The tiny home movement has captured the imagination of millions of Americans looking for affordable, minimalist living. But when it comes to financing these compact dwellings, the path isn't always straightforward. Understanding FHA loan requirements for tiny homes with loft bedrooms is essential for any homebuyer who wants to use government-backed financing to purchase one of these unique properties. The Federal Housing Administration sets specific property standards that all homes must meet before a loan can be approved — and tiny homes with loft sleeping areas face some particular hurdles. This guide breaks down what you need to know so you can approach the process with confidence.

What Makes FHA Loans Appealing for Tiny Home Buyers

FHA loans are a popular choice among first-time homebuyers and those with modest savings because they typically require a lower down payment — often as little as 3.5% for borrowers with qualifying credit scores. The credit score thresholds are also generally more flexible compared to conventional loans, making FHA financing an attractive option for buyers who are still building their financial profiles.

For someone drawn to the affordability of a tiny home, an FHA tiny home loan can seem like the perfect combination. Lower purchase prices mean smaller loan amounts, and the government-backed nature of FHA financing can provide a measure of security for both borrower and lender. However, the FHA doesn't just evaluate the borrower — it evaluates the property just as carefully. This is where tiny home buyers often encounter unexpected challenges.

It's worth noting that the FHA doesn't technically have a separate loan product specifically labeled for tiny homes. Instead, tiny homes must qualify under the same FHA loan requirements that apply to all residential properties. That means your compact dream home must clear a series of property condition and structural standards before the loan can move forward.

Core FHA Property Standards Every Tiny Home Must Meet

The FHA requires that any home financed through its programs meet the Minimum Property Standards outlined in HUD's guidelines. These standards are designed to ensure the home is safe, sound, and sanitary for the occupants. For tiny homes, meeting these standards can be more challenging than it might be for a traditionally sized house.

- Minimum square footage: The FHA requires a home to have at least 400 square feet of living space. Many tiny homes fall right at or just above this threshold, so buyers should verify the exact measurements carefully.

- Permanent foundation: The home must be built on a permanent foundation. This immediately disqualifies most mobile or trailer-mounted tiny homes unless they've been permanently affixed to land that meets FHA standards.

- Adequate utilities: The property must have access to safe drinking water, functional plumbing, heating systems appropriate to the climate, and proper electrical systems.

- Structural integrity: Walls, roofing, and foundational elements must be in good condition and free from significant defects that could affect safety or habitability.

These standards apply regardless of the home's size. A tiny home that's thoughtfully designed and properly constructed can potentially meet all of these criteria — but buyers shouldn't assume compliance without having a qualified FHA appraiser evaluate the property.

