Running a seasonal tourism business comes with its own rhythm — peak months bring strong cash flow, while the off-season can feel quietly uncertain. When you add an adjustable-rate mortgage (ARM) to that picture, the financial stakes can feel even higher. Rate adjustments don't wait for your busy season. They arrive on their own schedule, and they can significantly change your monthly obligations. That's why exploring the best options for refinancing an ARM mortgage with a seasonal tourism business is such an important step for property owners in this situation. Whether you own a vacation rental, a bed-and-breakfast, or a hospitality-focused commercial property, there are real strategies available to help you move toward a more stable and manageable mortgage structure.

Why ARM Refinancing Is Especially Urgent for Hospitality Property Owners

Adjustable-rate mortgages typically start with a lower introductory interest rate, which can be appealing when you're launching or expanding a tourism-related property. However, once the fixed period ends, your rate adjusts periodically based on a market index — and that adjustment may not align with your business's financial calendar.

For seasonal tourism operators, this mismatch can create real pressure. If your revenue is concentrated in summer or winter months, an unexpected rate increase during the shoulder season could strain your cash reserves. Unlike a salaried borrower who receives steady paychecks year-round, you may have months where income is minimal, making higher mortgage payments particularly difficult to absorb.

Beyond the immediate cash flow concern, ARM loans carry long-term uncertainty. Caps on rate increases do offer some protection, but over the full loan term, a variable rate mortgage could expose you to significantly higher costs than a fixed-rate alternative. That uncertainty alone is a strong reason to evaluate your refinancing options sooner rather than later.

Understanding How Lenders View Seasonal and Fluctuating Income

One of the biggest hurdles in ARM refinance seasonal income is demonstrating consistent, qualifying income to a lender. Traditional mortgage underwriting tends to favor borrowers with stable, monthly earnings. When your business earns most of its revenue in a few concentrated months, lenders may scrutinize your financial picture more carefully.

Most conventional lenders will want to see at least two years of self-employment income history, typically verified through federal tax returns. They'll often average your net income across those two years to determine a qualifying figure. If one year was significantly stronger than another — which is common in tourism — the averaged amount may be lower than your most recent earnings suggest.

It's also worth noting that business deductions, while beneficial for tax purposes, can reduce your reported net income and therefore your qualifying income for a mortgage. This is one of the more nuanced challenges that tourism business owners face when refinancing. Working with a mortgage professional who understands self-employed and non-QM borrower profiles can make a meaningful difference in how your application is structured and presented.

