Buying a high-value home in the United States is an exciting goal — whether you're relocating for work, investing in real estate, or establishing roots in a new country. But if your income comes from outside the U.S., securing the financing you need can feel like navigating a maze. Jumbo loans, which are mortgages that exceed the conforming loan limits set by the Federal Housing Finance Agency, come with stricter qualification standards than conventional loans. When you add foreign income into the equation, the process becomes even more nuanced. Understanding how to qualify for a jumbo loan with foreign income documentation is the first and most important step toward making your homeownership goal a reality. This guide walks you through what lenders typically expect, what documents you'll likely need, and how to position yourself as a strong borrower.

What Makes Jumbo Loans Different from Conventional Mortgages

Jumbo loans are designed for properties that exceed the conforming loan limits established annually by the FHFA. In most parts of the United States, any loan amount above $766,550 (as of recent guidelines) may be considered a jumbo mortgage, though this threshold can vary by county. Because these loans are too large to be purchased or backed by Fannie Mae or Freddie Mac, lenders take on more risk — and they respond to that risk with stricter underwriting standards.

For borrowers with domestic W-2 income, the process is already demanding. Lenders typically look for higher credit scores, larger down payments, lower debt-to-income ratios, and more substantial cash reserves compared to conventional loans. For those earning income abroad, the scrutiny can go even further. Lenders must verify not just how much you earn, but also the stability, currency, and reliability of that income over time.

It's also worth noting that jumbo loans are portfolio products, meaning lenders keep them on their own books rather than selling them on the secondary market. This gives individual lenders more flexibility in how they evaluate foreign income borrowers — but it also means requirements can vary significantly from one lender to the next. Shopping around is especially important in this space.

Understanding Foreign Income in the Context of Jumbo Mortgage Underwriting

Foreign income refers to wages, salaries, self-employment earnings, rental income, or other revenue sources generated outside the United States. Lenders evaluating this type of income must consider several factors that don't typically apply to domestic borrowers.

First, there's the matter of currency risk. If your income is paid in a foreign currency, lenders will often convert it to U.S. dollars using a current or averaged exchange rate. Fluctuations in that rate could affect how your income is calculated, and lenders may apply a conservative conversion approach to account for potential changes.

Second, lenders consider the stability and continuity of the income. Just as they would for a U.S.-based employee, they want to see a reliable, ongoing earnings history. For foreign employees, this may mean verifying employment with an international company, confirming the nature of your role, and assessing whether the income is likely to continue.

Third, there's the challenge of documentation standards. U.S.-based borrowers submit W-2s, tax returns, and pay stubs. Foreign income earners may need to provide translated and notarized equivalents, employer verification letters, bank statements showing consistent deposits, and sometimes country-specific tax filings. Not all lenders are equipped to evaluate these documents, which is why working with a lender experienced in international borrower scenarios is strongly recommended.

How to Qualify for a Jumbo Loan with Foreign Income Documentation: Core Requirements

So, exactly how to qualify for a jumbo loan with foreign income documentation? While requirements vary by lender, there are several core criteria that most underwriters will examine closely.

