When you're shopping for a home loan, one of the first decisions you'll face is choosing between a fixed-rate mortgage and an adjustable-rate mortgage. For many homebuyers, the idea of a rate that can change over time might seem a little unsettling. But an adjustable-rate mortgage could actually be a smart financial move — depending on your goals, your timeline, and your comfort with some degree of uncertainty. In this guide, we'll break down exactly how these loans work, what the risks and rewards look like, and how to decide whether this type of financing fits your situation.

Understanding How an Adjustable-Rate Mortgage Works

An adjustable-rate mortgage, commonly called an ARM, is a home loan where the interest rate can change periodically after an initial fixed-rate period. Unlike a fixed-rate mortgage — where your rate stays the same for the entire life of the loan — an ARM starts with a set rate for a defined period and then adjusts based on a financial index plus a margin set by the lender.

You'll often see ARMs described with two numbers, such as a 5/1 ARM or a 7/6 ARM. The first number tells you how many years the initial fixed rate lasts. The second number tells you how often the rate adjusts after that. So a 5/1 ARM keeps the same rate for five years and then adjusts once per year. A 7/6 ARM holds the rate steady for seven years and adjusts every six months after that.

The adjustment itself is tied to a benchmark index — often the Secured Overnight Financing Rate (SOFR), which has largely replaced the older LIBOR index in recent years. The lender adds a fixed margin on top of the index to determine your new rate. Because these indexes fluctuate with broader economic conditions, your monthly payment could go up or down after the fixed period ends.

Rate Caps and Consumer Protections Built Into ARM Loans

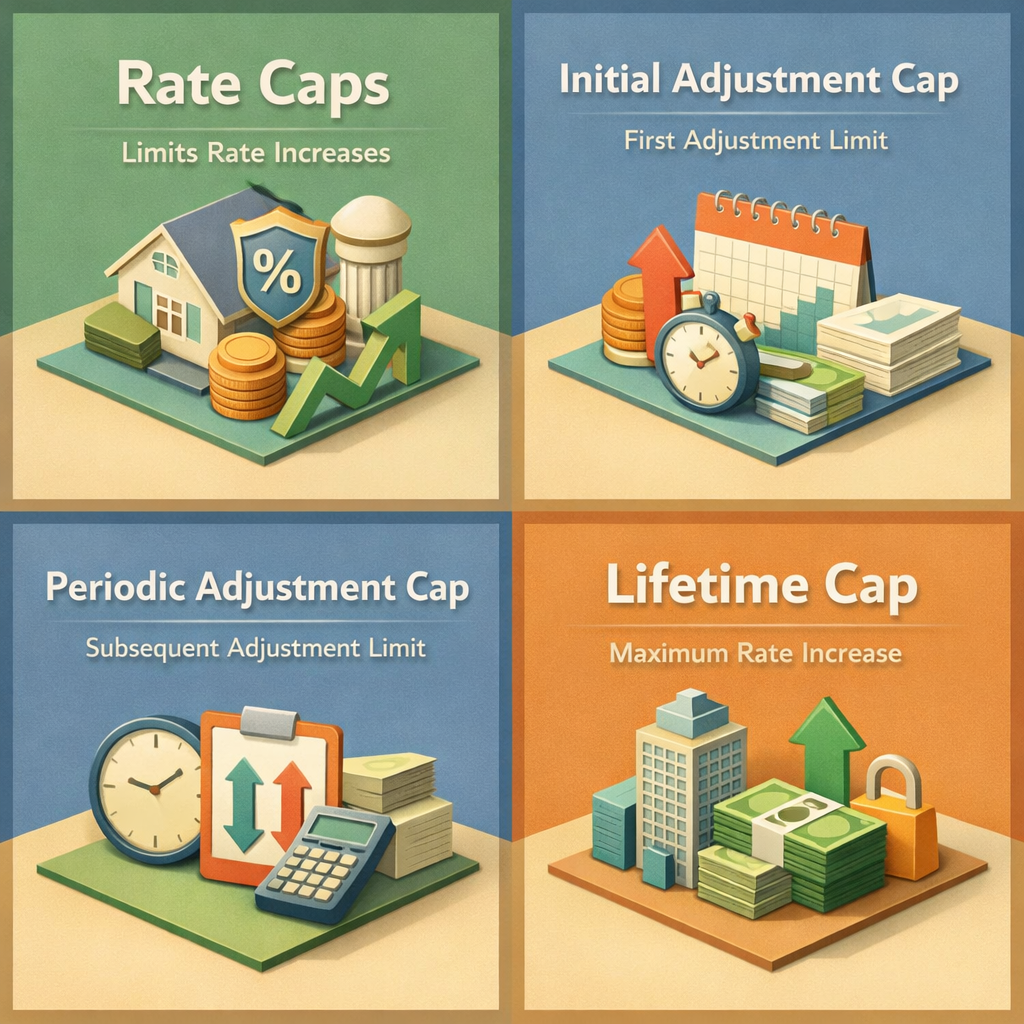

One of the most important features of a modern adjustable-rate mortgage is the rate cap structure. Caps limit how much your interest rate can rise — both at each adjustment and over the life of the loan. Understanding caps is essential before committing to any ARM product.

There are typically three types of caps you'll encounter:

- Initial adjustment cap: Limits how much the rate can change at the first adjustment after the fixed period ends. This is often capped at 2% to 5%.

- Periodic adjustment cap: Limits how much the rate can change at each subsequent adjustment. A 2% periodic cap is common in the market.

