Buying a home is one of the most significant financial decisions a person can make, and for many Americans who receive Medicaid, the path to homeownership may feel uncertain. A common question among this group is whether receiving Medicaid benefits disqualifies them from getting a mortgage. The good news is that understanding medicaid recipient mortgage eligibility for home purchase is more straightforward than it might seem. Medicaid is a health coverage program — not a disqualifying financial marker — and with the right preparation, many Medicaid recipients may be well-positioned to pursue a home loan. This article explores the key factors lenders consider, the programs that may help, and the steps you can take to move closer to owning a home.

Does Receiving Medicaid Affect Your Ability to Get a Mortgage?

Many homebuyers on Medicaid worry that their enrollment in a government health program will automatically flag them as a high-risk borrower. The reality, however, is more nuanced. Medicaid itself is not a factor that mortgage lenders directly evaluate when reviewing a loan application. What lenders do assess are your income, credit history, debt-to-income ratio, and ability to repay the loan.

That said, Medicaid enrollment often intersects with financial circumstances — such as lower income levels or reliance on government assistance — that can influence mortgage qualification. The key distinction is that it's those underlying financial factors lenders are examining, not the Medicaid status itself. In other words, receiving Medicaid does not legally disqualify you from obtaining a mortgage.

Federal fair lending laws, including the Fair Housing Act and the Equal Credit Opportunity Act, prohibit lenders from discriminating against borrowers based on characteristics unrelated to creditworthiness. While these laws do not explicitly name Medicaid status as a protected class, lenders are still required to evaluate every applicant based on objective financial criteria. If your income, credit, and assets meet the required thresholds, you may be eligible for a home loan regardless of your health coverage source.

How Lenders View Income From Government Assistance Programs

One of the most important aspects of medicaid recipient home buying mortgage qualification is income documentation. Mortgage lenders need to verify that a borrower has stable, ongoing income sufficient to cover monthly mortgage payments. For Medicaid recipients, income may come from a variety of sources, and understanding which types lenders will accept is critical.

