For many homebuyers eyeing rural and suburban communities, the USDA home loan program offers a powerful path to homeownership — often with no down payment required. But one of the most common questions buyers and their agents ask is: how much can you actually borrow? Understanding USDA loan limits for existing homes is a key step in planning your purchase, especially since the program operates a little differently than conventional or FHA financing. Whether you're a first-time homebuyer or someone looking to relocate to a quieter community, getting clarity on these limits could save you time, frustration, and money.

What Makes USDA Loans Different From Other Mortgage Programs

The USDA loan program is backed by the U.S. Department of Agriculture and was created to encourage homeownership in eligible rural and some suburban areas. Unlike FHA or conventional loans, the USDA's Single Family Housing Guaranteed Loan Program doesn't set a rigid published loan limit in the same way that FHA does. Instead, the maximum loan amount is tied to the borrower's ability to repay and the appraised value of the property.

That said, this doesn't mean there's no cap at all. The USDA program uses income limits, debt-to-income ratios, and property value guidelines to determine how much a borrower may qualify for. This approach is designed to ensure that the loan remains affordable and within the spirit of supporting moderate-income households in rural housing markets.

There are two main USDA loan programs to be aware of:

- Section 502 Guaranteed Loan Program: The most widely used option, offered through approved private lenders and backed by the USDA. This program serves moderate-income borrowers.

- Section 502 Direct Loan Program: Issued directly by the USDA to low- and very-low-income applicants, with payment assistance available to keep monthly costs manageable.

Each program has its own structure, and the loan maximums can differ significantly between them. For most homebuyers working with a traditional mortgage lender, the Guaranteed Loan Program will be the relevant option.

How USDA Loan Maximum for Existing Houses Is Determined

When it comes to the USDA loan maximum for existing houses, the program doesn't publish a single national dollar cap the way FHA does with its county-level limits. Instead, the maximum loan amount a borrower can receive under the Guaranteed Loan Program is typically determined by two primary factors: the appraised value of the home and the borrower's qualifying income.

Here's how the calculation generally works:

- Appraised Value: The USDA will typically allow financing up to 100% of the home's appraised value. This means the loan amount is effectively capped at what a licensed appraiser determines the property is worth — not the purchase price alone.

- Income Limits: USDA loans are means-tested. Borrowers must fall at or below the area median income (AMI) for their county or region. These income thresholds vary by household size and location, and exceeding them may disqualify a borrower entirely.

- Debt-to-Income (DTI) Ratios: Lenders and the USDA typically look for a front-end DTI of around 29% and a back-end DTI of 41%, though exceptions may be granted with strong compensating factors.

It's also worth noting that the USDA may allow the loan to cover more than just the purchase price. Eligible costs such as closing costs, the upfront guarantee fee, and certain repairs to the existing home may be rolled into the loan — provided the total doesn't exceed the appraised value or applicable program caps.

Rural Housing Loan Limits by Area: Why Location Matters

One of the most important things to understand is that rural housing loan limits by area can vary considerably. While there isn't a strict published limit in the USDA Guaranteed program, the program's income limits, property eligibility maps, and local appraisal values all interact to create an effective ceiling in any given market.

The USDA updates its income limits annually, and these figures are broken down by county and household size. For example, a family of four in a low-cost rural county may face a different income ceiling than a similar family in a more expensive suburban fringe area. This matters because higher-income areas often feature higher home prices, and lenders may need to confirm that both the income qualification and the appraised value align with program guidelines before approving the loan.

For the USDA Direct Loan Program, loan limits are more explicitly defined. The program publishes loan limits by area in a format similar to FHA county-level caps. These limits can range from modest amounts in low-cost rural communities to higher thresholds in areas with elevated housing costs. Borrowers pursuing a Direct Loan should check USDA's official property eligibility and loan limit tools to understand the specific ceiling in their target area.

It's also worth confirming that the property itself falls within a USDA-designated eligible area. The USDA provides an online mapping tool that allows buyers to check any address for program eligibility. Many suburban communities near mid-sized cities may qualify, even if they don't feel traditionally "rural."

