For many homebuyers, the dream of owning a home in a quieter, more affordable community is very real — and the USDA loan program could help make that dream a reality. If you're eyeing a move-in ready home in an eligible rural or suburban area, understanding USDA loan requirements for existing homes is one of the most important steps you can take before starting your search. This government-backed mortgage program offers zero down payment options and competitive interest rates, but it does come with specific property and borrower guidelines that every buyer should know. Whether you're a first-time homebuyer or someone relocating to a smaller community, this guide walks you through everything you need to know.

What Is a USDA Loan and Who Backs It

The USDA loan — officially known as the USDA Rural Development Guaranteed Housing Loan — is a mortgage program backed by the U.S. Department of Agriculture. Its primary mission is to promote homeownership in rural and some suburban communities by making financing more accessible to low- and moderate-income households.

Unlike conventional mortgages, USDA loans do not require a down payment, which makes them particularly attractive for buyers who have steady income but haven't had the opportunity to build substantial savings. The program is divided into two main types: the Section 502 Guaranteed Loan Program, which works through approved private lenders, and the Section 502 Direct Loan Program, which is issued directly by the USDA for very low-income applicants.

It's worth noting that while the USDA program is well-known for supporting new construction, it's equally applicable — and in many cases, more commonly used — for purchasing existing homes. That makes understanding the specific rules around existing properties especially valuable for today's homebuyers.

Location Eligibility: The Rural Area Requirement Explained

One of the first hurdles buyers encounter is the geographic eligibility requirement. USDA loans are intended for properties in rural and certain suburban areas, and the USDA maintains an online eligibility map that buyers and lenders can use to check a specific address.

The term "rural" might bring to mind farmland or remote countryside, but in practice, many eligible areas are small towns or communities on the outskirts of larger cities. Towns with populations under 35,000 may qualify, depending on their classification and distance from urban centers. It's always a good idea to verify the property address directly on the USDA's official eligibility portal before falling in love with a listing.

For buyers pursuing a rural housing loan for existing construction, location is often the first filter applied. If the home sits in an ineligible area, no amount of borrower qualification will change that outcome. Checking location early in the home search process can save considerable time and effort.

USDA Loan Property Standards for Existing Homes

When it comes to USDA loan property standards, the bar is set to ensure that any home financed through the program is safe, structurally sound, and functionally adequate for the occupants. These guidelines exist to protect both the buyer and the government's financial interest in the loan.

Here are some of the core property condition requirements typically associated with USDA loans for existing homes:

- Structurally sound foundation and roof: The home must not have significant structural defects. A leaking or deteriorating roof, for example, would likely need to be repaired or replaced before the loan can close.

- Functional mechanical systems: Heating, plumbing, and electrical systems must be in working order and meet basic safety standards for the region.

- Adequate square footage: The home should be suitable as a primary residence. Very small or overcrowded dwellings may not meet program standards.

- No health or safety hazards: Issues such as exposed wiring, lead-based paint in poor condition, or faulty well and septic systems could trigger required repairs before approval.

- Modest and decent condition: The USDA program is designed to support modest homeownership, so properties that are considered luxury or investment-grade may not qualify.

A USDA appraisal is required for all purchase transactions, and the appraiser is trained to flag any conditions that fall short of the program's minimum property requirements. This appraisal serves a dual purpose: confirming the home's market value and verifying its compliance with USDA standards.

Borrower Eligibility: Income, Credit, and Other Key Factors

Beyond the property itself, borrowers must meet specific eligibility criteria to qualify for a USDA loan. Understanding the eligibility for a USDA existing property purchase involves looking at both the home and the person applying for the mortgage.

