seasonal Business Financing

Small Business Administration (SBA) loan programs are backed by the federal government and offered through approved lenders. While SBA loans are often associated with long-term financing, certain programs may be appropriate for seasonal inventory needs — particularly if you're planning ahead and have some lead time before your peak season.

The SBA 7(a) loan is the most common option and can be used for working capital, including inventory purchases. It may offer competitive interest rates and longer repayment terms compared to conventional short-term products. However, the application process tends to be more involved, and funding timelines can be longer — sometimes several weeks or more.

For businesses that consistently rely on seasonal capital, establishing an SBA-backed relationship early in the year — before the rush — could be a smart planning move. Some lenders familiar with seasonal businesses may also offer seasonal payment structures, where repayments are lighter during off-peak months and heavier during high-revenue periods.

Is an SBA Loan the Right Fit for Your Peak Season Needs?

- Best suited for businesses with advance planning time before peak season

- May offer lower rates than alternative lenders for qualified borrowers

- Requires stronger documentation including tax returns, financial statements, and a business plan

- Could work well for established seasonal businesses with a proven revenue track record

Merchant Cash Advances and Invoice Financing for Fast Inventory Capital

When time is short and traditional lenders aren't moving fast enough, some business owners turn to alternative financing products like merchant cash advances (MCAs) or invoice financing to bridge seasonal cash flow gaps.

A merchant cash advance provides a lump sum in exchange for a percentage of your future credit card or debit card sales. Repayment happens automatically as customers pay, which means your payments naturally slow down during slower months. This structure could appeal to businesses with consistent card-based sales, though the effective cost of borrowing is often higher than traditional loans.

Meanwhile, invoice financing — sometimes called accounts receivable factoring — allows you to unlock cash tied up in unpaid customer invoices. If your business sells to retailers or wholesalers on net-30 or net-60 terms, this tool could free up working capital without taking on new debt in the traditional sense. You essentially receive a portion of the invoice value upfront, with the remainder (minus fees) paid once your customer settles.

Both options tend to prioritize speed and accessibility over cost efficiency. They may be worth considering for short-term gaps, but business owners should weigh the total cost carefully before proceeding.

How to Strengthen Your Loan Application Before Peak Season

No matter which financing product you're considering, lenders will evaluate your business's creditworthiness before approving funds. Preparing your application well in advance — ideally months before your peak season — could significantly improve your chances of approval and help you secure better terms.

Here are some practical steps to take before you apply for business loan options for seasonal inventory needs:

- Review your business credit report and address any errors or outstanding issues that could lower your score.

- Organize your financial statements, including profit and loss reports, balance sheets, and tax returns from the last two to three years.

- Document your seasonal revenue patterns clearly — lenders want to see that you understand your business cycle and have a repayment plan.

- Reduce existing debt where possible to improve your debt-to-income ratio before applying.

- Build relationships with lenders early rather than scrambling for capital once peak season is weeks away.

Entrepreneurs who treat loan preparation as an ongoing business practice — rather than a reactive measure — tend to have a smoother borrowing experience and access to more competitive products.

●Conclusion

Seasonal demand is a reality for countless small businesses across retail, agriculture, hospitality, and beyond. The good news is that there's a growing range of business loan options for seasonal inventory needs designed to meet exactly this challenge. From short-term loans and revolving lines of credit to SBA programs and alternative financing tools, today's lending market offers more flexibility than ever before.

The key is to start planning early, understand your cash flow cycle clearly, and match the right financing product to your specific situation. If you're unsure where to begin, speaking with a knowledgeable lending specialist can help you cut through the complexity and find a solution that keeps your shelves stocked and your business growing. At LoanWise, we're here to help you navigate your options with confidence — reach out today to explore what's available for your business.