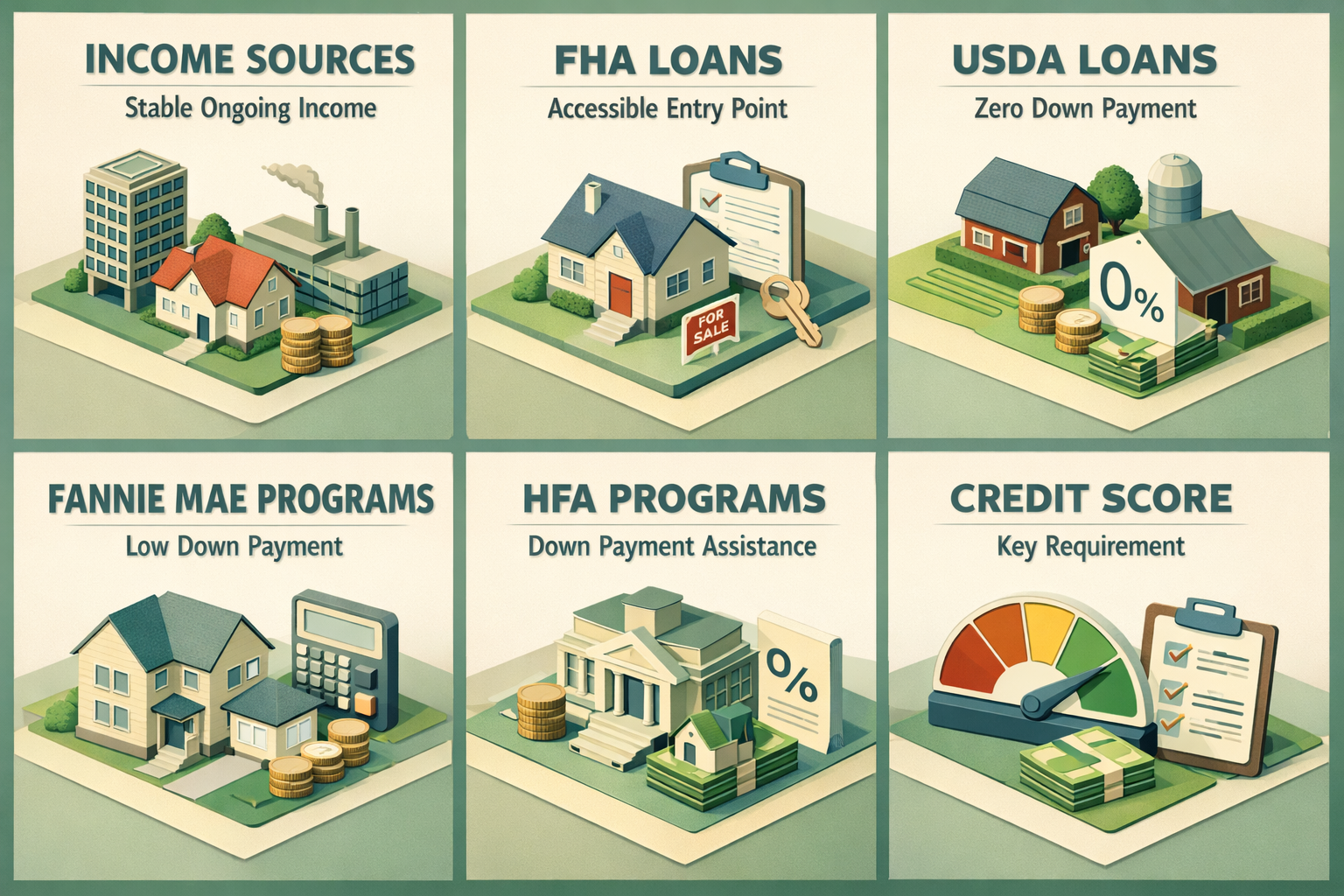

Lenders typically look for income that is likely to continue for at least three years from the loan closing date. Common income sources that Medicaid recipients might have include:

- Social Security Disability Insurance (SSDI): This is often considered stable, countable income by most lenders and loan programs.

- Supplemental Security Income (SSI): Some loan programs accept SSI as qualifying income, though the rules vary by lender and program type.

- Part-time or full-time employment wages: If a Medicaid recipient is also working, employment income is typically the primary qualifying source.

- Pension or retirement income: These are generally accepted if they can be documented as ongoing.

- Other benefit income: Certain programs may accept housing or other assistance income if it meets continuity requirements.

It's worth noting that Medicaid itself does not provide cash income — it provides health coverage. So the question isn't whether lenders will count Medicaid as income, but rather whether the borrower's other income sources are sufficient to support loan qualification. Borrowers should gather documentation such as benefit award letters, tax returns, and bank statements to support their application.

Loan Programs That May Be Accessible to Medicaid Recipients

Several mortgage programs may be particularly well-suited for homebuyers who are on Medicaid, especially those with modest incomes or limited savings for a down payment. Knowing which programs to explore could make the difference between renting indefinitely and owning a home.

FHA Loans

The Federal Housing Administration (FHA) loan program is a popular choice for borrowers with lower credit scores or limited down payment funds. FHA loans typically require a minimum down payment of 3.5% and accept lower credit scores than conventional loans. Because they are government-backed, lenders may be more flexible in how they evaluate non-traditional income sources. Medicaid recipients who have qualifying income from SSDI or employment may find FHA loans to be an accessible entry point.

USDA Loans

For homebuyers looking to purchase in rural or suburban areas, the U.S. Department of Agriculture's loan program offers zero-down-payment options for eligible borrowers. USDA loans have income limits, so applicants must fall within their area's qualifying thresholds — a factor that may actually work in favor of lower-income Medicaid recipients. Credit score requirements tend to be more flexible than conventional loans as well.

Fannie Mae and Freddie Mac Programs

Both Fannie Mae's HomeReady and Freddie Mac's Home Possible programs are designed for low-to-moderate income borrowers. These conventional loan options allow for down payments as low as 3% and may permit the use of income from household members or non-borrower contributors. They also accept certain non-traditional income types when properly documented, which could benefit borrowers who rely on disability income.

State Housing Finance Agency (HFA) Programs

Many states offer mortgage programs through their Housing Finance Agencies that include down payment assistance, reduced interest rates, and flexible underwriting guidelines for income-qualifying borrowers. These programs may be especially helpful for Medicaid recipients who meet the income criteria but need additional support with upfront costs.

Credit Score and Debt-to-Income Ratio Considerations for Borrowers on Medicaid

Beyond income, two of the most critical factors in mortgage approval are your credit score and your debt-to-income (DTI) ratio. These metrics help lenders assess how responsibly you've managed credit in the past and whether your current income can support new debt obligations.

