One of the most rewarding benefits available to eligible veterans, active-duty service members, and surviving spouses is the VA home loan program. It offers competitive interest rates, no private mortgage insurance, and in many cases, no down payment requirement. But even with all those advantages, one question comes up often among homebuyers: what are closing costs for VA loan purchase transactions, and how much should you budget? Understanding the fees involved before you reach the closing table can help you make smarter financial decisions and avoid surprises. This guide breaks down every major cost so you can move forward with confidence.

How VA Loan Closing Costs Differ From Conventional Loans

VA loans are backed by the U.S. Department of Veterans Affairs, which means lenders follow specific rules about what they can and cannot charge borrowers. This creates a closing cost structure that's notably different from conventional or FHA loans. In general, VA loan closing costs may be lower overall, but they're not eliminated entirely.

One of the biggest distinctions is that the VA limits or prohibits certain fees that lenders might otherwise charge. For example, lenders are not allowed to charge fees for things like attorney fees on the lender's behalf, prepayment penalties, or certain processing charges that exceed what the VA considers reasonable. This protection is designed to keep the loan accessible and affordable for those who've served.

That said, buyers using a VA loan still pay a range of standard and program-specific fees. The total average cost of VA loan closing typically falls somewhere between 2% and 5% of the purchase price, though this can vary significantly depending on loan amount, location, and lender. It's always worth shopping multiple lenders and requesting a Loan Estimate to compare what each one charges.

Breaking Down the VA Loan Closing Fees You'll Likely See

When reviewing your Loan Estimate or Closing Disclosure, you'll notice several categories of fees. Understanding the VA loan closing fees breakdown can help you spot anything unusual and negotiate where possible.

