When you're shopping for a home loan, you'll likely come across two main types of interest rate structures: fixed-rate and adjustable-rate. While fixed-rate mortgages offer predictable monthly payments, an adjustable-rate mortgage takes a different approach — one that could save you money upfront but requires a closer look before you commit. Whether you're a first-time homebuyer, a move-up buyer, or a real estate investor, understanding how ARMs work can help you make a smarter financing decision.

Understanding the Basic Structure of an Adjustable-Rate Mortgage

An adjustable-rate mortgage (ARM) is a home loan where the interest rate changes periodically after an initial fixed period. Unlike a fixed-rate mortgage — where your rate stays the same for the life of the loan — an adjustable-rate mortgage typically starts with a lower introductory rate that later adjusts based on a financial index plus a set margin determined by the lender.

Most ARMs are described using a two-number format, such as a 5/1 ARM or a 7/1 ARM. The first number refers to the length of the initial fixed-rate period, and the second number tells you how often the rate adjusts after that period ends. So, a 5/1 ARM keeps your rate fixed for five years, then adjusts once per year going forward.

The index your rate is tied to is typically a widely recognized benchmark, such as the Secured Overnight Financing Rate (SOFR), which replaced the older LIBOR index. Your lender adds a margin — usually a set number of percentage points — on top of that index to calculate your new rate at each adjustment. This means your future payments could go up or down depending on where market interest rates stand at the time of adjustment.

Key Terms Every Homebuyer Should Know Before Choosing an ARM

Before signing any mortgage documents, it helps to understand the specific terminology lenders use when describing an adjustable-rate mortgage. These terms can have a significant impact on how your loan behaves over time.

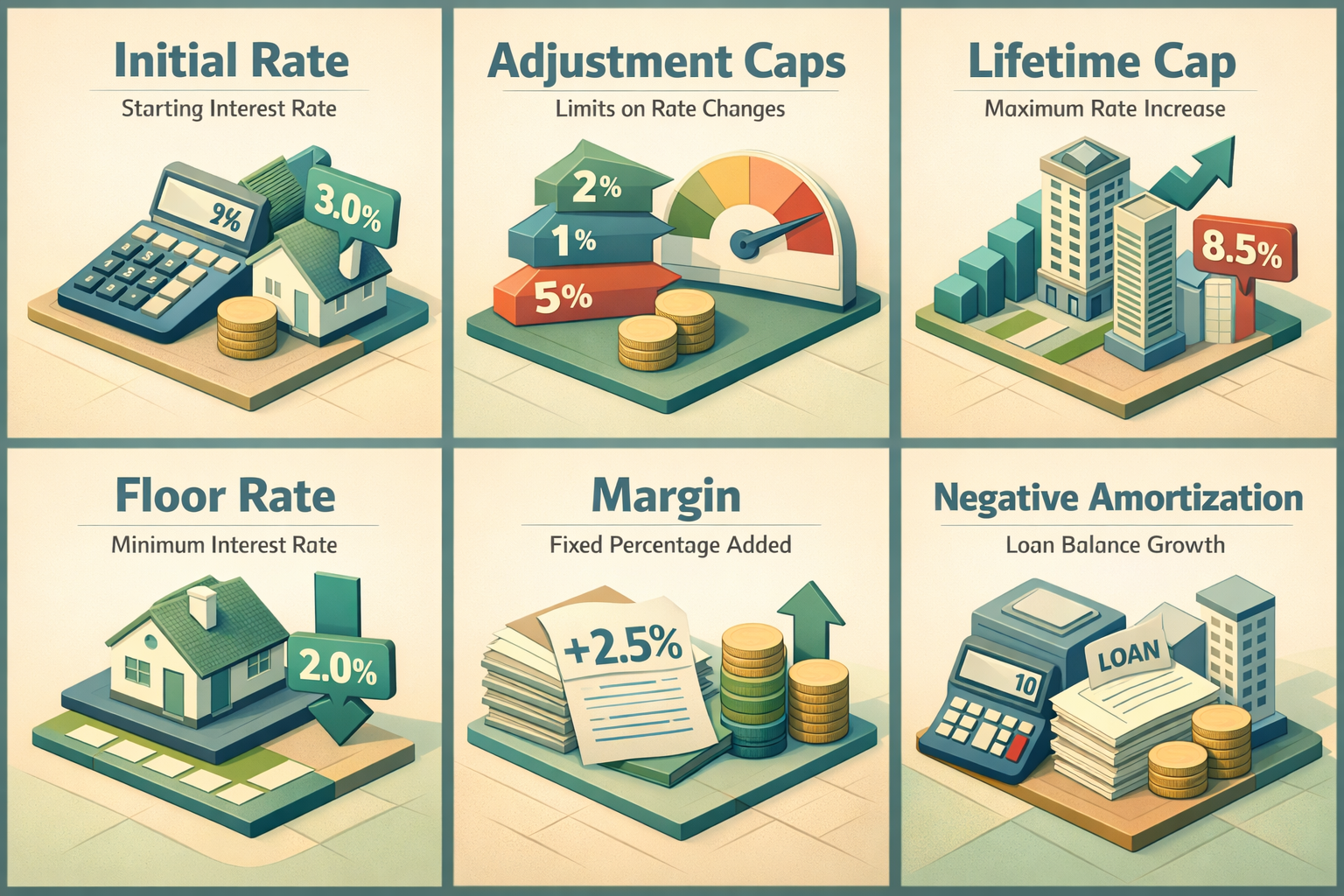

- Initial Rate: The starting interest rate offered during the fixed period. This rate is often lower than what you'd receive on a comparable fixed-rate loan.

