If you earn overtime pay regularly, you may be wondering whether that extra income can help you qualify for a home loan. The good news is that it often can — but the process isn't quite as straightforward as qualifying with a standard salary. Understanding how to calculate affordability for FHA loan with overtime requires knowing how lenders view variable income, what documentation they'll need, and how your debt-to-income ratio factors into the equation. This guide walks you through everything step by step, so you can approach the homebuying process with confidence.

What Makes FHA Loans a Popular Choice for Buyers with Non-Traditional Income

FHA loans, backed by the Federal Housing Administration, are well known for their flexible qualification standards. They're especially popular among first-time homebuyers, buyers with lower credit scores, and those whose income doesn't fit neatly into a traditional salary structure. Because many working Americans — including nurses, construction workers, factory employees, and first responders — rely on overtime pay to make ends meet, FHA guidelines have provisions that allow this income to be counted under the right circumstances.

The key distinction with FHA loans is that they're government-insured, which means lenders follow guidelines set by the Department of Housing and Urban Development (HUD). These guidelines provide a framework for how overtime and other forms of variable compensation may be treated during underwriting. While lender overlays can vary, the general principles remain consistent across most FHA-approved lenders.

FHA loans also offer relatively low down payment requirements — as low as 3.5% for borrowers who meet credit score thresholds — making them an accessible option for buyers who have stable employment but may not have large cash reserves. When overtime income is included correctly in your application, it could meaningfully increase your purchasing power.

How Lenders View Overtime for FHA Mortgage Qualification

One of the most important things to understand about the lenders view on overtime for FHA qualification is that not all overtime is treated equally. Lenders want to see that your overtime income is consistent, predictable, and likely to continue. A one-time bonus or a few extra hours here and there typically won't count. However, if you've been earning overtime steadily over a meaningful period, lenders may be willing to include it in your qualifying income.

Under standard FHA guidelines, overtime income may be considered if it has been received for at least two years and is expected to continue. This two-year history requirement is critical. Lenders will typically verify this through your W-2 forms, pay stubs, and tax returns. If your overtime has declined recently or is inconsistent, underwriters may average it differently or discount it entirely.

It's also worth noting that lenders will generally average your overtime income over the two-year period. If you earned significantly more overtime in one year than another, the averaged figure may be lower than your most recent earnings. This is why it helps to have a consistent track record rather than a spike in one particular period.

- Consistent history: Two or more years of documented overtime income is typically required.

- Continuation likelihood: Your employer may need to confirm that overtime opportunities are expected to remain available.

- Declining income caution: If your overtime has been decreasing year over year, lenders may use the lower figure or exclude it entirely.

- Documentation: Recent pay stubs, W-2s, and federal tax returns are standard requirements.

Step-by-Step: How to Calculate Affordability for FHA Loan with Overtime

Knowing how to calculate affordability for FHA loan with overtime starts with determining your effective qualifying income. Here's a practical breakdown of the process most lenders follow:

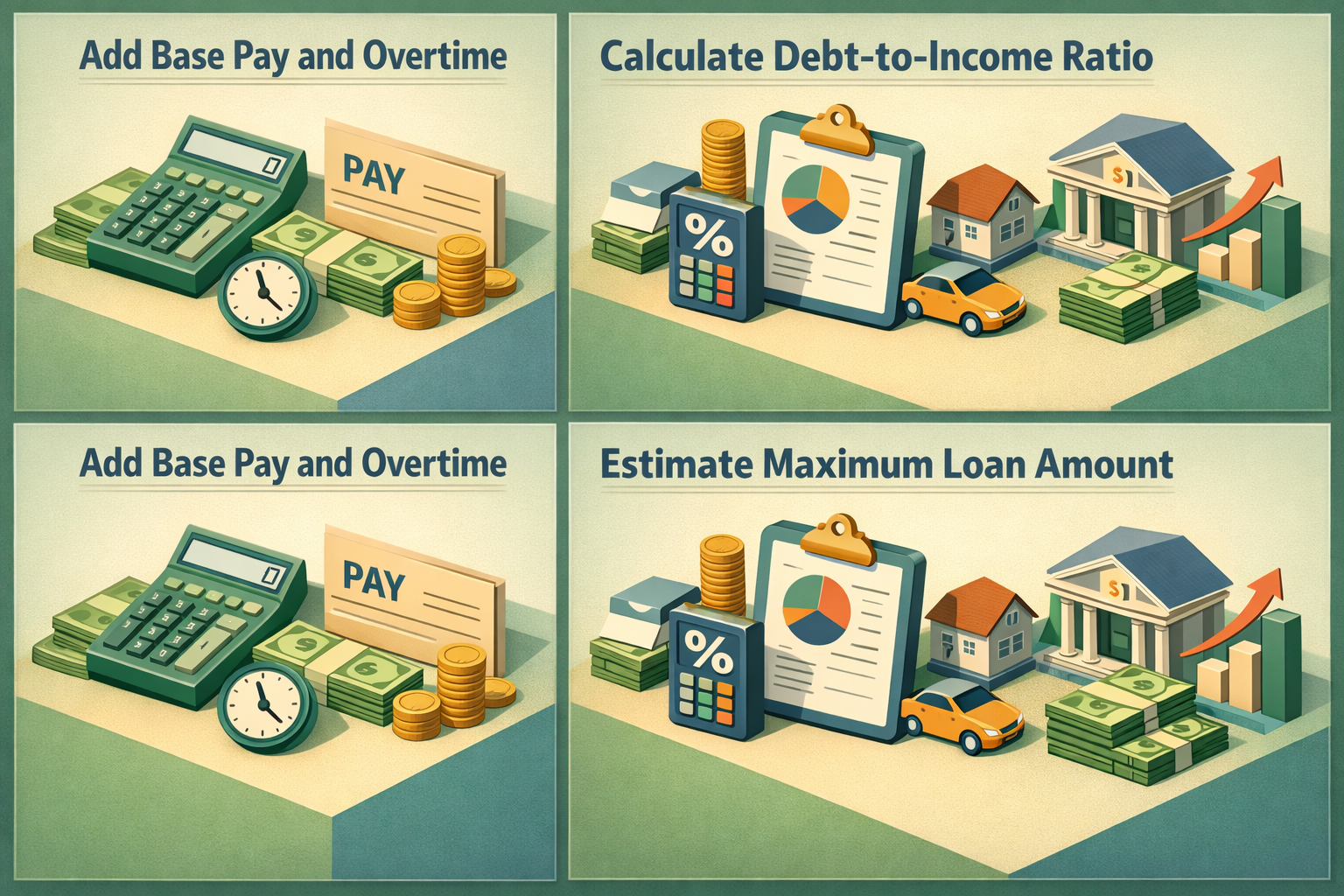

Step 1: Add Up Your Base Pay and Overtime

Start with your annual base salary. Then, add up your total overtime earnings over the past 24 months and divide by 24 to get your average monthly overtime. Add that figure to your monthly base pay. This combined number represents your gross monthly qualifying income.

For example, if your base salary is $4,000 per month and you averaged $800 per month in overtime over the past two years, your qualifying income would be approximately $4,800 per month — provided the income meets continuity requirements.

Step 2: Calculate Your Debt-to-Income Ratio

The DTI calculation FHA overtime process follows the same formula as any other income type. Your DTI compares your total monthly debt obligations to your gross monthly income. FHA guidelines generally look for a front-end DTI — housing expenses only — of no more than 31%, and a back-end DTI — all monthly debts combined — of no more than 43%. Some lenders with strong compensating factors may approve borrowers slightly above these thresholds.

Using the example above: if your qualifying income is $4,800 per month, your maximum allowable housing payment under the 31% front-end guideline would be roughly $1,488 per month. Your total monthly debts, including your new mortgage, should ideally fall at or below $2,064 per month under the 43% back-end cap.

Step 3: Estimate Your Maximum Loan Amount

Once you know your maximum housing payment, you can work backward using a mortgage calculator to estimate your maximum loan amount. Plug in the current interest rate, loan term (typically 30 years for FHA), and estimated property taxes and homeowner's insurance to arrive at a purchase price range. Don't forget to account for FHA mortgage insurance premiums, which include an upfront premium and an annual premium spread across monthly payments — these will reduce the portion of your payment that goes toward principal and interest.

