Tiny homes have become an increasingly popular housing choice for buyers looking to simplify their lifestyle, reduce their mortgage burden, or enter the real estate market at a lower price point. But when it comes to financing a tiny home, the process can be a bit more complex than a standard purchase. One of the most common questions buyers ask is: what are closing costs for FHA loan on a tiny home? Understanding these fees upfront can help you budget more effectively and avoid surprises at the closing table. In this guide, we'll walk through how FHA loans work for small homes, what closing fees to anticipate, and practical strategies to manage your total out-of-pocket costs.

How FHA Loans Apply to Small Homes and Tiny House Financing

Before diving into closing costs, it's important to understand whether your tiny home even qualifies for an FHA loan. The Federal Housing Administration insures FHA loans, which makes them an attractive option for buyers with lower credit scores or limited down payment savings. However, FHA guidelines include property requirements that can affect tiny home eligibility.

To qualify for FHA loan for small homes, the property typically must meet specific standards, including being classified as real property rather than personal property. This means the home generally needs to be built on a permanent foundation, connected to utilities, and meet local building codes. A tiny home that sits on wheels, for example, may be considered a recreational vehicle and would not qualify for standard FHA financing.

Additionally, FHA sets minimum property size requirements. While the FHA doesn't publish a strict minimum square footage, the property must be considered a viable and safe dwelling — meaning extremely small homes may face appraisal challenges. Buyers considering an FHA loan for small homes should work closely with an experienced lender and appraiser who understands these nuances before proceeding.

It's also worth noting that FHA loans come with a minimum loan amount threshold at many lenders, sometimes referred to informally as an overlay. Since tiny homes tend to carry lower purchase prices, some lenders may decline to originate very small loan amounts. Shopping around for a lender familiar with tiny house financing closing fees and low-balance FHA loans is an important first step.

Breaking Down What Are Closing Costs for FHA Loan on a Tiny Home

So, what are closing costs for FHA loan on a tiny home? Closing costs are fees paid at settlement to finalize your mortgage. They cover services like loan origination, title work, appraisals, inspections, and government recording fees. For FHA loans specifically, there are also government-mandated charges that conventional loan borrowers don't always face.

Closing costs for FHA loans generally range from roughly 2% to 6% of the loan amount, though the actual percentage can vary depending on your lender, location, and the specifics of the transaction. Because tiny homes typically carry lower price tags, the closing costs in dollar terms may be lower than a standard home purchase — but the percentage relative to the loan could feel just as significant or even higher if lenders charge flat minimum fees.

Here are the most common closing cost categories you're likely to encounter:

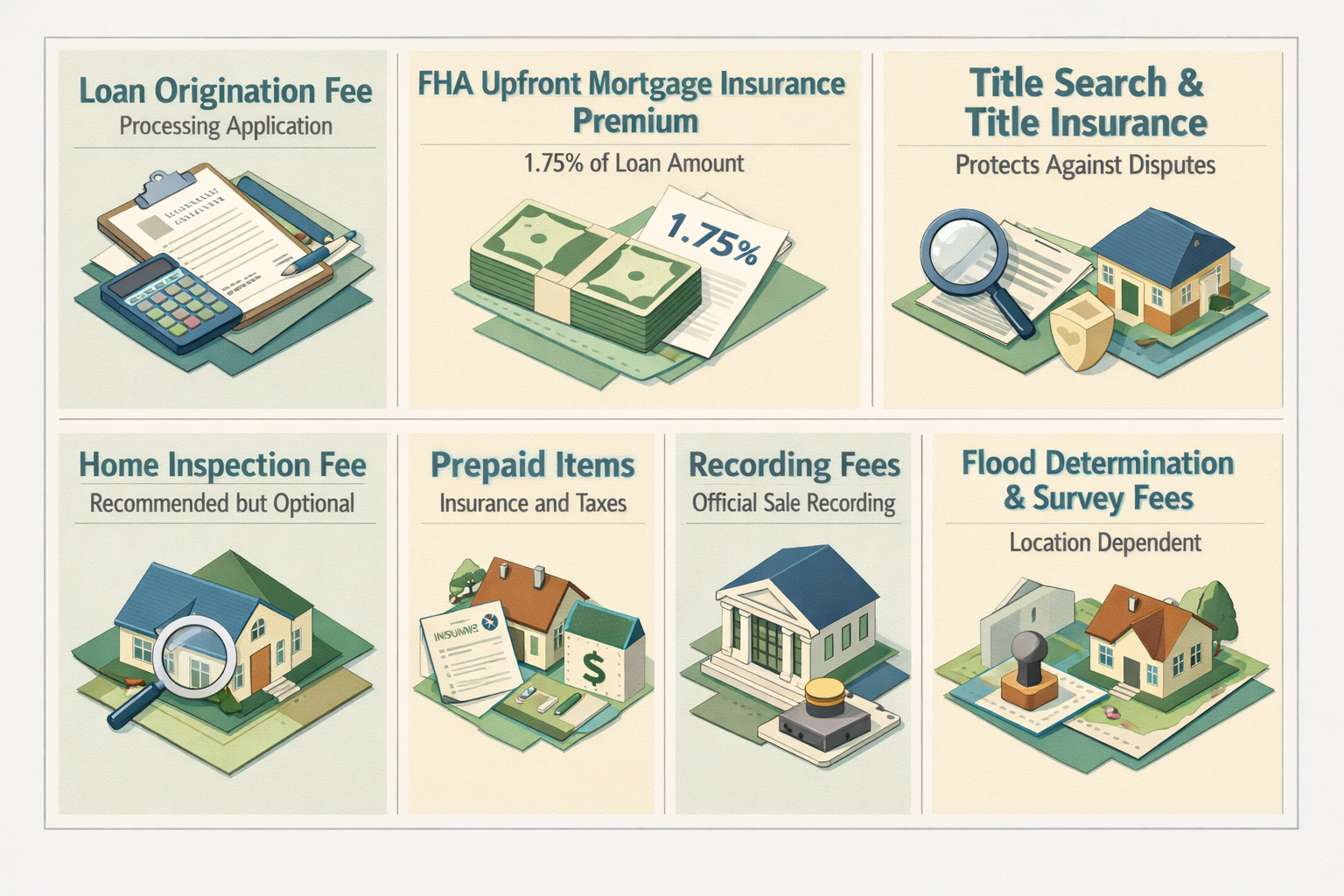

- Loan Origination Fee: Charged by the lender for processing your loan application. This is typically a percentage of the loan amount, though some lenders charge flat fees.

- FHA Upfront Mortgage Insurance Premium (UFMIP): One of the most notable FHA-specific costs, the UFMIP is currently set at 1.75% of the base loan amount. This can be rolled into the loan balance rather than paid out of pocket at closing.

- Appraisal Fee: FHA requires an FHA-approved appraisal, which may cost more than a conventional appraisal due to the additional property condition standards the appraiser must evaluate.

- Title Search and Title Insurance: These fees protect both you and the lender from title disputes. They vary by state and property value but are a standard part of any home purchase.

- Home Inspection Fee: While not always required by FHA, a home inspection is strongly recommended and is typically paid outside of closing.

- Prepaid Items: These include homeowners insurance premiums, prepaid interest, and initial escrow deposits for property taxes and insurance.

- Recording Fees: Charged by local government offices to officially record the sale and the new mortgage lien.

- Flood Determination and Survey Fees: Depending on the property's location and lender requirements, these may also apply.

For tiny homes, the appraisal process may be particularly notable. If there are few comparable sales of similar tiny homes in the area, the appraiser may have difficulty establishing fair market value, which could complicate the transaction and potentially add time and cost to the process.

Understanding FHA Mortgage Insurance and Its Role in Your Total Loan Cost

Mortgage insurance is a defining feature of FHA loans, and it plays a significant role in the total cost of borrowing. Beyond the Upfront Mortgage Insurance Premium paid at closing, FHA borrowers also pay an Annual Mortgage Insurance Premium (MIP) throughout the life of the loan in most cases.

The Annual MIP is added to your monthly mortgage payment. Its rate can vary depending on your loan term, loan-to-value ratio, and loan amount. For many FHA borrowers putting down less than 10%, MIP may remain in place for the life of the loan — a factor worth considering when evaluating the long-term affordability of tiny house financing closing fees and ongoing costs.

While mortgage insurance adds to your monthly obligations, it's also what makes FHA loans accessible to buyers who might not otherwise qualify for conventional financing. For first-time homebuyers or those with less-than-perfect credit, the trade-off is often well worth it. The key is to factor both the upfront and annual premiums into your full cost analysis before committing to an FHA loan for a tiny home.

Property Eligibility Challenges Unique to Tiny House Purchases

Beyond the financial components, tiny home buyers should be aware of the structural and legal hurdles that can affect whether a property qualifies for FHA financing at all. These challenges can influence not just loan approval but also which closing costs you might incur — and whether certain fees get spent before a deal falls through.