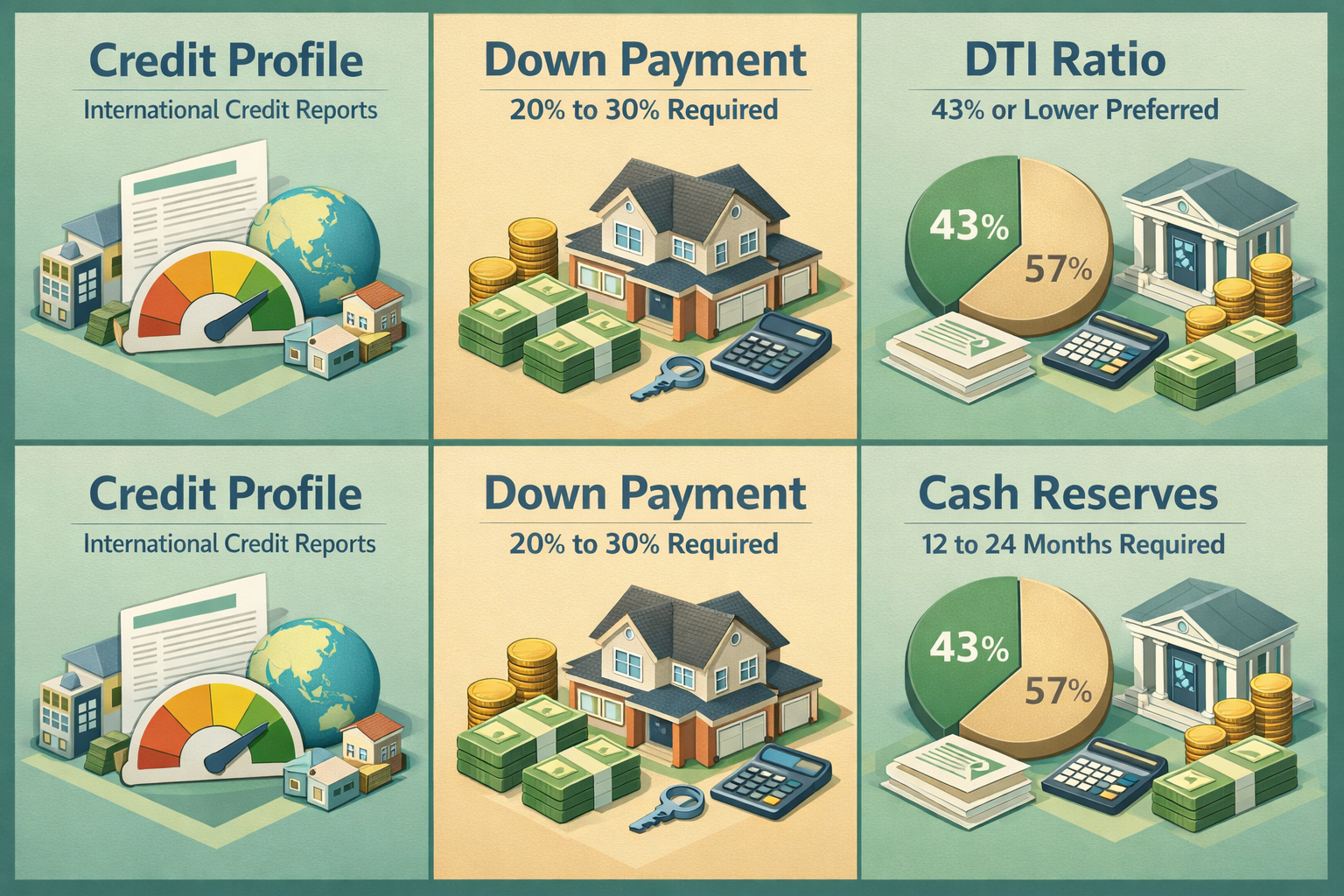

Credit Profile and History

Even if you don't have a U.S. credit history, many lenders may be willing to use international credit reports or alternative credit references to evaluate your creditworthiness. Some lenders have relationships with international credit bureaus, while others may accept bank references, landlord letters, or utility payment histories as substitutes. U.S. credit scores, if available, are still strongly preferred — a score of 700 or higher is often considered a baseline for jumbo loans, though some lenders may require 720 or above.

Down Payment Requirements

Jumbo loans for foreign income earners typically require a larger down payment than standard jumbo loans for domestic borrowers. It's common to see requirements ranging from 20% to 30% or more of the purchase price. A larger down payment reduces the lender's exposure and demonstrates your financial commitment to the property. It can also help offset other risk factors, such as limited U.S. credit history or income documentation complexity.

Debt-to-Income Ratio

Lenders will calculate your debt-to-income (DTI) ratio using your verified foreign income and any existing debt obligations. A DTI of 43% or lower is often preferred, though some portfolio lenders may accept slightly higher ratios depending on the strength of your overall financial profile. Keeping existing debts low before applying will help improve your DTI standing.

Cash Reserves

Cash reserves are a significant factor for jumbo borrowers in general, but they take on added importance for foreign income earners. Lenders may require 12 to 24 months — or more — of mortgage payments held in liquid reserves. These funds may need to be held in a U.S. bank account or at least be readily accessible and documented clearly.

Essential Documents You'll Likely Need to Prepare

Preparation is everything when applying for a jumbo loan as a foreign income earner. The documentation process can be more involved than what domestic borrowers experience, so starting early and organizing your paperwork thoroughly can make a meaningful difference.

- Foreign tax returns: Typically two years of returns from your home country, translated into English by a certified translator if necessary.

- Employer verification letter: A letter from your employer confirming your position, length of employment, salary, and the likelihood of continued employment. This may need to be on company letterhead and notarized.

- Pay stubs or salary statements: Recent pay documentation showing consistent income, ideally covering the last 30 to 60 days.

- Bank statements: 12 to 24 months of bank statements from both foreign and U.S. accounts demonstrating consistent deposits and available reserves.

- Passport and visa documentation: Proof of identity and legal status in the United States, including any relevant visa type (such as an E-2, L-1, H-1B, or O-1 visa).

- Foreign credit report or alternative credit references: If you lack a U.S. credit history, international credit reports or reference letters from creditors or financial institutions may be accepted by some lenders.

- Currency conversion documentation: Evidence showing how your income converts to U.S. dollars, potentially including exchange rate histories or statements from a licensed currency exchange service.