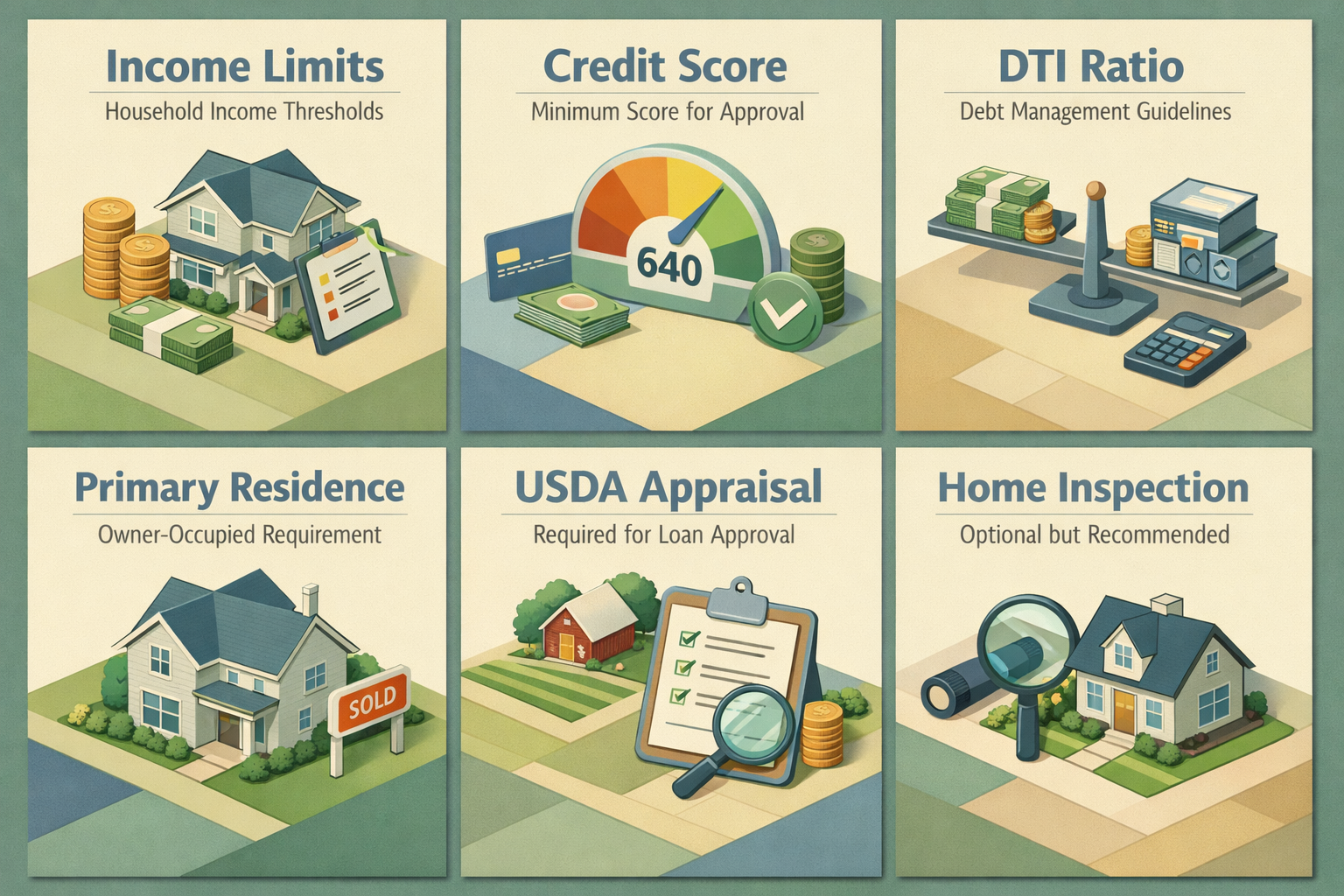

Income Limits

USDA loans are income-limited, meaning your household's total gross income must fall at or below a certain threshold to qualify. These limits vary by location and household size, and the USDA adjusts them periodically. Typically, income limits for the Guaranteed Loan Program are set at 115% of the area median income (AMI). Buyers should use the USDA's income eligibility tool to check their specific limit based on county and household size.

Credit Score Requirements

While the USDA program does not set a universal minimum credit score, most approved lenders look for a score of at least 640 for streamlined processing. Borrowers with scores below that threshold may still be considered, but they could face additional underwriting scrutiny and documentation requirements. A solid credit history with no recent derogatory events, such as foreclosure or bankruptcy, generally improves approval odds.

Debt-to-Income Ratio

Lenders will evaluate your debt-to-income (DTI) ratio to ensure you can manage the new mortgage payment alongside your existing obligations. A front-end DTI of around 29% (for housing costs) and a back-end DTI of around 41% (for all debt) are commonly cited benchmarks for USDA loans, though some lenders may allow exceptions with compensating factors.

