When you're using a VA loan to purchase your dream home, understanding the inspection process is crucial for a successful transaction. VA loan inspection requirements are designed to protect veterans and ensure they're making a sound investment in a safe, habitable property. While these standards might seem strict, they're actually working in your favor to guarantee you're getting quality housing that meets specific safety and livability criteria.

Understanding VA Loan Property Standards

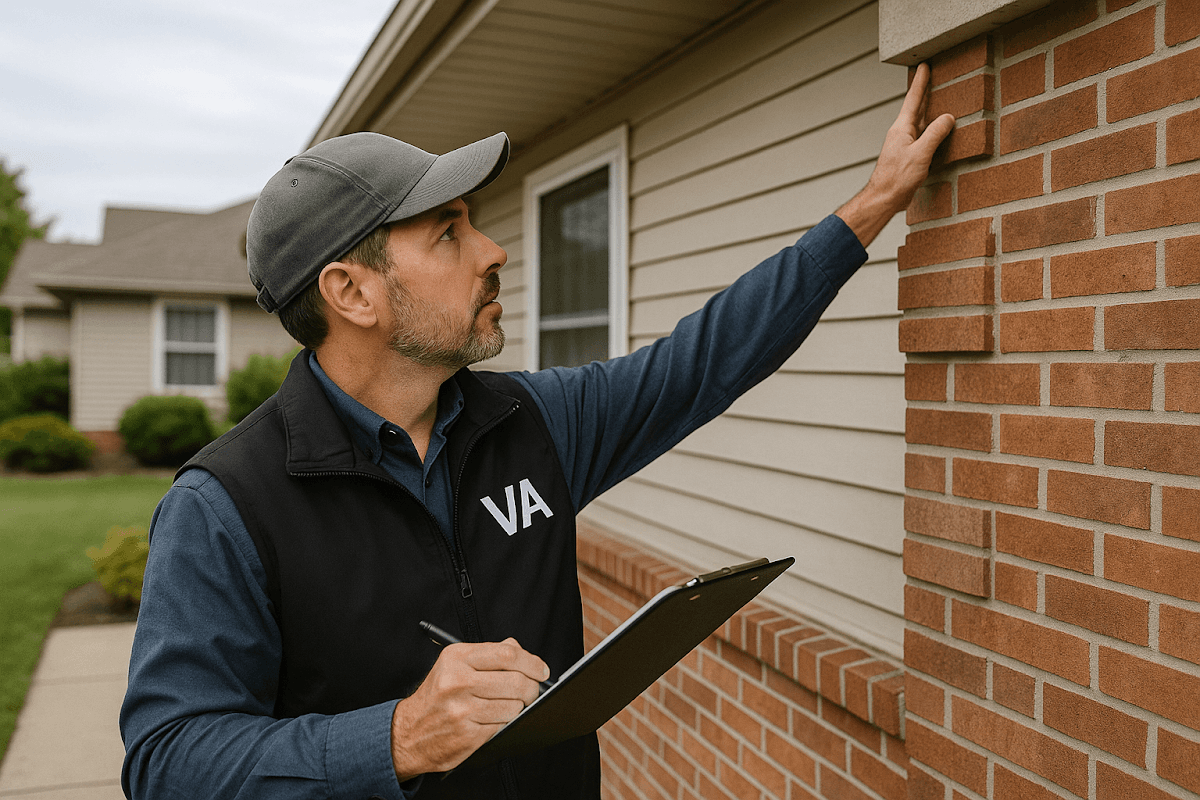

The Department of Veterans Affairs has established comprehensive property standards that go beyond typical mortgage inspections. These standards ensure that veterans receive homes that are safe, sanitary, and structurally sound. VA loan inspection requirements cover everything from the foundation to the roof, focusing on protecting your investment and well-being.

Unlike conventional loans that might only require basic appraisals, VA loans mandate thorough property evaluations. The inspector examines structural integrity, electrical systems, plumbing, heating and cooling systems, and overall safety features. This detailed approach helps veterans avoid purchasing properties with hidden defects that could become costly problems later.

The VA's property standards also consider the home's long-term value and marketability. This means the property must not only be livable today but also maintain its value over time. These requirements protect both you as the borrower and the VA as the loan guarantor, creating a win-win situation for everyone involved.

Essential Safety and Structural Evaluations

Safety takes center stage in VA property inspections, with specific focus on elements that could pose risks to occupants. Inspectors carefully examine the home's foundation for cracks, settling, or water damage that might compromise structural integrity. They also evaluate the roof condition, looking for missing shingles, leaks, or damage that could lead to interior problems.