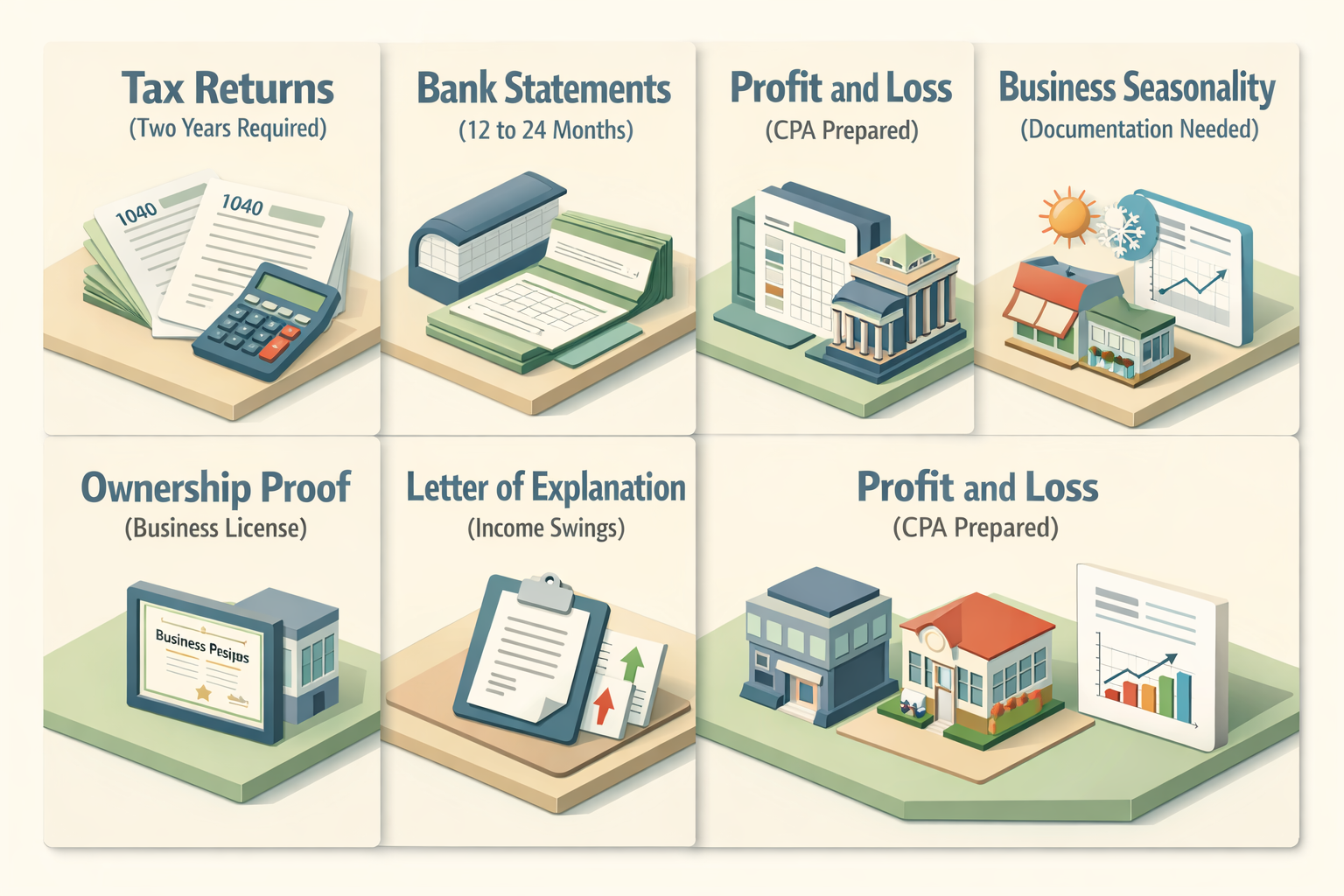

- Two years of tax returns are typically required for self-employed borrowers

- Bank statement loans may allow you to use 12 to 24 months of deposits as income evidence instead

- Profit and loss statements prepared by a CPA can supplement your application

- Business and personal statements may both be reviewed depending on your loan type

Fixed-Rate Refinancing: The Stability Anchor for Tourism Property Owners

The most straightforward of the best options for refinancing an ARM mortgage with a seasonal tourism business is converting to a fixed-rate mortgage. A fixed-rate loan locks in your interest rate for the entire loan term — typically 15, 20, or 30 years — so your principal and interest payment never changes based on market conditions.

For a tourism business owner managing fluctuating monthly revenue, this kind of predictability is invaluable. You'll know exactly what your mortgage payment will be in January just as clearly as you know what it will be in July. That certainty allows for more accurate budgeting during off-peak months and removes the anxiety of potential rate spikes.

Conventional fixed-rate loans backed by Fannie Mae or Freddie Mac are often the first choice for borrowers with strong credit and documented income. If your credit score is solid and your tax returns show sufficient qualifying income, this may be the most cost-effective path. Rates and terms will vary based on your credit profile, loan-to-value ratio, and current market conditions, so it's important to shop multiple lenders and compare offers carefully.

Non-QM and Bank Statement Loans Built for Variable Rate Mortgage Situations

If your tax returns don't fully capture the strength of your tourism business income, non-qualified mortgage (non-QM) products may offer a practical alternative. These loans fall outside the standard guidelines set by government-sponsored enterprises, which gives lenders more flexibility in how they verify income and assess creditworthiness.

Bank statement loans are one of the most commonly used non-QM products for self-employed borrowers. Instead of relying solely on tax returns, lenders review 12 or 24 months of business or personal bank statements to calculate average monthly deposits. For a seasonal operator who brings in strong revenue during peak periods, this method may reflect actual cash flow more accurately than tax-based income averaging.

