When exploring financing options for rural property investments, many potential investors wonder about USDA loans for investment property. These government-backed loans offer attractive benefits for rural homebuyers, but their specific restrictions and requirements can create confusion for real estate investors. Understanding the relationship between USDA loans and investment properties is crucial for making informed financing decisions in rural markets.

Understanding USDA Loan Program Fundamentals

The USDA Rural Development loan program was designed to promote homeownership in eligible rural and suburban areas across the United States. These loans typically offer zero down payment options and competitive interest rates for qualified borrowers. The program aims to strengthen rural communities by making homeownership more accessible to families with modest incomes.

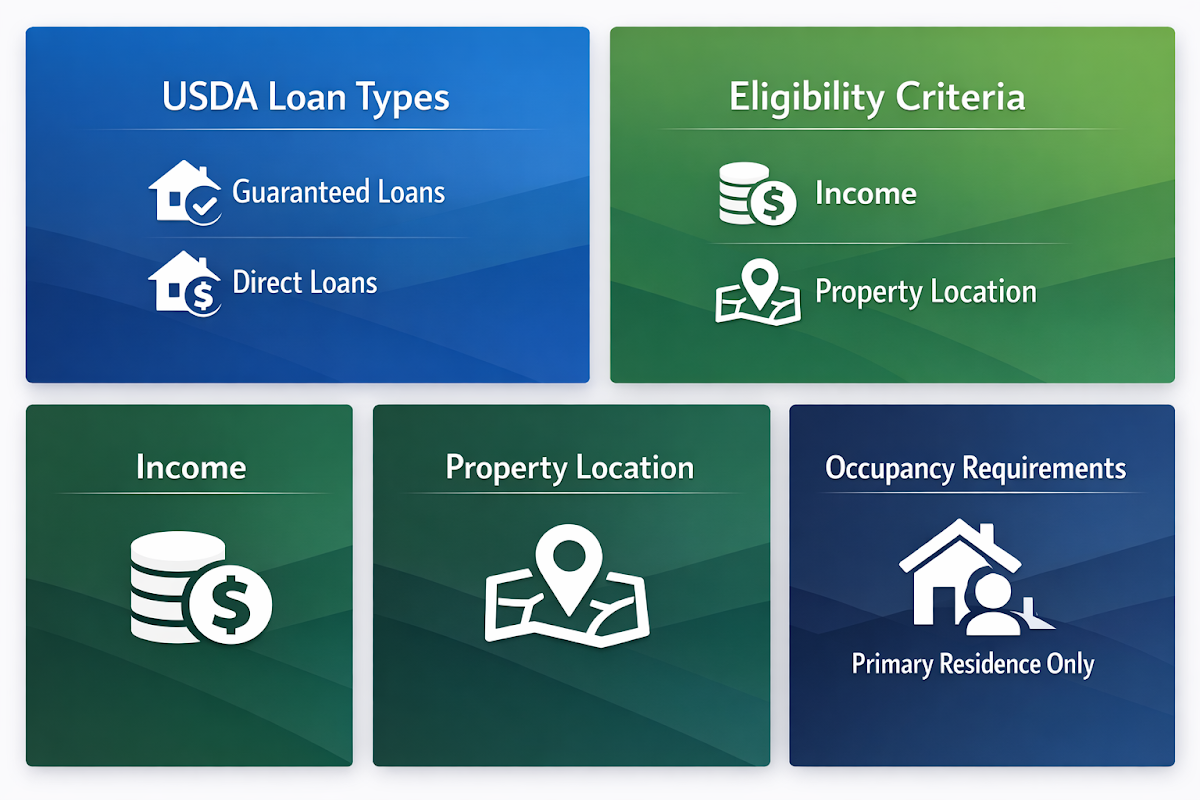

USDA loans come in two main varieties: guaranteed loans backed by private lenders and direct loans funded directly by the government. Both programs focus on serving families who might otherwise struggle to secure conventional financing in rural areas. The properties must be located in USDA-designated eligible areas, which generally include communities with populations under 35,000 residents.

Income limits apply to USDA loan applicants, typically requiring household income to fall within 115% of the area median income for guaranteed loans. These requirements reflect the program's mission to serve moderate-income families rather than high-earning investors seeking additional properties for their portfolios.

Investment Property Restrictions and Limitations

USDA loans maintain strict occupancy requirements that effectively prohibit their use for traditional investment properties. Borrowers must intend to use the financed property as their primary residence, living in the home for the majority of the year. This fundamental requirement eliminates the possibility of using USDA financing for rental properties or vacation homes.