Using an FHA Mortgage Calculator with Overtime Income Scenarios

An FHA mortgage calculator overtime income tool can save you a great deal of time and guesswork. Most online mortgage calculators allow you to input your gross monthly income, monthly debts, interest rate, loan term, and down payment to estimate how much home you may be able to afford. When using these tools with overtime income, make sure you're entering your averaged qualifying income — not your peak earnings — to get a realistic picture.

Here's what to keep in mind when running your numbers:

- Use gross income: Mortgage calculators work with pre-tax income figures, not take-home pay.

- Include all monthly debts: Car loans, student loans, credit card minimum payments, and any other recurring obligations should be factored in.

- Add FHA MIP: FHA loans carry both an upfront mortgage insurance premium (typically 1.75% of the loan amount) and an annual MIP that varies based on loan term and loan-to-value ratio. Make sure your calculator accounts for this.

- Factor in property taxes and insurance: These vary significantly by location and can meaningfully affect how much home you can afford.

Running multiple scenarios — such as higher vs. lower overtime averages, or different down payment amounts — can help you understand your range and set realistic expectations before speaking with a lender.

Qualifying for an FHA Loan with Variable Pay: Key Documentation Requirements

When qualifying for FHA loan with variable pay, documentation is everything. Lenders need a clear paper trail to verify that your overtime income is real, consistent, and likely to continue. Being organized and proactive about gathering your records can make the approval process significantly smoother.

Here's what you'll typically need to provide:

- Two years of W-2 forms: These show your total annual earnings broken down by employer and year, making it easy for underwriters to spot overtime trends.

- Recent pay stubs (30 days): Current pay stubs confirm that overtime is still being earned at the time of application. They should reflect your year-to-date earnings.

- Federal tax returns (two years): Tax returns provide additional verification, especially if you have multiple income sources or deductions that affect your adjusted gross income.

- Employer verification letter: Some lenders may request a written statement from your employer confirming that overtime opportunities are expected to remain available. While not always required, it can strengthen your file.

If your overtime income has been inconsistent — for example, high in one year and much lower in another — be prepared for the lender to use the lower or averaged figure. Transparency with your loan officer from the start can help avoid surprises during underwriting.

Common Challenges and How to Strengthen Your FHA Application

Even when overtime income is documented and consistent, borrowers may still face hurdles during the FHA approval process. Understanding these challenges ahead of time can help you take steps to improve your position before you apply.

High Debt-to-Income Ratio

One of the most common obstacles for buyers relying on overtime is a high back-end DTI. If your existing debts are significant, adding a mortgage payment — even with overtime income included — may push your DTI above acceptable levels. In this case, paying down debts before applying could meaningfully improve your qualifying ratios.

Inconsistent Overtime History

If your overtime has been irregular or you've recently changed jobs, lenders may be hesitant to include that income. Building a longer, more consistent track record at your current employer before applying could increase lender confidence.

Credit Score Concerns

FHA loans are more forgiving on credit scores than conventional mortgages, but your score still matters. A higher credit score may give you access to better interest rates and increase your chances of approval, especially if other aspects of your file — like your DTI — are close to the guideline limits.

Down Payment Planning

While FHA loans allow down payments as low as 3.5%, putting more down can reduce your loan amount and monthly payment, potentially bringing your DTI into a more comfortable range. It can also reduce your annual MIP costs depending on the loan-to-value ratio.

●Conclusion

Understanding how to calculate affordability for FHA loan with overtime is an essential first step for any buyer who depends on variable pay to support their household. While the process involves a few more moving parts than a straightforward salary-based application, it's absolutely manageable with the right preparation. By averaging your overtime income accurately, keeping your DTI within FHA guidelines, and assembling thorough documentation, you can build a strong case for approval. If you're ready to explore your options, speaking with an FHA-approved lender early in the process can help you get a clear picture of where you stand and what steps — if any — you may need to take before submitting your application. The path to homeownership may be closer than you think.