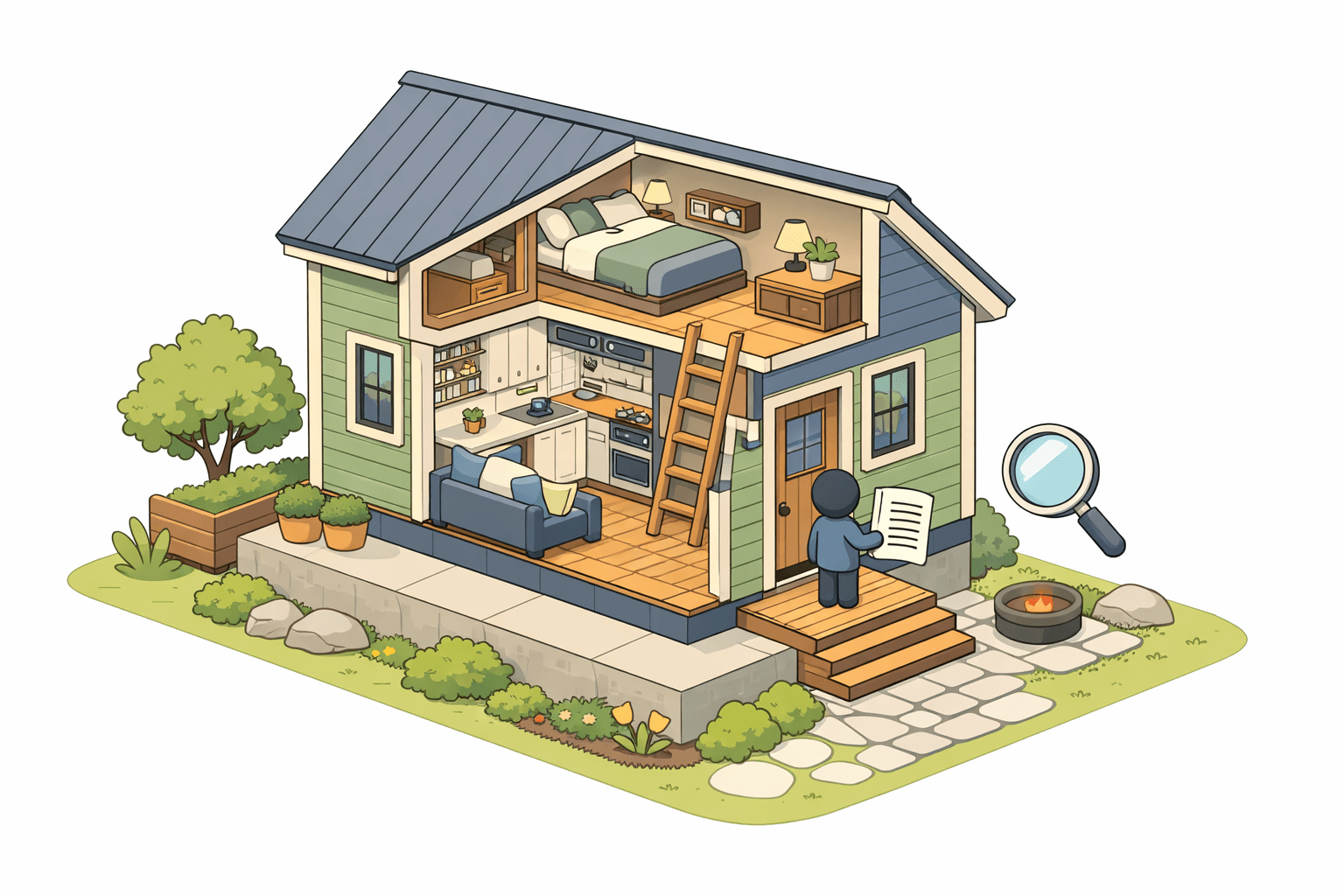

The Loft Bedroom Challenge: FHA Ceiling Height and Access Requirements

This is where understanding FHA loan requirements for tiny homes with loft bedrooms becomes particularly important. Loft sleeping areas are one of the most common design features in tiny homes, allowing builders to maximize square footage by stacking functional spaces vertically. However, FHA appraisers apply specific standards when evaluating whether a loft space qualifies as a legitimate bedroom.

The FHA generally follows guidelines that require habitable rooms — including bedrooms — to have a minimum ceiling height of at least 7 feet for the majority of the room's floor area. Many tiny home lofts, by design, have sloped or angled ceilings that drop well below this threshold. In those cases, the loft bedroom may not be recognized as a true bedroom by the FHA appraiser, which can affect the property's valuation and classification.

Beyond ceiling height, the FHA also considers how a loft is accessed. A sleeping area reached only by a ladder rather than a proper staircase may not meet habitability standards. The reasoning is rooted in safety — a fixed staircase provides safer egress in an emergency than a removable ladder. Some tiny home builders have addressed this by incorporating ship-style stairs or alternating-tread staircases, though whether these satisfy FHA requirements may depend on the individual appraiser's interpretation and local building codes.

Key Loft Bedroom FHA Requirements to Verify

- Ceiling height: Aim for at least 7 feet over the majority of the loft's usable floor area where possible.

- Stair access: A fixed staircase is generally preferred over a ladder for bedroom designation purposes.

- Egress windows: Bedrooms typically need at least one egress window of minimum dimensions to allow for emergency escape.

- Floor area: The sleeping space should meet minimum room size standards recognized under local building codes.

