For small business owners dreaming of owning their own commercial space or investing in major equipment, financing can feel like a steep mountain to climb. Traditional commercial loans often come with high down payments, short repayment windows, and variable interest rates that make long-term planning difficult. That's where the SBA 504 loan program steps in as a compelling alternative. Backed by the U.S. Small Business Administration, this program is designed to help entrepreneurs and small business borrowers access long-term, fixed-rate financing for major fixed assets — often at terms that are hard to match in the conventional lending market. Whether you're looking to purchase a building, expand an existing facility, or acquire heavy equipment, the SBA 504 loan may offer a practical path forward.

What Is the SBA 504 Loan Program?

The SBA 504 loan is a government-backed financing program specifically designed to support the growth and modernization of small businesses. Unlike general-purpose business loans, this program focuses on the acquisition of major fixed assets such as commercial real estate, large equipment, and long-term machinery. It's administered through Certified Development Companies (CDCs), which are nonprofit organizations regulated and certified by the SBA to work alongside private-sector lenders.

The structure of an SBA 504 loan is unique. It typically involves three parties: a private lender such as a bank or credit union, a CDC, and the borrower. The private lender usually covers approximately 50% of the total project cost, the CDC provides up to 40% through an SBA-backed debenture, and the small business owner contributes the remaining 10% as a down payment. This three-part structure is what makes the program so accessible — it significantly reduces the upfront capital burden on the business owner while spreading risk across multiple parties.

This program is not designed for working capital, inventory, or short-term business needs. Its strength lies in long-term, asset-backed investments that can help a business build equity and stability over time. For entrepreneurs ready to make a serious capital investment, the SBA 504 loan program could be one of the most cost-effective financing vehicles available.