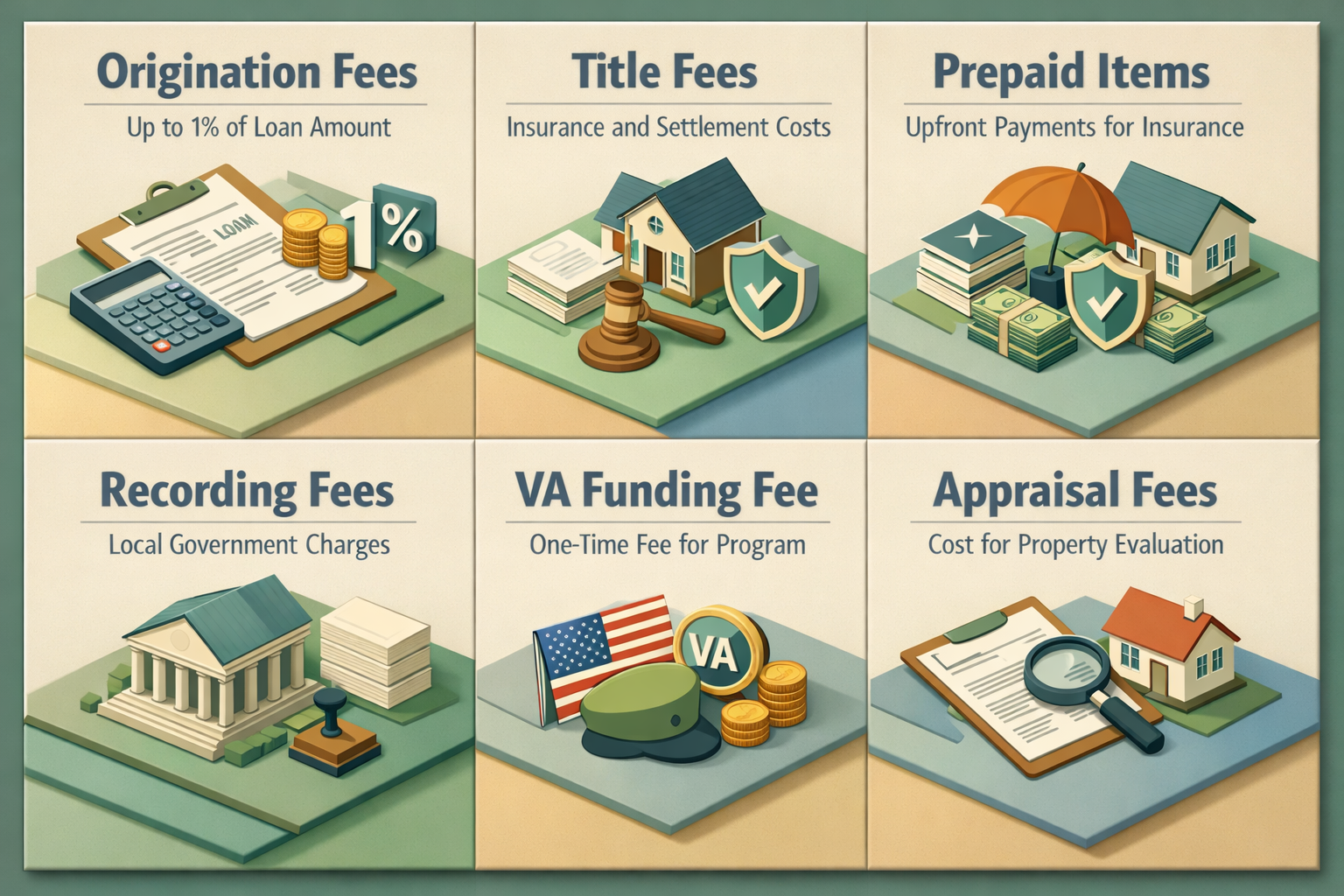

Origination and Lender Fees

Lenders may charge an origination fee, which is typically up to 1% of the loan amount. This covers the administrative work of processing and underwriting your loan. Some lenders bundle multiple fees into this one charge, while others itemize them separately. Either way, the VA caps what lenders can charge under its "1% rule," which limits origination-related fees to no more than 1% of the loan amount.

Title and Settlement Fees

Title insurance and settlement fees are standard across most home purchase transactions. You'll likely pay for a lender's title insurance policy, a title search to verify ownership history, and settlement or escrow fees charged by the closing agent or title company. These costs can vary by state and are influenced by local custom and the purchase price of the home.

Prepaid Items and Escrow Deposits

Prepaids are not technically fees — they're upfront payments for costs you'll owe anyway. These often include prepaid homeowner's insurance, prepaid mortgage interest covering the days between closing and your first payment, and an initial deposit into your escrow account for property taxes and insurance. While prepaids can add a few thousand dollars to your closing costs, they represent money going into your own account or coverage, not a lender's pocket.

Recording Fees and Transfer Taxes

Local governments typically charge recording fees to register the new deed and mortgage documents. Some jurisdictions also charge transfer taxes when property changes hands. These amounts vary considerably by location and are generally non-negotiable since they're set by local law.

The VA Funding Fee: What It Is and How Much It Costs

Perhaps the most unique cost associated with VA home loans is the VA funding fee. This is a one-time fee paid to the Department of Veterans Affairs that helps sustain the program for future borrowers. Because VA loans don't require private mortgage insurance, the funding fee partially offsets the cost the government assumes by guaranteeing the loan.

The VA funding fee amount depends on several factors, including whether it's your first time using a VA loan or a subsequent use, your down payment amount, and your military service category. For first-time VA loan users with no down payment, the fee is typically around 2.15% of the loan amount. For subsequent uses, it may increase to approximately 3.3%. However, if you make a down payment of 5% or more, the fee is reduced, and a down payment of 10% or more reduces it further.

Importantly, certain borrowers may be exempt from paying the VA funding fee entirely. Veterans receiving VA disability compensation, surviving spouses of veterans who died in service or from a service-connected disability, and active-duty service members who have received a Purple Heart may qualify for an exemption. Always confirm your exemption status with your lender before closing.

One of the most borrower-friendly features of this fee is that it can be rolled into the loan balance rather than paid out of pocket at closing. This means you don't need to bring additional cash to the table to cover it, though it will slightly increase your monthly payment and total interest paid over time.

