If you've been exploring government-backed home financing, you've likely come across the term FHA loan limits. For many homebuyers, especially those shopping in expensive metropolitan areas, these limits can feel confusing or even discouraging. The good news is that the Federal Housing Administration adjusts its borrowing caps based on where you live — meaning buyers in high-cost markets may qualify for a much higher FHA maximum loan amount than they'd expect. Understanding FHA loan limits for high cost areas is a critical step toward making smart financing decisions, whether you're a first-time buyer, a move-up buyer, or a real estate investor exploring options in a competitive city.

What Are FHA Loan Limits and Why Do They Exist

FHA loans are insured by the Federal Housing Administration and designed to help borrowers who may not qualify for conventional financing. Because the government backs these loans, it sets limits on how much a borrower can finance through the program. These caps — known as FHA loan limits — exist to ensure the program stays focused on moderate-income and first-time homebuyers rather than serving the luxury home market.

The limits are not one-size-fits-all. Instead, they're set at the county level and adjusted annually by the Department of Housing and Urban Development (HUD). Two key benchmarks shape this system:

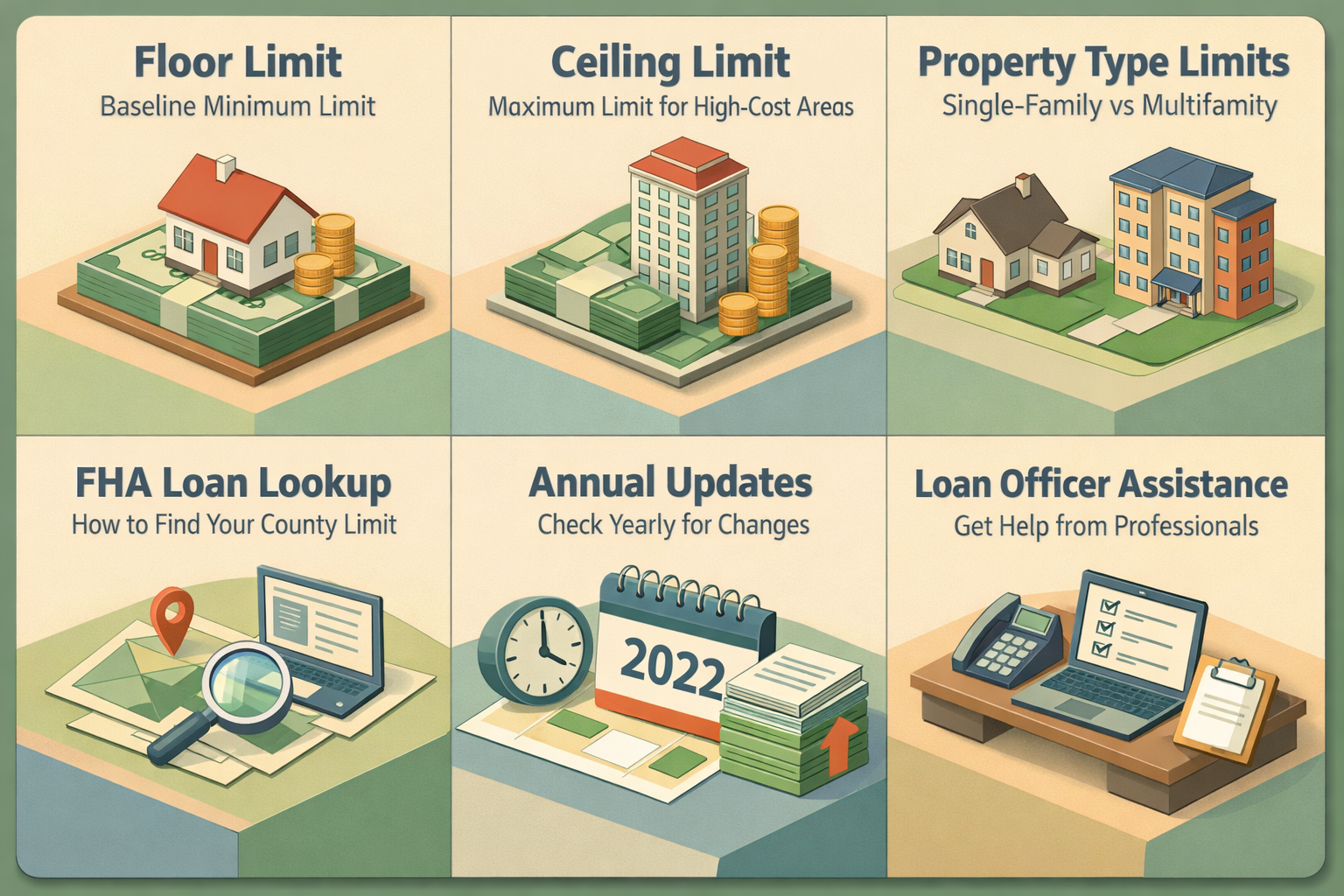

- Floor limit: The baseline minimum FHA loan limit that applies to lower-cost counties across the country.

- Ceiling limit: The maximum FHA loan amount allowed, which applies to designated high-cost counties and metro areas.

Each year, HUD reviews median home prices across the country and updates loan limits accordingly. This means the FHA mortgage limits by county you see today may differ from what was in place a year ago — so it's always worth checking current figures before making financing decisions.

How High-Cost Area Limits Are Calculated

The distinction between a standard county and a high-cost area comes down to median home prices. HUD calculates local FHA loan limits as a percentage of the conforming loan limits set by the Federal Housing Finance Agency (FHFA). In general terms:

- Counties where home prices are relatively modest receive the floor limit, which is typically set at 65% of the national conforming loan limit.