First, zoning laws vary widely by municipality. Some areas don't permit homes below a certain square footage, and tiny homes may be classified differently depending on local ordinances. If a tiny home is located in a zoning area that doesn't formally recognize it as a residential dwelling, FHA financing may not be available for it regardless of the home's physical condition.

Second, the home must be on a permanent foundation to qualify as real property under FHA guidelines. Homes on skids, trailers, or mobile chassis are generally not eligible for standard FHA mortgage products. Buyers who have already paid for inspections or appraisals before discovering this limitation may find those fees are non-recoverable.

Third, FHA-approved appraisers use Minimum Property Standards (MPS) to evaluate homes. Tiny homes must meet these standards, which address things like adequate space for living, sleeping, cooking, and sanitation. A home that doesn't meet MPS could require repairs before the loan can close, potentially adding costs and delays to the process.

Working with a real estate agent and lender who specialize in alternative or niche housing types can help you navigate these challenges before spending money on non-refundable fees.

Strategies to Reduce Tiny House Financing Closing Fees

The good news is that there are several strategies buyers can use to lower their out-of-pocket closing costs when pursuing an FHA loan for a tiny home. While you may not be able to eliminate these fees entirely, there are legitimate ways to keep costs manageable.

- Negotiate Seller Concessions: FHA guidelines allow sellers to contribute up to 6% of the purchase price toward the buyer's closing costs. This is known as a seller concession and can meaningfully reduce what you need to bring to the closing table. In a buyer's market or with a motivated seller, this negotiation is often possible.

- Roll the UFMIP Into the Loan: As mentioned, the 1.75% Upfront Mortgage Insurance Premium can be financed into your loan balance rather than paid at closing. This reduces your immediate cash requirement, though it does slightly increase your monthly payment and total interest paid over time.

- Compare Lender Loan Estimates: Under federal law, lenders are required to provide a Loan Estimate within three business days of receiving your application. Comparing Loan Estimates from multiple lenders helps you identify which origination fees and lender charges are most competitive.

- Ask About Lender Credits: Some lenders offer lender credits in exchange for a slightly higher interest rate. This effectively shifts some closing costs into your rate, which may be a worthwhile trade-off if you plan to sell or refinance within a few years.

- Look Into Down Payment Assistance Programs: Some state and local programs offer grants or second loans that can be used toward both down payment and closing costs. These programs often target first-time homebuyers and may have income or location eligibility requirements.

- Time Your Closing Strategically: Closing later in the month can reduce the amount of prepaid interest you owe at closing, since interest is only collected for the remaining days of the month.

Comparing FHA Loan Costs to Other Tiny Home Financing Options

FHA loans are not the only way to finance a small or tiny home. Depending on your situation and the property type, other financing options may be worth exploring — and each comes with its own closing cost considerations.

Conventional loans typically require a higher credit score and a larger down payment than FHA loans, but they don't carry the mandatory mortgage insurance premium structure in the same way. For buyers with strong credit who can put down 20% or more, a conventional loan might result in lower long-term costs, though closing fees can be comparable in many categories.

Personal loans are sometimes used to finance tiny homes, particularly those on wheels that don't qualify as real property. Personal loans generally don't have the same property-based closing costs as mortgages, but they often carry higher interest rates and shorter repayment terms, which can make monthly payments significantly higher.

Chattel loans, sometimes called manufactured home loans, may apply to certain factory-built homes that aren't on permanent foundations. These loans typically carry higher rates than traditional mortgages and come with their own fee structures.

USDA loans are another government-backed option for eligible rural properties. If a tiny home is located in a USDA-eligible area and meets the program's property standards, this could be a competitive alternative to FHA financing — particularly given that USDA loans can offer zero down payment options.

Evaluating these alternatives side by side with a qualified mortgage professional can help you determine which path offers the best combination of accessibility, closing costs, and long-term affordability for your specific situation.

●Conclusion

Understanding what are closing costs for FHA loan on a tiny home is an essential part of budgeting for your purchase. From origination fees and FHA mortgage insurance premiums to appraisal challenges and title costs, tiny home buyers face a unique combination of expenses that require careful planning. While FHA loans offer an accessible path to homeownership for many buyers, the property eligibility requirements and fee structures can add complexity to transactions involving smaller or non-traditional dwellings.

The most important step you can take is to connect with a lender who understands the nuances of FHA loan for small homes and has experience with alternative housing types. Comparing Loan Estimates, exploring seller concessions, and reviewing local assistance programs can all help you close with confidence and keep more money in your pocket. At LoanWise, we're here to help you navigate your financing options with clarity and expertise — so you can make the right decision for your home and your financial future.