Credit score requirements vary by loan program. FHA loans may accept scores as low as 580 with a 3.5% down payment, or even 500 with a larger down payment, though individual lenders may set higher minimums. Conventional loans generally require scores of 620 or above. If your credit score is on the lower end, there are steps you can take to improve it before applying — such as paying down revolving balances, disputing inaccuracies on your credit report, and avoiding new hard inquiries.

Debt-to-income ratio is calculated by dividing your total monthly debt payments by your gross monthly income. Most lenders prefer a DTI below 43%, though some programs allow higher ratios with compensating factors. For Medicaid recipients with fixed or modest income, managing existing debts carefully before applying for a mortgage could meaningfully improve eligibility.

It's also worth noting that some Medicaid recipients may have thin or limited credit histories rather than damaged credit — perhaps because they've relied primarily on cash or have avoided using credit altogether. In these cases, lenders may consider alternative credit data, such as on-time rent payments, utility bills, or insurance premiums, to establish creditworthiness. This option is more commonly available with FHA loans and some specialty programs.

The Impact of Medicaid's Asset Rules on Home Purchase Planning

One area where Medicaid and home purchase genuinely intersect is around asset rules. Medicaid eligibility — particularly for long-term care benefits — often involves strict asset limits. However, in most states, a primary residence is considered an exempt asset for Medicaid eligibility purposes. This means that owning a home generally does not disqualify you from Medicaid coverage.

That said, there are nuances worth understanding:

- Medicaid Estate Recovery: In many states, Medicaid programs can seek reimbursement from a recipient's estate after death for costs paid on their behalf. For homeowners, this may mean the state could place a claim on the home after the recipient passes away. This is sometimes called Medicaid estate recovery and is worth discussing with a legal or financial advisor before purchasing a home.

- Long-Term Care Medicaid vs. Standard Medicaid: Standard Medicaid (used for regular healthcare coverage) typically has more lenient asset rules than long-term care Medicaid. Homebuyers using standard Medicaid health coverage are less likely to encounter asset-related barriers to homeownership.

- State Variation: Medicaid rules vary significantly by state, so the specific impact on homeownership may differ depending on where you live. Consulting with a HUD-approved housing counselor or a benefits advisor familiar with your state's rules is strongly recommended.

Understanding these distinctions can help Medicaid recipients make informed decisions about how purchasing a home might affect their benefits over time.

Practical Steps to Strengthen Your Mortgage Application

Whether you're a first-time homebuyer or someone returning to the market after a financial setback, there are concrete steps that can improve your chances of mortgage approval. For individuals who are working through understanding medicaid recipient mortgage eligibility for home purchase, preparation is everything.

- Organize your income documentation: Gather benefit award letters, recent bank statements, W-2s or tax returns, and any other proof of recurring income. Lenders need a clear picture of your financial situation.

- Check your credit report: Review your credit report from all three major bureaus — Equifax, Experian, and TransUnion — and dispute any errors. You're entitled to a free report annually at AnnualCreditReport.com.

- Work with a HUD-approved housing counselor: These professionals offer free or low-cost guidance on the homebuying process and can help you understand which loan programs you may qualify for. They're especially helpful for borrowers navigating complex benefit situations.

- Explore down payment assistance: Many state and local programs offer grants or forgivable loans to help cover the down payment and closing costs. Income-qualifying Medicaid recipients may be well-positioned for these programs.

- Get pre-approved before you shop: A mortgage pre-approval gives you a realistic sense of what you can afford and signals to sellers that you're a serious buyer.

- Consult a benefits advisor: Before purchasing, speak with someone knowledgeable about how homeownership might interact with your specific Medicaid benefits. This step is especially important for those receiving long-term care Medicaid.

●Conclusion

Homeownership is a goal within reach for many Medicaid recipients who are willing to understand the process and prepare accordingly. While receiving Medicaid does not itself disqualify anyone from obtaining a mortgage, it's important to address the income, credit, and asset factors that lenders do evaluate. Programs like FHA loans, USDA loans, and state HFA options may provide accessible pathways — especially for those with lower incomes or limited savings. By gathering the right documentation, strengthening your credit profile, and consulting with housing and benefits professionals, you can move forward with confidence. LoanWise is here to help you explore your options and connect with lenders who understand your unique financial picture. Reach out today to take the first step toward your new home.