The program includes specific language prohibiting the purchase of properties intended for investment purposes. Borrowers must certify their intention to occupy the property as their primary residence, and violations of this requirement can result in loan acceleration or other serious consequences. These restrictions help ensure program resources reach their intended beneficiaries rather than real estate investors.

Additionally, USDA loans cannot be used to purchase properties that generate rental income at the time of purchase. Even mixed-use properties with rental components typically don't qualify for USDA financing. The program's focus remains firmly on supporting primary residence purchases for eligible families in rural communities.

Eligible Property Types Under USDA Guidelines

USDA loans can finance various property types, but all must serve as the borrower's primary residence. Single-family detached homes represent the most common eligible property type, provided they meet program standards and are located in qualifying rural areas. These properties must be in decent, safe, and sanitary condition without need for major repairs.

Manufactured homes may qualify for USDA financing if they meet specific requirements, including permanent foundation installation and compliance with HUD standards. The home must be classified as real property rather than personal property, which often requires proper foundation work and removal of wheels and axles.

Some multi-unit properties might be eligible under certain circumstances, but only if the borrower occupies one unit as their primary residence and the property doesn't exceed program guidelines. However, these situations are relatively rare and require careful evaluation of program requirements and property characteristics.

Geographic Limitations and Rural Designation Requirements

USDA loan eligibility depends heavily on property location within designated rural areas. The program defines rural areas as communities with populations of 35,000 or fewer, though some exceptions exist for certain suburban areas that maintain rural characteristics. These geographic restrictions significantly limit where investors might consider using USDA financing, even if it were available for investment purposes.

Property locations must be verified through the USDA's online eligibility mapping system, which provides definitive answers about specific addresses. Areas that appear rural might not qualify if they're too close to metropolitan centers or if recent population growth has moved them outside program boundaries. These designations can change over time as communities develop and grow.

The geographic restrictions mean that potential real estate investments in many desirable rural areas might qualify location-wise, but the program's primary residence requirements still prevent investment use. Understanding these boundaries helps investors identify areas where alternative financing might be necessary for investment property purchases.

Alternative Financing Options for Rural Investment Properties

Conventional investment property loans offer the most straightforward alternative for financing rural rental properties. These loans typically require larger down payments, often 20-25%, and may carry higher interest rates than owner-occupied financing. However, they provide the flexibility to purchase investment properties in both rural and urban areas without occupancy restrictions.

Portfolio lenders and community banks often maintain more flexible underwriting standards for rural investment properties. These institutions might offer competitive terms for local real estate investors, especially those with established relationships or strong local market knowledge. Building relationships with regional lenders can open doors to financing options that larger national lenders might not provide.

Private money lenders and hard money loans represent additional options for rural investment property financing. These sources often provide faster closing times and more flexible qualification criteria, though typically at higher interest rates and shorter terms. For investors seeking to move quickly on rural opportunities, these options might prove valuable despite higher costs.

Converting USDA Financed Properties to Investments

Homeowners with existing USDA loans might wonder about converting their properties to investment use after a period of owner occupancy. USDA loan terms typically require borrowers to maintain the property as their primary residence for a specific period, often several years. Violating this requirement early in the loan term could trigger acceleration clauses or other penalties.

After satisfying the occupancy requirements, homeowners may have more flexibility to relocate and rent their USDA-financed property. However, this process requires careful review of loan documents and potentially communication with the loan servicer to ensure compliance with all program requirements. Some situations might require refinancing into a conventional investment property loan.

The conversion process might also trigger changes in property tax assessments or insurance requirements. Investment properties often face different tax treatment and insurance needs compared to primary residences. Property owners should consult with tax professionals and insurance agents before making such transitions to understand all implications.

Making Informed Rural Investment Decisions

Successful rural real estate investment requires understanding local market dynamics beyond just financing options. Rural markets often have different characteristics than urban areas, including longer holding periods, smaller tenant pools, and unique property management challenges. These factors should influence investment strategies and financing decisions.

Working with experienced rural real estate professionals can provide valuable insights into local market conditions and investment opportunities. Real estate agents, property managers, and local contractors familiar with rural markets can help investors identify promising opportunities and avoid potential pitfalls specific to rural property investment.

Developing comprehensive investment strategies that account for financing limitations helps investors build successful rural portfolios. This might include focusing on conventional financing from the start, building relationships with local lenders, or exploring creative financing arrangements that work within rural market constraints while meeting investment objectives.

●Conclusion

While USDA loans offer excellent benefits for rural homebuyers, their strict primary residence requirements prevent their use for investment properties. Real estate investors interested in rural markets must explore alternative financing options, including conventional investment loans, portfolio lenders, and private financing sources. Understanding these limitations and available alternatives helps investors make informed decisions about rural property investments and develop strategies that align with their financial goals and market opportunities.