- Adjustment Caps: Limits on how much your interest rate can change at each adjustment period. For example, a cap of 2% means your rate can't jump more than 2 percentage points at any single adjustment.

- Lifetime Cap: The maximum amount your interest rate can increase over the entire life of the loan, regardless of market movement. Many ARMs carry a lifetime cap of 5% above the initial rate.

- Floor Rate: The minimum interest rate your loan can fall to, even if the index drops significantly.

- Margin: The fixed percentage the lender adds to the index to determine your adjusted rate. This number doesn't change throughout the loan term.

- Negative Amortization: A situation where your minimum payment doesn't cover the interest owed, causing your loan balance to grow instead of shrink. Not all ARMs carry this risk, but it's worth confirming with your lender.

Taking time to review these terms with your loan officer can help you avoid surprises and understand the full range of possible outcomes before your first rate adjustment arrives.

How ARM Payments Can Shift Over Time

One of the most important things to grasp about an adjustable-rate mortgage is that your monthly payment isn't locked in forever. During the initial fixed period, your payment remains steady and predictable, much like it would on a fixed-rate loan. But once that period ends, your payment could change — sometimes noticeably — at each adjustment interval.

For example, if you took out a 5/1 ARM with a starting rate of 5.5%, your payment stays consistent for the first five years. After that, if the index has risen and your new rate adjusts to 7%, your monthly payment will increase accordingly. Conversely, if rates have fallen, you might actually pay less after the adjustment — which is one of the potential benefits ARM borrowers sometimes overlook.

It's wise to calculate what your payment could look like at the cap limits before you apply. Many lenders and mortgage tools allow you to run these scenarios so you can determine whether you'd still be able to afford the home if your rate reached its maximum allowed adjustment. This kind of stress-testing is an important part of responsible homebuying.

When an Adjustable-Rate Mortgage Might Work in Your Favor

An adjustable-rate mortgage isn't the right fit for every borrower, but there are situations where it may offer a meaningful financial advantage. Understanding when an adjustable-rate mortgage could benefit you helps you weigh it more accurately against other loan options.

One scenario where ARMs tend to shine is when a homebuyer doesn't plan to stay in the home for longer than the initial fixed period. If you know you'll sell or relocate within five to seven years, a 5/1 or 7/1 ARM could let you enjoy a lower initial rate without ever facing an adjustment. This strategy is common among buyers in transitional life stages — such as young professionals, military families, or those entering a growing real estate market with a short-term horizon.

ARMs can also appeal to real estate investors who purchase properties with the intent to renovate and sell within a defined window. A lower initial rate can improve cash flow during the holding period, making the numbers work more favorably on investment deals.

Additionally, some homebuyers opt for an ARM when they expect their income to increase significantly in the coming years, making higher potential payments easier to manage down the road. While this approach carries some risk, it can be a calculated move when based on realistic financial projections.

The Potential Drawbacks and Risks Worth Considering

No mortgage product is without trade-offs, and an adjustable-rate mortgage is no exception. It's important to approach ARMs with a clear-eyed view of the risks involved so you can make a truly informed decision.

The most obvious concern is payment uncertainty. If interest rates rise substantially after your fixed period ends, your monthly housing cost could increase in ways that strain your budget. While adjustment caps provide some protection, a series of maximum adjustments over several years could still lead to a meaningfully higher payment than you started with.

Refinancing is one way homeowners manage this risk — by switching to a fixed-rate loan before the ARM begins adjusting. However, refinancing isn't free. Closing costs, appraisal fees, and potential prepayment penalties can all add up, and you'll need to qualify for the new loan based on your credit profile and financial situation at that time, which may have changed.

Market conditions also matter. If home values have declined since you purchased, your equity position might limit your refinancing options. This is a scenario that some ARM borrowers encountered during the housing market downturn of the late 2000s, which serves as a reminder that real estate and interest rate conditions can shift in unexpected ways.

Borrowers who plan to stay in a home long-term and prioritize payment stability may find that a fixed-rate loan offers greater peace of mind, even if the starting rate is slightly higher.

How Lenders Qualify Borrowers for Adjustable-Rate Home Loans

Qualifying for an ARM follows many of the same steps as applying for any mortgage, but there are a few distinctions worth noting. Lenders will typically review your credit score, debt-to-income ratio, employment history, and down payment amount as part of the standard underwriting process.

One important nuance is that some lenders qualify ARM borrowers at a higher rate than the initial teaser rate — often at the fully indexed rate or a rate based on the first adjustment cap — to ensure you can handle potential payment increases. This practice is designed to prevent borrowers from becoming overextended once the loan begins adjusting.

Conventional ARMs are available through most major lenders and typically follow guidelines set by Fannie Mae and Freddie Mac, which may include minimum credit score requirements and maximum debt-to-income thresholds. FHA-backed ARMs exist as well, and they may be accessible to borrowers with lower credit scores or smaller down payments, though the specific program terms can vary by lender.

If you're self-employed or have non-traditional income, you might explore non-QM ARM products that use alternative documentation methods. These loans are generally priced at higher rates and may carry different qualification standards, so it's worth speaking with a knowledgeable loan officer who can walk you through your options.

●Conclusion

An adjustable-rate mortgage can be a smart financing tool in the right circumstances, but it's not something to enter into without fully understanding how it works. From the initial fixed period and rate caps to the index and margin that drive future adjustments, each element of an ARM plays a role in shaping your long-term housing costs. If you're considering this type of loan, take time to run the numbers, think honestly about how long you plan to stay in the home, and consult with a mortgage professional who can help you compare your options side by side. At LoanWise, we're here to help you navigate the lending landscape with clarity and confidence — so you can choose the home financing path that truly fits your goals.