- Lifetime cap: Sets the maximum amount the rate can ever increase over the life of the loan, regardless of index movement. Many ARMs carry a 5% lifetime cap above the initial rate.

These protections mean that even if interest rates rise sharply, your monthly payment can't spiral upward without limit. That said, it's still wise to calculate what your payment would look like at the maximum possible rate so you're never caught off guard.

The Potential Advantages of Choosing an ARM Over a Fixed Loan

The most compelling reason homebuyers consider an adjustable-rate mortgages is the lower initial interest rate. Because lenders are taking on less long-term rate risk during the fixed period, they typically offer a lower starting rate compared to a 30-year fixed mortgage. That lower rate translates directly into a lower monthly payment during the introductory period.

This could be a meaningful advantage in several scenarios:

- Short-term homeownership plans: If you expect to sell the home or refinance before the fixed period ends, you may benefit from the lower rate without ever experiencing an adjustment.

- Buying in a high-rate environment: When fixed rates are elevated, the initial rate on an ARM may offer meaningful savings in the short term while you wait for rates to potentially drop.

- Qualifying for a larger loan: A lower initial payment might help some borrowers qualify for a higher loan amount, which could expand their options in a competitive housing market.

- Paying down principal faster: If you apply the savings from the lower payment toward additional principal payments, you could build equity more quickly during the fixed period.

Of course, these advantages only hold if the math works for your specific situation. It's worth using a mortgage calculator to compare total interest costs under different rate scenarios before making a decision.

Risks and Considerations Every Homebuyer Should Weigh Carefully

An adjustable-rate mortgages isn't the right fit for everyone, and it's important to go in with a clear-eyed view of the potential downsides. The most obvious risk is that your rate — and therefore your monthly payment — could rise significantly once the fixed period is over.

If interest rates are higher when your ARM adjusts than they were when you took out the loan, your payment will increase. Depending on how much rates have moved, that increase could strain your monthly budget. Homeowners who aren't financially prepared for higher payments sometimes face difficult choices, including selling the home or refinancing under less favorable conditions.

There are a few other risks worth considering:

- Refinancing isn't always guaranteed: If your home's value has dropped or your credit profile has changed, refinancing out of an ARM before it adjusts may not be as straightforward as anticipated.

- Payment shock: If a borrower isn't fully aware of the cap structure or hasn't planned for higher payments, the adjustment can come as a financial surprise.

- Complexity compared to fixed loans: ARMs involve more moving parts — indexes, margins, caps, and adjustment schedules — which can make them harder to evaluate without expert guidance.

The key is to be honest about your financial resilience. If a rate increase to the maximum cap level would make your payment unaffordable, an ARM may carry more risk than reward for your household.

Who Tends to Benefit Most From an Adjustable-Rate Mortgage

While an ARM isn't universally ideal, certain borrower profiles may find it especially well-suited to their circumstances. Understanding who typically benefits most can help you assess your own fit.

Move-up buyers and relocation professionals who anticipate selling within five to seven years may find that an ARM's lower initial rate delivers real savings without much exposure to rate adjustments. If you know your job or lifestyle will lead to a move within a predictable timeframe, locking into a 30-year fixed rate might mean paying a premium for long-term stability you won't actually use.

High-income borrowers with strong cash reserves may be better positioned to absorb payment increases if and when they occur. For these buyers, the initial rate savings could be meaningful, and the financial cushion reduces the risk of payment shock.

Real estate investors financing rental properties or fix-and-flip projects might also consider ARMs when the investment horizon is short. If the property is expected to be sold or refinanced well within the fixed-rate window, the lower starting payment may improve cash flow and overall return on investment.

Borrowers planning to refinance when rates improve may choose an ARM as a transitional product, accepting the initial rate environment with the expectation of moving into a fixed loan when conditions are more favorable. This strategy carries its own risks, however, and shouldn't be pursued without a contingency plan.

How to Compare ARM Offers and Ask the Right Questions

If you're seriously considering an adjustable-rate mortgage, taking a structured approach to comparison shopping can help you make a well-informed decision. Not all ARMs are created equal, and the details in the loan terms matter a great deal.

Here are some key questions to ask any lender when evaluating an ARM:

- What index does this ARM use, and where can I track it?

- What is the margin the lender adds to the index?

- What are the initial, periodic, and lifetime caps on rate increases?

- What would my payment look like at the cap rate?

- Are there prepayment penalties if I refinance before the fixed period ends?

- How frequently does the rate adjust after the initial period?

You should also compare the Annual Percentage Rate (APR) across loan options, not just the starting interest rate. The APR accounts for certain loan costs and fees and can give you a more accurate picture of the true cost of borrowing over time.

Working with a knowledgeable mortgage professional can make this process significantly easier. An experienced loan officer can model different rate scenarios, walk you through the cap structure in plain language, and help you understand how the ARM you're considering stacks up against current fixed-rate alternatives.

●Conclusion

An adjustable-rate mortgage can be a genuinely useful financing tool when it's matched to the right borrower at the right time. The lower initial rate may offer real savings, and for homebuyers with a clear short-term plan, the risk of future adjustments could be manageable or even avoidable. That said, it's not a one-size-fits-all solution. The decision to choose an ARM over a fixed-rate loan should come from a careful look at your financial situation, your timeline, and your ability to handle potential payment increases down the road. If you're ready to explore your mortgage options and find out what kind of loan fits your goals, connect with the team at LoanWise — we're here to help you make a confident, informed choice.