It's important to work closely with your lender early in the process to confirm exactly which documents they require. Requirements can vary, and gathering the right paperwork upfront prevents delays in underwriting.

Jumbo Mortgage Requirements for Non-US Residents: Visa Status and Residency Considerations

Your immigration or residency status can play a significant role in how lenders evaluate your application. Understanding the jumbo mortgage requirements for non-US residents across different categories will help you set realistic expectations.

Permanent Residents and Green Card Holders

Borrowers with lawful permanent resident status (green card holders) are often treated similarly to U.S. citizens by most lenders. You'll still need to document foreign income thoroughly, but your legal residency status typically removes one layer of complexity from the qualification process.

Non-Permanent Residents on Work Visas

Borrowers on work visas such as H-1B, L-1, O-1, or E-2 may qualify for jumbo loans, but lenders will closely examine the remaining validity of the visa and the likelihood of renewal. Some lenders require at least one to two years of remaining visa validity, while others may look at the employer's sponsorship commitment as an indicator of continued residency.

Foreign Nationals Without U.S. Residency

This group faces the most rigorous scrutiny. Foreign national borrowers — those who do not live in the U.S. full-time — may still qualify for jumbo loans through certain portfolio lenders and private banks that specialize in international clients. These programs often carry higher interest rates, require larger down payments (sometimes 30% or more), and may limit loan-to-value ratios more aggressively. However, they can be a viable pathway for real estate investors or buyers purchasing vacation and second homes in the United States.

Strategies to Strengthen Your Jumbo Loan Application as a Foreign Income Earner

Even with the added complexity of foreign income documentation, there are practical steps you can take to make your application more compelling to lenders.

Establish U.S. Banking Relationships Early

Opening and maintaining U.S. bank accounts well before you apply for a jumbo loan helps demonstrate financial ties to the country. Consistent deposits, a positive account history, and solid account balances all work in your favor during underwriting.

Build U.S. Credit History Where Possible

If you've been in the U.S. for any period of time, building a U.S. credit profile can significantly ease the qualification process. Secured credit cards, credit-builder loans, or becoming an authorized user on a trusted person's account are a few ways to start establishing a domestic credit history.

Work with Lenders Who Specialize in International Borrowers

Not all lenders are equipped or willing to evaluate foreign income documentation. Seeking out portfolio lenders, private banks, or mortgage brokers who have experience with international clients can save you considerable time and frustration. These specialists understand how to evaluate non-standard income documentation and may offer more flexible program options.

Consider a Larger Down Payment

If you have the financial capacity, offering a larger down payment than the minimum required can reassure lenders and potentially improve your loan terms. It lowers the loan-to-value ratio, reducing the lender's risk exposure and potentially opening doors to better interest rates or more favorable underwriting decisions.

Reduce Existing Debt Obligations

Paying down existing debts before applying will help lower your DTI ratio and signal financial discipline to underwriters. Even modest reductions in credit card balances or installment loan balances can shift your DTI into a more favorable range.

Finding the Right Lender for Your Situation

Choosing the right lending partner is arguably the most critical step in this process. Because jumbo loans are portfolio products and foreign income adds additional complexity, lenders vary widely in their willingness and ability to work with international borrowers.

Private banks and wealth management institutions often have dedicated programs for high-net-worth international clients. These programs may offer competitive terms for buyers with substantial assets, even when income documentation is more complex. Some regional and community banks with a strong international client base may also offer tailored solutions.

Mortgage brokers who specialize in non-QM (non-qualified mortgage) lending and foreign national programs can be valuable allies. They have access to a wide network of portfolio lenders and can match your specific situation to the most suitable program. Non-QM programs may allow for bank statement income verification rather than traditional tax return documentation, which could be particularly helpful if your foreign income is structured in ways that don't translate neatly to U.S. tax conventions.

When evaluating lenders, ask directly about their experience with foreign income documentation, their specific requirements for your visa or residency status, and any programs they offer for international borrowers. A lender who can speak confidently and specifically to your situation is far more likely to help you reach the closing table successfully.

●Conclusion

Qualifying for a jumbo loan as someone who earns income abroad requires careful planning, thorough documentation, and the right lending partner. The process may be more involved than a standard domestic mortgage application, but it's absolutely achievable with the right preparation. Understanding how to qualify for a jumbo loan with foreign income documentation starts with knowing what lenders are looking for — strong credit, substantial reserves, a manageable DTI, and well-organized documentation of your earnings. From there, building U.S. financial relationships, working with experienced specialists, and presenting your application as thoroughly as possible can make a meaningful difference in your outcome. At LoanWise, we're here to help you navigate complex mortgage scenarios with confidence. Whether you're a foreign national purchasing a U.S. investment property or a visa holder buying your primary residence, our team can connect you with lenders equipped to evaluate your unique financial profile. Reach out today and take the first step toward securing your jumbo mortgage.