Starting or expanding a boutique alpaca farm is an exciting venture, but securing the right financing can feel overwhelming. If you're exploring a SBA loan for your alpaca farm, you're on the right track — the Small Business Administration offers loan programs that may be well-suited to specialty agricultural businesses. That said, the application process requires careful preparation, especially when it comes to documentation. Knowing what documents are needed for an SBA loan for a boutique alpaca farm before you sit down with a lender can save you time, reduce stress, and significantly improve your chances of approval. This guide walks you through every major document category so you can approach your lender with confidence.

Why SBA Loans Can Work Well for Specialty Farm Financing

Boutique alpaca farms occupy a unique space in the agricultural economy. They may generate revenue from fiber production, breeding stock sales, agritourism, yarn and textile products, or farm-stay experiences. Because of this diversity, they don't always fit neatly into traditional agricultural lending boxes. That's where SBA loan programs can offer real advantages.

The SBA's 7(a) loan program is the most commonly used option for small business owners seeking working capital, equipment purchases, or real estate acquisition. The SBA 504 loan may be better suited for larger capital expenditures like purchasing land or constructing farm buildings. Both programs are designed to support small businesses that might struggle to qualify for conventional financing, and specialty farm financing lenders often fall into that category.

Because alpaca farming is considered a niche agricultural business, lenders will likely want to see stronger-than-average documentation to feel comfortable with the loan. Understanding this upfront helps you prepare a more compelling application package from the start.

