For military veterans and active-duty service members, VA loans represent one of the most valuable home financing benefits available. These government-backed mortgages offer competitive rates, no down payment requirements, and flexible qualification standards. However, many veterans wonder about the credit score requirements and whether they'll qualify for this powerful homebuying tool. Understanding VA loan credit score requirements can help veterans navigate the approval process more effectively and secure the home financing they deserve.

Understanding VA Loan Credit Score Standards

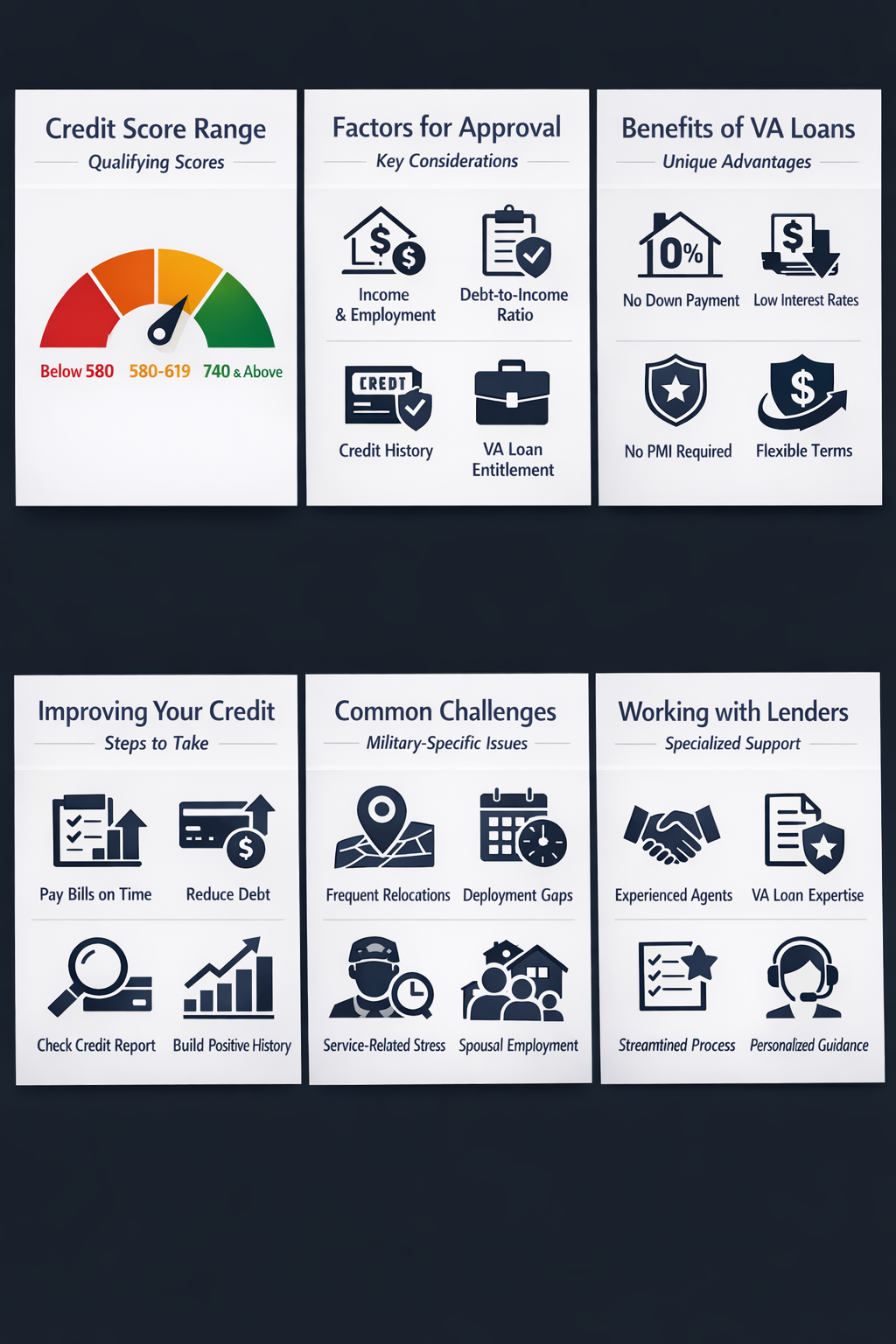

VA loans typically offer more flexible credit requirements compared to conventional mortgages, though specific standards may vary among lenders. Most financial institutions approve VA loans with credit scores starting around 620, though some lenders might accept lower scores with compensating factors.