These loft bedroom FHA requirements aren't always uniformly enforced — local appraisers may interpret guidelines slightly differently — so it's wise to consult with an FHA-approved lender and appraiser before making a purchase offer on a tiny home with a loft.

How Tiny Home Classification Affects FHA Eligibility

One of the most important factors in determining FHA eligibility for a tiny home is how the property is legally classified. Not all tiny homes are created equal in the eyes of lenders and appraisers, and the classification can make or break your financing options.

Tiny homes that are built on a permanent foundation and classified as site-built residential properties have the strongest chance of qualifying for FHA financing, provided they meet all minimum property standards. These homes are treated much like any other single-family residence during the appraisal process.

Tiny homes built on wheels — sometimes called THOWs (Tiny Houses on Wheels) — are typically classified as recreational vehicles or personal property. FHA loans do not apply to RVs or personal property, which means these structures are generally ineligible regardless of how well-appointed they may be.

There's also the manufactured home pathway. FHA does have a specific program for manufactured homes (FHA Title I and Title II loans), which could potentially apply to factory-built tiny homes that meet HUD's manufactured housing construction standards. However, this pathway comes with its own set of requirements regarding foundation type, size, and construction standards that may or may not align with the typical tiny home design.

Working With an FHA-Approved Appraiser on Tiny Home Purchases

The FHA appraisal process plays a central role in determining whether a tiny home — loft bedroom and all — can qualify for financing. An FHA-approved appraiser doesn't just estimate market value; they also assess whether the property meets HUD's Minimum Property Requirements. For tiny homes, this dual evaluation can be more complex than for standard residential properties.

It's a good idea to connect with an appraiser who has experience evaluating non-traditional or alternative housing. An appraiser unfamiliar with tiny home construction might flag issues that an experienced evaluator would recognize as code-compliant alternatives. Similarly, working with an FHA tiny home loan lender who has processed tiny home loans before can help you anticipate potential issues before the appraisal stage.

Before submitting a formal loan application, consider requesting a preliminary walkthrough or consultation from a knowledgeable appraiser. They may be able to identify whether the loft ceiling height, staircase design, or egress windows could pose challenges. Addressing these issues proactively — either by negotiating repairs with the seller or selecting a property that already meets standards — could save significant time and expense later in the process.

Tips for Strengthening Your FHA Tiny Home Loan Application

Beyond property standards, your personal financial profile matters greatly when applying for an FHA loan. Here are some practical steps that may improve your chances of approval:

- Review your credit score: FHA loans typically require a minimum credit score of 580 for the 3.5% down payment option. Scores between 500 and 579 may still qualify but generally require a 10% down payment. Checking your credit report for errors before applying could give your score a meaningful boost.

- Calculate your debt-to-income ratio: FHA guidelines generally prefer a debt-to-income (DTI) ratio of 43% or lower, though some lenders may allow slightly higher ratios with compensating factors. Paying down existing debts before applying can help bring your DTI into a more favorable range.

- Document your income thoroughly: Self-employed buyers or those with non-traditional income sources should gather at least two years of tax returns, profit and loss statements, and bank records to demonstrate stable income.

- Save beyond the minimum down payment: Having additional reserves after closing can signal financial stability to lenders and may provide a buffer for any required repairs or improvements to the property.

- Choose the right property: Select a tiny home that's already on a permanent foundation, has a properly designed loft with adequate ceiling height, and has been built to local residential building codes.

Being well-prepared on both the borrower and property fronts gives your application the best possible foundation for success.

●Conclusion

Navigating understanding FHA loan requirements for tiny homes with loft bedrooms requires patience, preparation, and the right professional guidance. The FHA's property standards — particularly those affecting loft bedroom ceiling heights, stair access, egress, and minimum square footage — can present real obstacles for buyers drawn to the compact, efficient design of tiny homes. That said, these challenges aren't insurmountable. With a property that's thoughtfully constructed to residential standards, a solid borrower financial profile, and experienced professionals on your team, FHA financing for a tiny home is a realistic goal worth pursuing. At LoanWise, we're here to help you understand your options and connect with lenders who have real experience with specialty home financing. Reach out today to explore what's possible for your unique homebuying journey.