Asset depletion loans are another option worth exploring. If you've accumulated significant savings, investments, or retirement assets, some lenders may allow those assets to be converted into a qualifying monthly income figure. This can be particularly useful for tourism property owners who have built up reserves over time but show modest income on paper due to business deductions.

Keep in mind that non-QM loans typically come with slightly higher interest rates than conventional products. However, for borrowers who can't qualify through traditional channels, they can be a bridge to refinancing out of an unpredictable ARM and into something more manageable.

Timing Your Tourism Business Mortgage Refinance for Maximum Advantage

Timing matters in any refinance, but it carries extra weight when your income is seasonal. Applying during or just after your peak revenue season may give you the strongest financial snapshot possible. Your bank balances will likely be higher, your cash flow statements will look more favorable, and you may be better positioned to cover closing costs without stretching your reserves.

It's also wise to begin the refinance process before your ARM's fixed period expires or before a scheduled rate adjustment. Once your rate adjusts upward, your monthly payment increases — and that can affect your debt-to-income ratio, which lenders evaluate carefully. Proactively refinancing while your current rate is still low may help you qualify more comfortably.

Additionally, monitoring broader interest rate trends can help you decide when to move. While no one can predict market movements with certainty, refinancing when rates are relatively favorable could reduce your long-term interest costs meaningfully. A mortgage advisor familiar with tourism business mortgage scenarios can help you weigh these timing factors against your personal financial goals.

Preparing Your Financial Documents to Strengthen Your Refinance Application

Strong preparation is one of the most effective tools a seasonal borrower has. Lenders need to feel confident about your ability to repay the loan, and the documentation you provide tells that story. The more clearly and completely you present your financial situation, the smoother the underwriting process is likely to be.

Here's a practical checklist of documents that may be requested during a refinance application:

- Two years of personal federal tax returns including all schedules

- Two years of business tax returns if you operate through an LLC, S-Corp, or partnership

- 12 to 24 months of bank statements for both personal and business accounts

- A current profit and loss statement ideally prepared or reviewed by a licensed CPA

- Documentation of business seasonality such as booking records, revenue reports, or industry letters that explain the cyclical nature of your income

- Proof of business ownership such as a business license or articles of incorporation

- A letter of explanation if there are significant income swings between years

Being proactive and organized not only speeds up the process but also signals to underwriters that you're a serious and responsible borrower. If gaps or inconsistencies do exist in your records, addressing them upfront with a clear explanation is far better than having a lender discover them mid-process.

Working with the Right Lender for Your Seasonal Income Refinance

Not every lender is equally equipped to handle the nuances of a tourism business mortgage refinance. Large retail banks may apply rigid qualification standards that don't accommodate seasonal cash flow patterns. Mortgage brokers and specialty lenders, on the other hand, often have access to a wider range of loan products — including non-QM options — and may have more experience working with self-employed and hospitality-sector borrowers.

When evaluating lenders, consider asking the following questions:

- Do you offer bank statement loans or asset depletion programs?

- How do you treat seasonal income when calculating my qualifying amount?

- Are you familiar with hospitality or tourism-sector borrowers?

- What are your typical timelines from application to closing?

- What are your rate lock options, and how long can I lock in a rate?

A lender who asks thoughtful questions about your business model and income cycle is likely a better fit than one who applies a one-size-fits-all approach. The best options for refinancing an ARM mortgage with a seasonal tourism business often depend just as much on who you work with as on which loan product you choose. A knowledgeable mortgage advisor can help you match your financial profile with the right program and lender from the start.

●Conclusion

Refinancing an adjustable-rate mortgage when you run a seasonal tourism business isn't a simple checkbox exercise — it requires strategy, preparation, and the right partners. From fixed-rate conversions to non-QM bank statement programs, there are meaningful options available for borrowers who know where to look and how to present their financial story. The key is to start early, get your documents in order, and work with a lender who understands the seasonal nature of your income. If you're ready to explore your options, speaking with a mortgage specialist at LoanWise could be your first step toward replacing rate uncertainty with long-term financial stability.