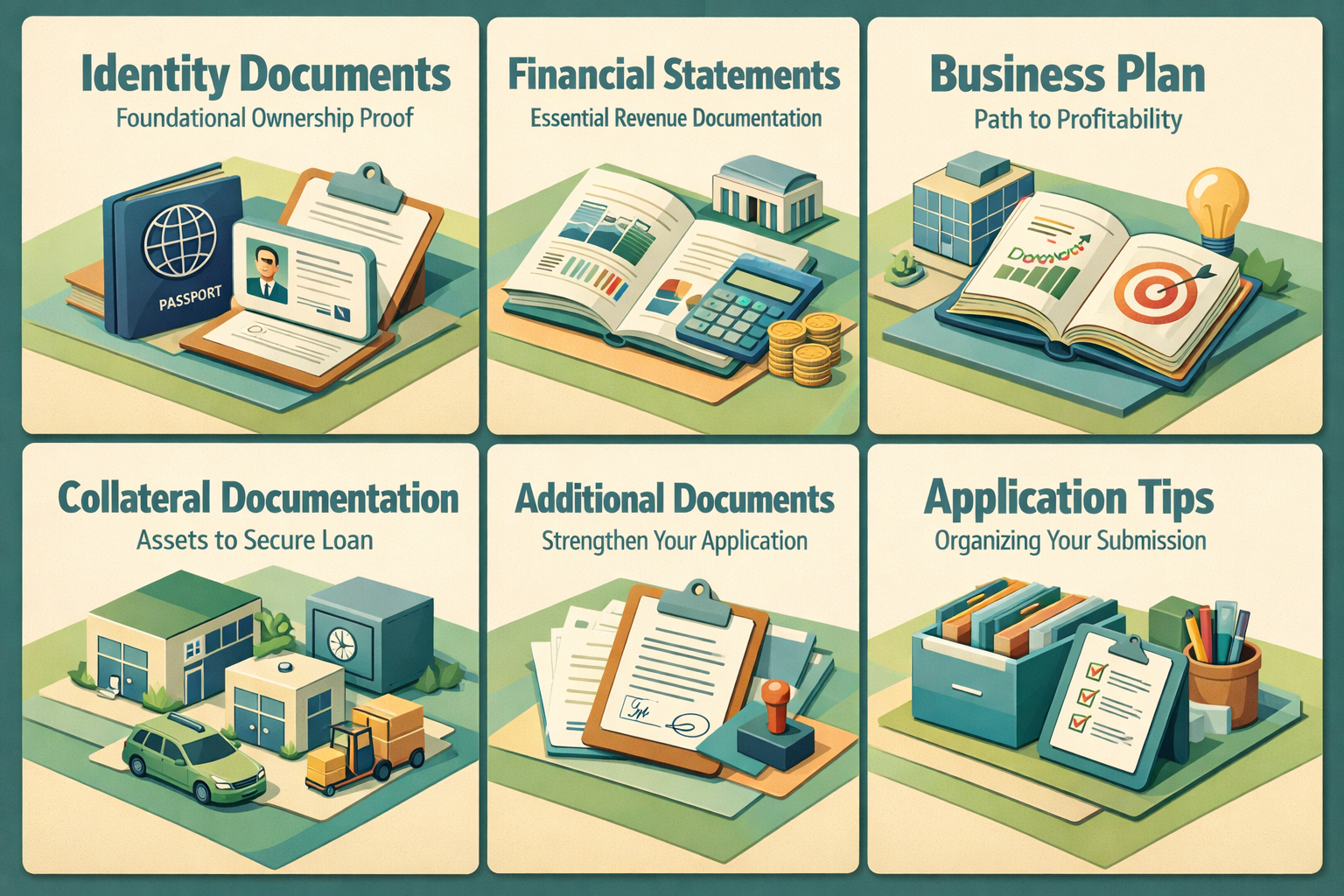

Core Personal and Business Identity Documents You'll Need

Every SBA loan application — regardless of the type of business — typically starts with a foundational set of identity and ownership documents. For a boutique alpaca farm, these would generally include:

- Government-issued photo ID for all business owners with 20% or more ownership stake

- Social Security numbers for each owner, used for personal credit checks

- Business formation documents such as articles of incorporation, partnership agreements, or LLC operating agreements

- Business licenses and permits relevant to agricultural operations in your state or county

- Employer Identification Number (EIN) issued by the IRS

- Proof of U.S. citizenship or lawful permanent residency for all principal owners

It's worth noting that some states require specific permits for livestock operations, agritourism activities, or the sale of animal fiber products. Gathering these early could prevent delays later in the process.

Financial Statements and Tax Records That Lenders Expect

Financial documentation is the backbone of any SBA loan application. Lenders need to assess whether your boutique alpaca farm generates — or is projected to generate — enough revenue to repay the loan. Here's what you'll typically need to provide:

- Personal tax returns for the past two to three years for all owners

- Business tax returns for the same period, if the farm has been operating

- Year-to-date profit and loss (P&L) statement, ideally prepared by an accountant

- Balance sheet showing current assets, liabilities, and equity

- Bank statements — personal and business — for the most recent three to six months

- Accounts receivable and payable aging reports, if applicable

If your alpaca farm is a startup or has been operating for less than two years, you may not have a full financial history. In that case, lenders will likely place greater emphasis on your business plan and financial projections, which we'll cover in the next section.

Keep in mind that lenders may scrutinize seasonal income patterns closely. Alpaca fiber shearing, for example, typically happens once per year, which means your cash flow may be uneven. Being able to explain and document this seasonality thoughtfully can work in your favor.

A Strong Business Plan Is Essential for Agricultural Business Loan Approval

For any agricultural business loan, and especially for a niche operation like a boutique alpaca farm, a well-crafted business plan can make or break your application. Lenders use the business plan to evaluate whether your farm has a realistic path to profitability and long-term sustainability.

Your business plan should typically include:

- Executive summary — a clear, concise overview of your farm's mission, products, and financial goals

- Business description — details about your farm's size, location, herd count, product lines, and revenue streams

- Market analysis — evidence of demand for alpaca fiber, yarn, breeding stock, or agritourism in your target market

- Operations plan — how you'll care for the animals, process fiber, manage staff, and handle logistics

- Marketing and sales strategy — how you'll attract customers, whether through farmers markets, online sales, wholesale accounts, or farm events

- Financial projections — three to five years of projected income statements, cash flow forecasts, and break-even analysis

- Use of loan proceeds — a specific breakdown of exactly how you intend to use the SBA loan funds

Being specific here matters. A lender reviewing a small farm loan application for an alpaca operation will want to see that you've thought through the real-world economics of the business — not just the lifestyle appeal of farming with alpacas.