Electrical systems receive thorough scrutiny during VA inspections. The electrical panel, wiring, and outlets must meet current safety codes to prevent fire hazards or electrocution risks. Similarly, plumbing systems are checked for proper function, adequate water pressure, and absence of leaks that could cause water damage or health concerns.

Heating and cooling systems are essential components that inspectors evaluate for both functionality and safety. The HVAC system must adequately heat and cool the entire living space while operating safely without carbon monoxide risks or other hazards. Windows and doors are also examined to ensure they provide proper security and weatherproofing.

Common Issues That May Require Repairs

Several common problems frequently arise during VA loan inspections that may need addressing before loan approval. Peeling paint in homes built before 1978 often requires remediation due to potential lead paint hazards. This is particularly important in homes where children might live, as lead exposure can cause serious health problems.

Faulty electrical systems, including outdated wiring or improperly installed outlets, commonly require updates to meet VA standards. Plumbing issues such as low water pressure, leaking pipes, or non-functional fixtures may also need repair before the loan can proceed. These fixes protect your investment and ensure the home meets habitability standards.

Structural problems like damaged foundations, compromised roofing, or inadequate support beams typically require professional repair before VA loan approval. While these issues might seem daunting, identifying them early through the inspection process prevents you from purchasing a property with expensive hidden problems that could surface later.

The VA Appraisal Process Explained

The VA appraisal process combines property valuation with inspection requirements, creating a comprehensive evaluation of your potential home purchase. A VA-approved appraiser conducts this assessment, examining both the property's market value and its compliance with VA standards. This dual approach ensures you're not overpaying for a property while also confirming it meets quality requirements.

During the appraisal process, the appraiser documents any deficiencies that need correction before loan approval. They create a detailed report outlining the property's condition, required repairs, and estimated value. This information helps determine whether the property qualifies for VA financing and if the purchase price aligns with current market values.

The appraisal typically takes several days to complete after the on-site inspection. The appraiser needs time to research comparable sales, analyze market conditions, and prepare the comprehensive report. Understanding this timeline helps you plan accordingly and set realistic expectations for your home buying process.

Preparing for Your VA Property Inspection

Preparation can significantly improve your VA loan inspection experience and increase the likelihood of a smooth approval process. Work with your real estate agent to conduct a preliminary walkthrough of the property before the official inspection. This allows you to identify potential issues early and discuss them with the seller.

Consider hiring an independent home inspector in addition to the VA appraisal, especially for older properties or homes with unique features. While this creates an additional expense, it provides more detailed information about the property's condition and helps you make informed decisions about your purchase.

Ensure the property is accessible for the inspection by confirming utilities are connected and functional. The appraiser needs to test electrical systems, plumbing, and HVAC equipment, which requires these systems to be operational. Coordinate with the seller to ensure the property is ready for evaluation on the scheduled inspection date.

Working with Sellers on Required Repairs

When VA inspections identify required repairs, effective negotiation with sellers becomes crucial for successful loan approval. Most sellers understand that VA loan requirements are non-negotiable and may be willing to complete necessary repairs to close the sale. Your real estate agent can help navigate these discussions and find mutually acceptable solutions.

Consider requesting repair credits or price reductions instead of having sellers complete the work directly. This approach gives you more control over repair quality and contractor selection while potentially speeding up the closing process. However, ensure any agreed-upon repairs meet VA standards before finalizing the transaction.

Document all repair agreements in writing and obtain proper permits for electrical, plumbing, or structural work when required. The VA may require re-inspection after repairs are completed, so maintaining clear documentation helps ensure a smooth approval process. Professional contractors should handle major repairs to guarantee they meet VA standards and local building codes.

Timeline and Next Steps After Inspection

After the VA inspection is complete, you'll typically receive the appraisal report within 7-10 business days, depending on the appraiser's workload and report complexity. This document outlines any required repairs, property value assessment, and recommendations for loan approval. Review this report carefully with your lender and real estate agent.

If repairs are required, work with the seller to establish a timeline for completion and schedule any necessary re-inspections. Most repairs must be completed before loan closing, though some minor issues might be addressed through escrow holdbacks or other arrangements approved by your lender.

Once all VA requirements are satisfied and repairs completed, your loan can proceed to final underwriting and closing preparation. This process typically takes several additional weeks, so factor this timeline into your overall home buying schedule. Stay in close communication with your lender throughout this period to address any additional requirements or questions that may arise.

●Conclusion

VA loan inspection requirements provide valuable protection for veterans making one of life's largest investments. While the process might seem comprehensive, these standards ensure you're purchasing a safe, habitable property that maintains its value over time. By understanding what inspectors look for and preparing accordingly, you can navigate the VA loan process with confidence and secure the quality home you deserve for your service to our country.