VA Appraisal Fees and Inspection Costs for Purchase Transactions

Before a VA loan can be approved, the property must be appraised by a VA-certified appraiser. The appraisal serves two purposes: it confirms the home's market value and verifies that the property meets the VA's Minimum Property Requirements (MPRs), which cover safety, structural soundness, and sanitation standards.

VA appraisal fees for purchase transactions are set by the VA and vary by location. In many parts of the country, you might expect to pay somewhere in the range of a few hundred dollars for a standard single-family home appraisal, though fees in high-cost or rural areas can be higher. The VA publishes maximum allowable appraisal fees by state, so your lender should be able to tell you the cap that applies to your area.

It's worth noting that the VA appraisal is not a substitute for a home inspection. While the appraisal checks for major deficiencies, a full home inspection conducted by a licensed inspector provides a much more thorough evaluation of the property's condition. Home inspection fees are typically paid separately and out of pocket before closing. Skipping this step could leave you unaware of costly issues that weren't caught during the appraisal process.

Other inspection-related costs that might arise include termite or pest inspections, which are sometimes required in certain states or geographic regions for VA loans. These fees are relatively modest but should be factored into your overall closing cost estimates.

Who Pays VA Loan Closing Costs: Buyer, Seller, or Lender?

One of the most appealing aspects of VA loan rules is that sellers are permitted — and sometimes expected in negotiation — to cover a portion of the buyer's closing costs. The VA allows sellers to pay all of the buyer's loan-related closing costs, plus up to 4% of the loan amount in concessions. This can include paying for the funding fee, prepaid items, or other costs, which could dramatically reduce how much cash a veteran buyer needs at closing.

This makes seller concessions a powerful negotiating tool, especially in a buyer's market where sellers may be more motivated to offer incentives. Even in competitive markets, it's worth asking your real estate agent to negotiate seller-paid closing costs as part of your offer strategy.

Lender credits are another option. In exchange for accepting a slightly higher interest rate, a lender may offer credits that offset some or all of your closing costs. This can be a smart choice if you're short on cash upfront and plan to sell or refinance within a few years before the rate difference significantly affects your total interest paid.

Veterans can also use gift funds from family members to help cover closing costs, as long as they're properly documented according to the lender's requirements. Combining seller concessions, lender credits, and gift funds could potentially allow a qualified VA borrower to close on a home with little to no money out of pocket.

Practical Tips for Reducing What You Pay at the Closing Table

Knowing what are closing costs for VA loan purchase transactions is the first step. The second is finding ways to reduce them. Here are several strategies worth exploring as you prepare to buy:

- Shop multiple lenders: Lender fees can vary significantly. Getting at least three Loan Estimates lets you compare origination charges, points, and other lender-controlled costs side by side.

- Negotiate seller concessions: As mentioned, sellers can legally pay your closing costs up to the VA's limits. Make it part of your offer discussion, especially when inventory is higher and sellers have more motivation to deal.

- Ask about lender credits: If preserving cash is the priority, a lender credit in exchange for a marginally higher rate might make sense for your situation.

- Roll the funding fee into the loan: If the upfront cost of the VA funding fee is a concern, financing it into the loan removes that immediate burden at closing.

- Review your Closing Disclosure carefully: You'll receive this document at least three business days before closing. Compare it line by line with your Loan Estimate and ask your lender to explain any discrepancies or unexpected charges.

- Confirm funding fee exemptions: If you receive VA disability benefits, verify your exemption status early in the process so it's reflected accurately in your loan documents.

Being proactive and informed throughout the loan process can help you arrive at closing prepared and without unwelcome financial surprises.

●Conclusion

Understanding what goes into your closing costs is an essential part of planning a successful home purchase with a VA loan. From lender origination charges and title fees to the VA funding fee and appraisal costs, each line item plays a role in the total amount you'll need to bring to closing — or negotiate away. The good news is that VA loans come with built-in protections that limit excessive lender charges, and flexible options like seller concessions and funding fee financing can make homeownership even more accessible for those who've earned this benefit through their service. If you're ready to explore your VA loan options or want a personalized estimate of your closing costs, LoanWise is here to help you take the next step with clarity and confidence.