USDA Loan Eligibility for Existing Construction: What Buyers Should Know

A common misconception is that USDA loans are only for new construction. In fact, USDA loan eligibility for existing construction is very much a part of the program's design. Many buyers use USDA financing to purchase older homes in rural communities — provided those homes meet the program's property condition requirements.

For an existing home to qualify under the USDA Guaranteed or Direct Loan program, it generally must:

- Be a single-family dwelling intended as the borrower's primary residence

- Meet basic safety, sanitation, and structural standards

- Be in a USDA-eligible geographic area

- Have functional systems including heating, plumbing, and electrical

- Not have any major deficiencies that pose a health or safety risk without repair

If the appraiser identifies issues during the review, repairs may sometimes be required as a condition of loan approval. In certain cases, the cost of modest repairs may be included in the loan amount — though this is subject to program guidelines and shouldn't be assumed without lender confirmation.

Older homes are not automatically disqualified based on age alone, but they may face greater scrutiny during the appraisal process. Buyers interested in fixer-uppers should explore whether a USDA repair loan or the Section 504 Home Repair program might be a better fit for their situation.

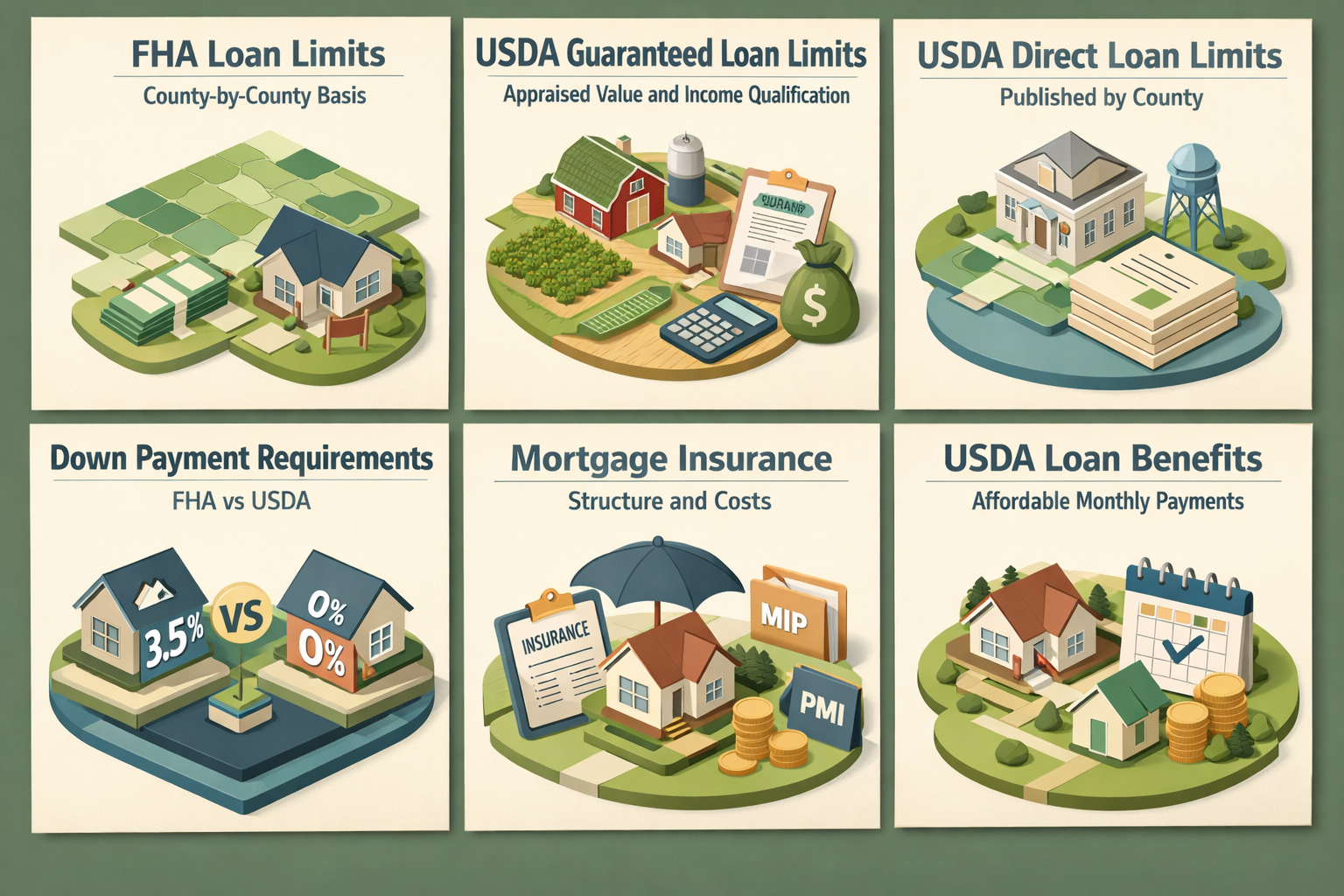

FHA Loan Limits vs USDA Limits: Key Differences for Rural Homebuyers

When evaluating financing options, many buyers weigh FHA loan limits vs USDA limits to determine which program fits their situation best. While both programs are government-backed and accessible to borrowers with moderate credit profiles, they work quite differently when it comes to loan ceilings and geographic restrictions.

Here's a side-by-side breakdown of how these programs compare:

- FHA Loan Limits: Set annually by HUD on a county-by-county basis. In lower-cost areas, the FHA floor limit for a single-family home may be around $498,257 for 2024, while high-cost areas can see limits significantly higher. FHA loans have no geographic restriction — they can be used in urban, suburban, or rural areas.

- USDA Guaranteed Loan Limits: Not published as a fixed dollar cap; instead capped by appraised value and income qualification. Borrowers must be within income limits and the property must be in an eligible rural or suburban area.

- USDA Direct Loan Limits: Published by county, often lower than FHA ceilings, specifically designed for low- and very-low-income borrowers.

- Down Payment Requirements: FHA requires a minimum 3.5% down payment (for those with a 580+ credit score). USDA Guaranteed loans may offer 100% financing with no down payment required.

- Mortgage Insurance: Both programs require mortgage insurance, though the structure and costs differ. USDA charges an upfront guarantee fee and an annual fee, while FHA charges an upfront MIP and monthly MIP.

