Navigating Mortgage for Self-Employed Borrowers in Today's Market

Real estate investors who are self-employed face unique challenges when securing financing for their investment properties. The mortgage for self-employed borrowers has become increasingly complex, with lenders implementing stricter documentation requirements and tightened debt-to-income thresholds. However, understanding these evolving requirements and implementing strategic preparation can significantly improve your chances of securing favorable loan terms for your rental property acquisitions and refinancing needs.

As a self-employed real estate investor, your income documentation process differs substantially from traditional W-2 borrowers. Recent regulatory changes have reshaped the lending landscape, making it crucial to understand both the challenges and opportunities that lie ahead in 2026's mortgage market.

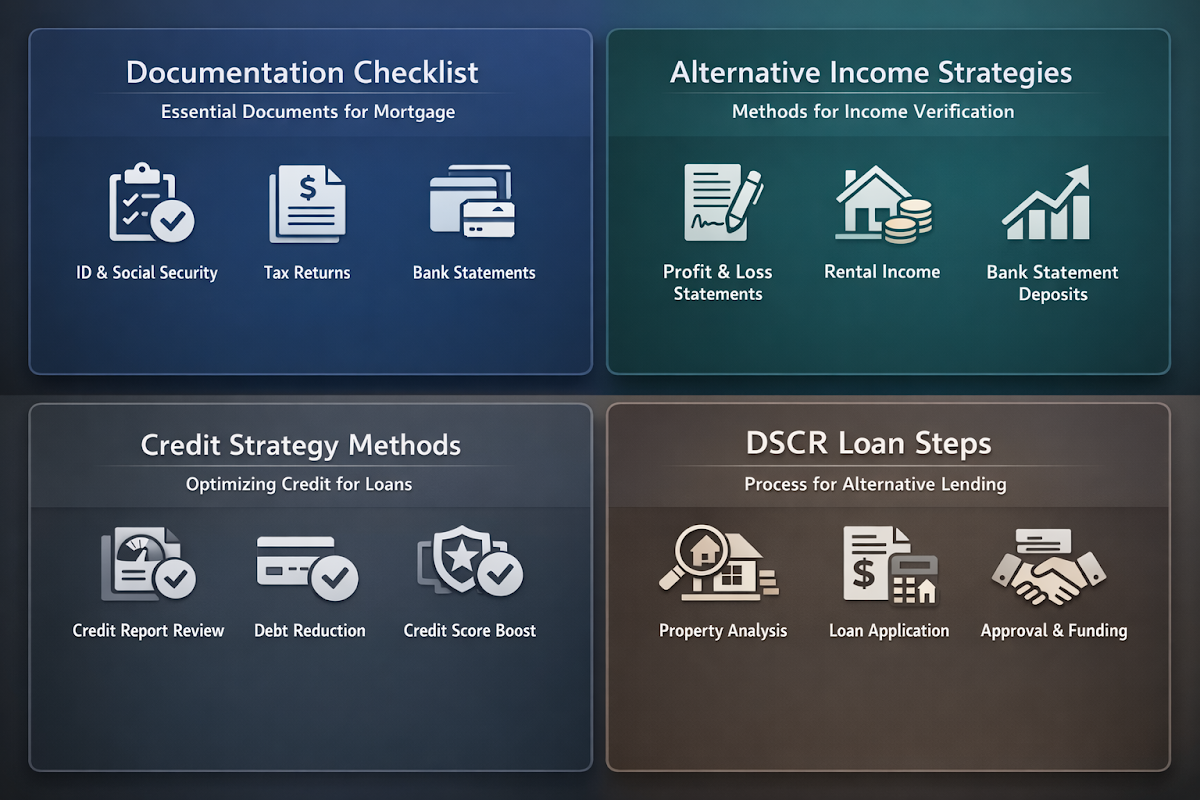

Essential Documentation Preparation Checklist

Essential documentation preparation checklist forms the foundation of successful mortgage applications for self-employed borrowers. Lenders now require comprehensive financial histories that demonstrate consistent income and business stability over extended periods.