- Counties where home prices significantly exceed the national median may qualify for limits as high as 150% of the conforming loan limit — this is the ceiling.

- Counties that fall somewhere in between receive limits calculated based on local median home prices.

This tiered structure means that FHA mortgage limits by county can vary dramatically across the country. A homebuyer in a rural Midwestern county and a homebuyer in the San Francisco Bay Area are both eligible for FHA financing — but their maximum loan amounts could differ by hundreds of thousands of dollars.

It's also worth noting that limits differ depending on the property type. Single-family homes carry one limit, while two-unit, three-unit, and four-unit properties have progressively higher caps, reflecting the higher cost of multifamily housing. This makes FHA loans potentially attractive for real estate investors who plan to live in one unit of a small multifamily property.

Can I Get an FHA Loan in an Expensive City

One of the most common questions homebuyers ask is: can I get an FHA loan in an expensive city? The answer is often yes — but with important caveats. Many major metropolitan areas across the country are designated as high-cost regions, which means they receive elevated loan limits that may realistically align with local home prices.

Cities such as Los Angeles, New York, Seattle, Denver, and Miami, among others, tend to fall into high-cost or special exception categories. Buyers in these markets may access the ceiling FHA loan maximum loan amount rather than the national floor, giving them more purchasing power while still benefiting from the program's lower down payment requirements and flexible credit standards.

That said, even in high-cost areas, FHA loan limits may not cover the full price of the most expensive homes in that market. If the home you're targeting is priced above the FHA ceiling for your county, you'd need to either cover the gap with a larger down payment, pursue a conventional loan, or explore jumbo financing. Understanding this boundary is essential before you start house hunting in a pricey market.

Here's what typically makes FHA loans appealing even in expensive cities:

- Down payments as low as 3.5% for borrowers with qualifying credit scores

- More lenient debt-to-income ratio guidelines compared to some conventional products

- Competitive interest rates backed by government insurance

- Accessibility for borrowers with less-than-perfect credit histories

FHA Loan County Loan Limits Explained: How to Look Up Your Area

Looking up your county's specific FHA loan limit is simpler than many buyers realize. HUD publishes updated FHA loan county loan limits every year, typically toward the end of the calendar year to take effect at the start of the next. You can find this information through HUD's official website or through FHA-approved lenders who stay current with program guidelines.

When researching your county's limit, keep the following in mind:

- Search by county, not just city: FHA mortgage limits by county are set at the county level, so two neighboring cities in different counties could have different maximums.

- Check for annual updates: Limits can and do change year to year. Always verify the current limit rather than relying on figures from a prior year's search.

- Consider property type: Confirm you're looking at the right limit for your intended property — single-family versus multifamily limits are published separately.

- Ask your loan officer: A knowledgeable mortgage professional can quickly pull up the applicable limit for your target area and explain how it affects your purchasing options.

Being proactive about this research helps you avoid surprises during underwriting and ensures your target home price aligns with what the FHA program can actually support in your county.

How FHA Limits Interact With Down Payment and Purchase Price

It's important to understand that the FHA maximum loan amount refers to the loan amount — not the purchase price of the home. This distinction matters when you're calculating what you can afford. If your county's FHA loan limit is set at a specific ceiling, you may still be able to purchase a more expensive home by putting down a larger down payment.

For example, if the FHA loan limit in your county is $800,000 and you want to buy a home priced at $850,000, you'd need to cover the $50,000 difference in addition to your minimum required down payment. This combined approach can sometimes allow buyers to stay within the FHA program while reaching slightly higher price points.

However, buyers should also account for other costs associated with FHA financing, including:

- Upfront mortgage insurance premium (UFMIP): Typically rolled into the loan amount, this is a one-time fee charged at closing.

- Annual mortgage insurance premium (MIP): An ongoing monthly cost that continues for the life of the loan in many cases, depending on down payment size and loan term.

- Appraisal requirements: FHA appraisals follow specific HUD guidelines and may flag property condition issues that a conventional appraisal would not.

These factors don't diminish the value of FHA financing — but they're important to factor into your total cost comparison when evaluating whether an FHA loan is the right fit for your situation.

Special Exception Areas and Alaska, Hawaii, Guam, and the Virgin Islands

Beyond the standard high-cost area designation, certain geographic regions receive even higher FHA loan limits due to unique construction costs and market conditions. Alaska, Hawaii, Guam, and the U.S. Virgin Islands fall into this special exception category, and their FHA loan limits may exceed the standard national ceiling.

These elevated limits reflect the genuine cost realities of building and buying in these locations. Construction materials, labor, and logistics in island or remote environments tend to cost more than in the continental United States, and FHA's structure attempts to account for that reality.

If you're buying in one of these special exception areas, it's especially important to work with a lender familiar with local FHA guidelines. The nuances of applying for financing in these markets — from appraisal requirements to property eligibility — can differ meaningfully from the standard continental U.S. experience.

●Conclusion

Understanding FHA loan limits for high cost areas is one of the most practical things you can do before beginning your home search in a competitive market. These limits directly shape what you can borrow, how much you'll need to bring to closing, and whether the FHA program is even a viable path for the home you have in mind. The FHA mortgage limits by county system is designed to reflect real-world market variation — and in many cases, it provides meaningful flexibility for buyers in expensive cities who might otherwise assume they're priced out of government-backed financing.

Whether you're a first-time buyer trying to break into a high-cost market or a homeowner exploring refinance options in a pricey metro area, knowing your county's FHA loan limit puts you in a stronger position at the negotiating table and in the lender's office. Take the time to look up your local limits, talk with an FHA-approved lender, and make sure your target purchase price aligns with what the program can support. With the right information and guidance, FHA financing may be more accessible than you think — even in some of the country's most expensive markets.