Primary Residence Requirement

USDA loans are strictly for owner-occupied primary residences. Investment properties and vacation homes are not eligible. The borrower must intend to occupy the home as their main place of residence upon closing.

What Makes an Existing Home a Good Fit for USDA Financing

Not every existing home will sail through the USDA approval process, but many USDA loan for move-in ready homes situations work out smoothly when buyers know what to look for. Here's what tends to make an existing property a strong candidate:

- Updated mechanical systems: Homes with newer HVAC units, updated electrical panels, and modern plumbing tend to pass USDA appraisals with fewer flags.

- Sound roof and foundation: Properties with well-maintained roofs — ideally with several years of useful life remaining — and crack-free foundations are less likely to trigger repair conditions.

- Working well and septic system: In rural areas, many homes rely on private well water and septic systems. The USDA may require water quality testing and a septic system inspection to confirm functionality and safety.

- No deferred maintenance issues: Cosmetic issues like dated paint or old carpet are generally acceptable, but deferred maintenance that affects livability or safety could create hurdles.

- Modest market value: Since the program targets affordable homeownership, properties with extremely high valuations may fall outside the spirit — and sometimes the letter — of the program's guidelines.

Buyers who tour homes with these factors in mind are often better prepared to make offers on properties that have a realistic chance of USDA approval without costly repair negotiations.

The USDA Appraisal Process and How It Differs From a Home Inspection

A common point of confusion for buyers is the difference between a USDA appraisal and a standard home inspection. While both involve a professional evaluating the property, they serve different purposes and carry different weight in the transaction.

The USDA appraisal is ordered by the lender and is required as part of the loan approval process. The appraiser assesses the home's fair market value and checks that it meets the program's minimum property requirements. If the appraiser identifies conditions that must be repaired — such as a compromised roof or unsafe electrical work — those repairs typically need to be completed before the loan can close.

A home inspection, on the other hand, is an optional but highly recommended step that the buyer typically arranges independently. A licensed home inspector will provide a much more detailed assessment of the property's systems and components, often identifying issues that a USDA appraiser might not flag. For buyers purchasing an existing home through the USDA program, investing in a thorough home inspection is a smart strategy to uncover potential problems before they become costly surprises after closing.

In short, passing the USDA appraisal is a requirement; getting a home inspection is simply good practice that protects your investment.

Steps to Start the USDA Loan Process for an Existing Home

If you're ready to move forward, here's a practical roadmap for pursuing a USDA loan on an existing home:

- Check your income eligibility: Use the USDA's online tools to confirm your household income eligibility falls within the limits for your target area and family size.

- Review your credit profile: Pull your credit reports and scores early. Address any inaccuracies and work on improving your credit if needed before applying.

- Find a USDA-approved lender: Not all lenders participate in the USDA Guaranteed Loan Program. Working with an experienced lender familiar with USDA guidelines can help the process run more smoothly.

- Get pre-approved: A pre-approval letter gives you a clear budget and signals to sellers that you're a serious buyer with financing lined up.

- Search within eligible areas: Use the USDA eligibility map to focus your home search on qualifying locations. Your real estate agent can also help filter listings accordingly.

- Make an offer and schedule an appraisal: Once your offer is accepted, the lender will order a USDA appraisal. Be prepared to negotiate repairs if the appraisal uncovers conditions that must be addressed.

- Complete underwriting and close: After the appraisal clears and all conditions are met, your loan moves through final underwriting before reaching the closing table.

The timeline for a USDA loan can be slightly longer than a conventional mortgage — sometimes taking 30 to 60 days or more — largely because the file may need to go through a USDA conditional commitment process. Planning ahead and staying organized with your documentation can help minimize delays.

●Conclusion

Understanding USDA loan requirements for existing homes gives buyers a meaningful advantage in the home search process. From verifying location eligibility and meeting income thresholds to ensuring the property clears USDA appraisal standards, each step brings you closer to a zero-down mortgage on a home you'll love. The USDA program remains one of the most accessible paths to homeownership for buyers in rural and suburban communities, and existing homes represent the majority of purchases made through this program. If you're ready to explore your options, connect with a LoanWise mortgage specialist today — we're here to help you navigate the process from eligibility check to closing day.