Collateral and Asset Documentation for Small Farm Loan Requirements

SBA loans are often partially secured by collateral, meaning the lender may ask you to pledge business or personal assets to reduce their risk. For a boutique alpaca farm, relevant collateral documentation might include:

- Real property appraisals for any land or farm buildings you own or plan to purchase

- Equipment lists and valuations for farm machinery, fiber processing equipment, or livestock trailers

- Livestock inventory and appraisals — alpacas themselves may be considered assets, and some lenders accept them as partial collateral

- Insurance certificates for livestock, property, and liability coverage

- Vehicle titles if farm vehicles are being pledged

The SBA generally does not decline a loan solely because collateral is insufficient, but having documented assets strengthens your application. Specialty farm financing lenders are accustomed to working with non-traditional asset types, so don't assume your herd has no value in the eyes of the lender.

It's also worth having your livestock independently appraised if possible. Registered alpacas with documented bloodlines may carry significant value, particularly if you're involved in breeding high-quality animals for resale.

Additional Documentation That Could Strengthen Your Application

Beyond the standard paperwork, there are several supplementary documents that could meaningfully improve your SBA loan application for a boutique alpaca farm. These are often overlooked by first-time applicants but can demonstrate both industry knowledge and operational readiness.

- Letters of intent or purchase orders from buyers, retailers, or wholesale fiber customers

- Lease agreements if you're renting land or farm facilities rather than owning them

- Franchise or licensing agreements, if relevant to your business model

- Resumes or professional biographies of the farm owners and key management, highlighting relevant agriculture, animal husbandry, or business experience

- Industry certifications or memberships such as registration with the Alpaca Owners Association or similar organizations

- Prior loan history or credit references demonstrating responsible borrowing behavior

- Environmental compliance documents if your operation is subject to local zoning or environmental regulations

Lenders evaluating specialty farm financing often have limited benchmarks for niche agricultural businesses. Providing third-party validation — like association memberships, customer commitments, or expert endorsements — can help fill that gap and build lender confidence in your operation.

Tips for Organizing and Submitting Your SBA Loan Application Package

Knowing what documents are needed for an SBA loan for a boutique alpaca farm is only half the battle. How you organize and present those documents can also influence the lender's perception of your professionalism and attention to detail. Here are some practical tips to keep in mind:

- Work with an SBA-approved lender early in the process. They can provide a specific checklist tailored to your loan type and business profile.

- Use a certified public accountant (CPA) to prepare or review your financial statements. Professionally prepared financials tend to carry more weight with underwriters.

- Create a digital and physical file system organized by document category, making it easy to add or update items as requested.

- Be proactive about explanations. If there are gaps in your financial history, unusual income patterns, or prior credit issues, include a brief written explanation rather than leaving the lender to draw their own conclusions.

- Double-check for consistency across all documents — the income figures on your tax returns, P&L statements, and bank statements should tell a coherent story.

- Allow adequate time. SBA loan processing can take several weeks to a few months, so beginning your document preparation well in advance is strongly advisable.

Some borrowers also find it helpful to consult with a SCORE mentor or a local Small Business Development Center (SBDC), both of which offer free guidance to small business owners navigating the SBA loan process for the first time.

●Conclusion

Preparing a complete and well-organized loan application is one of the most important steps you can take when pursuing SBA loan alpaca farm financing. While the document list may seem lengthy, each item serves a clear purpose — helping lenders understand your business, assess risk, and ultimately decide whether to fund your vision. Boutique alpaca farms occupy a genuinely exciting and growing niche in the agricultural economy, and lenders who specialize in small farm loans are increasingly familiar with these operations. By taking the time to understand and gather everything that's needed, you put yourself in the strongest possible position to secure the capital your farm deserves. Ready to take the next step? Reach out to a qualified SBA lender or speak with a LoanWise specialist today to explore your options.