For buyers purchasing in a USDA-eligible area who meet the income requirements, USDA financing often offers a more affordable monthly payment than FHA — largely because the annual fee is typically lower than FHA's monthly MIP. However, buyers in higher-cost rural markets or those who exceed USDA income limits may find that FHA offers greater flexibility.

Tips for Maximizing Your USDA Loan Approval in a Rural Market

Getting approved for a USDA loan — and securing the highest possible loan amount — often comes down to preparation. Here are several practical strategies homebuyers and refinancers can use to strengthen their application:

- Verify income eligibility early: Use the USDA's online income eligibility tool to confirm your household income falls within the limits for your specific county and household size before you begin shopping for homes.

- Check property eligibility: Use the USDA's address lookup tool to confirm your target home is in an eligible area. Don't assume — some areas near cities qualify, while others just outside rural zones may not.

- Work on your credit profile: While USDA doesn't set a hard minimum credit score, most approved lenders look for a score of at least 640 for streamlined underwriting. Scores below this threshold may still qualify but could require more documentation.

- Keep your DTI ratio in check: Reducing existing debt before applying can improve your debt-to-income ratio, which may allow you to qualify for a larger loan amount.

- Get a thorough home inspection: Since existing homes must meet USDA property condition standards, a detailed inspection before making an offer can help you identify any issues that might delay or jeopardize approval.

- Work with an experienced USDA lender: Not all lenders are equally familiar with USDA guidelines. Choosing one who regularly processes USDA loans can streamline the process and reduce the risk of surprises at closing.

●Conclusion

Understanding USDA loan limits for existing homes doesn't have to be overwhelming. While the Guaranteed Loan Program takes a more flexible approach to loan maximums — focusing on appraised value and income qualification rather than a published dollar cap — knowing how these factors interact puts you in a much stronger position as a buyer. Whether you're comparing FHA loan limits vs USDA limits, researching rural housing loan limits by area, or simply trying to confirm that an older farmhouse qualifies under USDA loan eligibility for existing construction, the key is to start early, gather the right information, and work with professionals who know the program well. At LoanWise, we're here to help you navigate every step of the rural homebuying journey with clarity and confidence. Ready to explore your USDA loan options? Connect with a LoanWise mortgage specialist today.