The Department of Veterans Affairs doesn't establish a minimum credit score requirement, leaving this decision to individual lenders. This flexibility means veterans with less-than-perfect credit might still qualify for VA financing. However, borrowers with higher credit scores often secure better interest rates and more favorable loan terms.

Credit scores between 620 and 679 generally qualify for VA loans, while scores above 680 typically receive the most competitive rates. Veterans with scores below 620 might still find approval through specialized lenders who focus on serving military borrowers with unique financial circumstances.

Factors Beyond Credit Scores in VA Loan Approval

While credit scores matter, VA lenders evaluate multiple factors when reviewing loan applications. Debt-to-income ratio plays a crucial role, with most lenders preferring ratios below 41% though some flexibility exists for strong applications.

Employment history and income stability often compensate for lower credit scores. Veterans with steady employment, military pensions, or disability benefits might qualify despite credit challenges. Residual income requirements ensure borrowers can afford monthly expenses after mortgage payments.

Cash reserves and down payment funds can strengthen applications, even though VA loans don't require down payments. Having savings demonstrates financial responsibility and provides additional security for lenders considering borderline applications.

Improving Your Credit Profile for VA Loan Success

Veterans planning to apply for VA loans can take specific steps to strengthen their credit profiles. Paying down existing debt reduces credit utilization ratios, which significantly impacts credit scores. Keeping credit card balances below 30% of available limits demonstrates responsible credit management.

Addressing any errors on credit reports can quickly boost scores. Veterans should review reports from all three major credit bureaus and dispute inaccuracies promptly. Many service members find success working with credit repair services that specialize in military finances.

Establishing consistent payment patterns several months before applying helps demonstrate creditworthiness. Even small improvements in credit scores can result in better interest rates, potentially saving thousands over the loan term.

VA Loan Benefits That Offset Credit Requirements

VA loans offer unique advantages that make homeownership accessible despite credit challenges. The government guarantee reduces lender risk, enabling more flexible underwriting standards than conventional loans typically allow.

No private mortgage insurance requirements mean lower monthly payments, making homes more affordable for veterans with modest incomes. This benefit can offset concerns lenders might have about borderline credit scores by improving overall loan affordability.

VA loan assumability allows qualified buyers to take over existing loans, potentially providing exit strategies if financial circumstances change. These built-in protections encourage lenders to approve applications they might decline for conventional financing.

Working with Specialized VA Lenders

Choosing lenders experienced with VA financing can significantly improve approval odds for veterans with credit concerns. These specialists understand military compensation structures, deployment impacts on credit, and unique circumstances affecting service members.

VA-approved lenders often have more flexible underwriting guidelines and experience evaluating military-related income sources. They might consider factors like combat pay, housing allowances, and disability benefits that traditional lenders might overlook or undervalue.

Many specialized lenders offer pre-qualification services that help veterans understand their borrowing capacity before house hunting. This preparation allows veterans to address potential credit issues and strengthen their applications before formal loan submission.

Common Credit Challenges for Military Borrowers

Military service can create unique credit situations that civilian lenders might not fully understand. Frequent relocations can result in missed payments or difficulty maintaining consistent banking relationships, affecting credit histories.

Deployment-related financial management challenges sometimes impact credit scores. Service members might struggle with automatic payments, identity theft, or financial power of attorney issues while overseas. These circumstances often have legitimate explanations that experienced VA lenders can evaluate appropriately.

The Servicemembers Civil Relief Act provides certain protections for active-duty personnel, including interest rate reductions on pre-service debt. Understanding these protections can help veterans improve their overall financial picture before applying for VA loans.

Strategies for VA Loan Credit Success

Veterans can maximize their VA loan approval chances by preparing comprehensive loan packages that tell their complete financial story. Documentation explaining credit challenges, such as medical bills or deployment-related issues, can help lenders make informed decisions.

Consider working with housing counselors approved by the Department of Veterans Affairs or HUD. These professionals provide free guidance on credit improvement, budgeting, and homebuying preparation specifically tailored to military borrowers.

Timing applications strategically can improve outcomes. Veterans should avoid applying during periods of financial stress and instead wait until their credit and income situation stabilizes. This patience often results in better loan terms and smoother approval processes.

●Conclusion

VA loan credit score requirements offer veterans significant flexibility compared to conventional mortgage options. While most lenders prefer credit scores of 620 or higher, the combination of government backing, specialized underwriting, and unique military circumstances often enables approval for deserving veterans with lower scores. By understanding these requirements, working with experienced VA lenders, and taking steps to strengthen their credit profiles, veterans can successfully navigate the home financing process. The key lies in preparation, documentation, and choosing lenders who truly understand the military experience and its impact on personal finances.