- 24-month business bank statements showing consistent cash flow patterns and income deposits

- Two years of complete tax returns including all schedules and business profit and loss statements

- Current profit and loss statement prepared by a certified public accountant for the most recent quarter

- Business license and registration documents proving legitimate business operations and compliance

Alternative Income Documentation Strategies

Alternative income documentation strategies provide pathways for self-employed investors when traditional documentation might not fully represent their financial capacity. These methods can help bridge gaps in conventional income verification processes.

- Asset-based income calculations using investment portfolios and liquid assets to demonstrate repayment ability

- Rental income documentation from existing properties with lease agreements and rent rolls

- Business asset valuations including equipment, inventory, and real estate holdings

- Bank deposit analysis showing consistent cash flow over 12-24 months beyond basic statements

Credit Strategy Optimization Methods

Credit strategy optimization methods help self-employed borrowers align with new debt-to-income limits while maintaining strong creditworthiness. These approaches can significantly impact loan approval prospects in the current regulatory environment.

- Debt consolidation planning to reduce overall monthly obligations before mortgage application

- Business credit separation maintaining distinct personal and business credit profiles

- Strategic credit utilization keeping personal credit card balances below 30% of available limits

- Payment history consistency ensuring no missed payments across all accounts for 12+ months

DSCR Loan Application Process Steps

DSCR loan application process steps offer self-employed investors an alternative path to traditional income-based lending. These loans focus on property cash flow rather than personal income documentation.

- Property cash flow analysis: Calculate the debt service coverage ratio using rental income projections and property expenses to demonstrate the investment's ability to service the debt

- Leverage optimization: Structure down payment and loan amounts to achieve favorable DSCR ratios, typically 1.2 or higher for optimal rates

- Rental income documentation: Provide lease agreements, rent rolls, and market rent studies to support income projections for the subject property

- Property condition assessment: Ensure the investment property meets lender requirements and obtain necessary inspections before final approval

Strategic Refinancing Timing Considerations

Strategic refinancing timing considerations help self-employed investors capitalize on current market conditions while their financial documentation is optimally prepared. The timing of refinancing applications can significantly impact available rates and terms.

- Rate environment assessment: Monitor DSCR loan rates currently ranging between 6.00% and 7.50% to identify optimal refinancing windows

- Documentation readiness verification: Ensure all financial records are current and comprehensive before initiating the refinancing process

- Property performance evaluation: Analyze rental income stability and property appreciation to maximize loan-to-value ratios

- Portfolio diversification timing: Coordinate refinancing with acquisition plans to optimize overall portfolio leverage and cash flow

Key Success Factors for Self-Employed Mortgage Approval

Success in securing a mortgage for self-employed borrowers requires a comprehensive approach that addresses both traditional lending criteria and the unique challenges faced by self-employed real estate investors. The evolving regulatory landscape demands proactive preparation and strategic positioning to achieve favorable loan terms. Self-employed investors who maintain robust business histories, prepare extensive documentation, and adapt their credit strategies to conform with new debt-to-income limits position themselves for better approval prospects. Additionally, understanding alternative lending products like DSCR loans can provide valuable financing options when traditional income documentation might not fully capture an investor's financial capacity.

●Conclusion

The mortgage landscape for self-employed real estate investors continues to evolve, presenting both challenges and opportunities for those prepared to adapt. By focusing on comprehensive documentation preparation, exploring alternative income verification methods, and leveraging specialized loan products like DSCR financing, self-employed investors can successfully navigate the current lending environment.

Success in securing favorable mortgage terms depends largely on preparation and strategic positioning. Investors who proactively address documentation requirements, optimize their credit profiles, and work with lenders who understand the unique needs of self-employed borrowers will find themselves well-positioned to capitalize on investment opportunities in the current market.

As lending standards continue to evolve, staying informed about regulatory changes and maintaining strong financial records will remain crucial for self-employed real estate investors seeking to expand their portfolios through strategic financing.