Key Benefits That Make This Program Stand Out

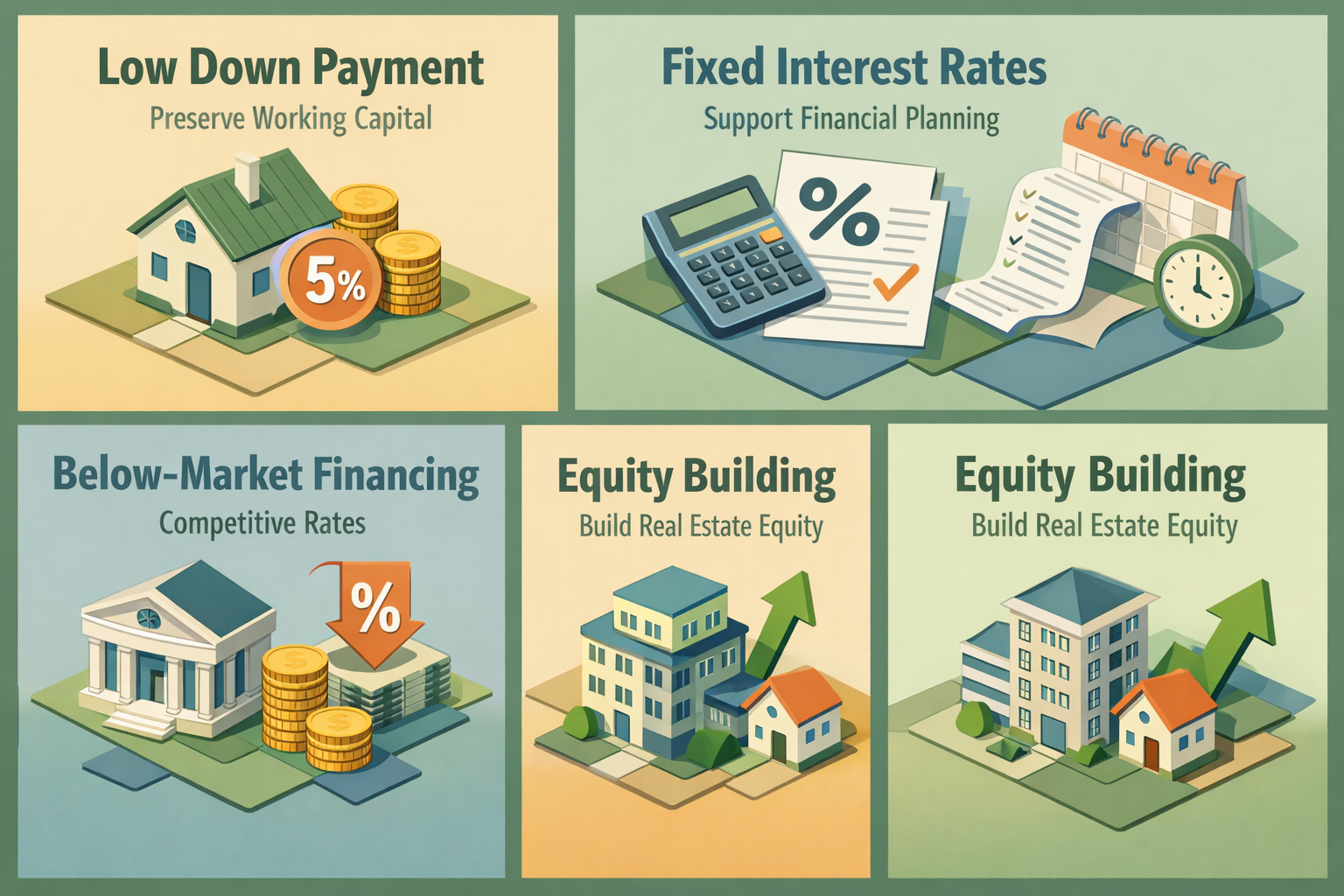

One of the most appealing aspects of the SBA 504 loan is its combination of low down payment requirements and long repayment terms. Many conventional commercial real estate loans require down payments of 20% to 30% or more. With the SBA 504 program, eligible borrowers may qualify with as little as 10% down in many cases, which can preserve valuable working capital for day-to-day business operations.

Repayment terms are another major advantage. SBA 504 loans are typically available with 10-year, 20-year, or 25-year terms depending on the asset being financed. Real estate projects often qualify for the longer terms, giving business owners more room to manage their monthly obligations without straining cash flow. The interest rates on the CDC portion of the loan are fixed and tied to U.S. Treasury rates, which may offer predictability in an otherwise volatile lending environment.

- Low down payment: Often as little as 10%, freeing up working capital for other business needs.

- Fixed interest rates: The CDC portion carries a fixed rate, supporting more accurate long-term financial planning.

- Long repayment terms: Up to 25 years for commercial real estate, reducing monthly payment pressure.

- Below-market financing: Rates on the CDC debenture portion are often competitive compared to conventional commercial loans.

- Equity building: Owning property rather than leasing can help businesses build real estate equity over time.

These benefits collectively make the SBA 504 loan a particularly strong fit for small business owners who want to stop paying rent and start building ownership in a commercial property.

Who Qualifies for an SBA 504 Loan?

Understanding eligibility requirements is an important first step before pursuing an SBA 504 loan. The SBA has established specific criteria that both the business and the project must meet. While lenders and CDCs may have their own additional requirements, the general SBA guidelines provide a useful framework for evaluating readiness.

To be eligible, a business must operate as a for-profit entity within the United States and meet the SBA's size standards, which typically means having a tangible net worth of less than $15 million and an average net income of less than $5 million after federal taxes for the two years prior to application. These thresholds can vary slightly depending on industry, so it's worth verifying the specific standards that apply to your sector.

Beyond size requirements, the business must demonstrate a genuine need for the financing, show that it can repay the loan from projected operating cash flow, and be owner-occupied — meaning the business must plan to occupy at least 51% of an existing building or 60% of a newly constructed property. Investment properties or buildings primarily leased to other tenants typically do not qualify under this program.

Borrowers should also be prepared to show solid creditworthiness. While the SBA 504 program is more accessible than many conventional loans, lenders and CDCs will still evaluate personal and business credit history, financial statements, and the viability of the project being financed. Good preparation and clean financial records can go a long way in strengthening an application.

Eligible Uses: What Can You Finance?

The SBA 504 loan is purpose-built for long-term fixed asset investment. That means not every business expense qualifies, but the eligible uses are substantial and meaningful for growth-oriented entrepreneurs. Understanding what the program covers helps small business owners plan their investment strategy accordingly.

Eligible uses for SBA 504 funds include the purchase of existing buildings intended for business use, the purchase of land and construction of new commercial facilities, renovation or modernization of existing buildings, and the acquisition of long-term machinery and equipment with a useful life of at least 10 years. These categories cover a wide range of commercial real estate and capital equipment scenarios.

What the program does not cover is equally important to understand. Borrowers cannot use SBA 504 funds for working capital, inventory, debt refinancing in most cases, or assets used primarily for investment or rental purposes. Attempting to use the loan outside these parameters could disqualify an application or result in compliance issues down the line.

For commercial real estate borrowers specifically, the 504 program can cover the full cost structure of a purchase — including land, building, and even soft costs like legal fees, appraisals, and environmental studies — as long as the overall project meets program guidelines. This makes it a comprehensive financing tool rather than a partial solution.

Comparing SBA 504 to Other Business Financing Options

It helps to understand how the SBA 504 loan stacks up against other popular financing options available to small business owners. Each product has its strengths, and the right choice often depends on the specific nature of the investment and the borrower's financial profile.

The SBA 7(a) loan is the SBA's most commonly used program and offers more flexibility in how funds can be used — including working capital, inventory, and debt refinancing. However, for commercial real estate or heavy equipment purchases, the 504 program often provides more favorable terms, particularly in regard to down payment requirements and the fixed-rate structure on the CDC portion. The 7(a) loan may also carry variable interest rates on a larger portion of the debt, which introduces more uncertainty for long-term planning.

Conventional commercial real estate loans from banks and credit unions can offer speed and simplicity, but they typically require higher down payments and may come with balloon payment structures or shorter amortization periods. For a small business owner trying to manage cash flow carefully, these features can create financial stress over time.

Equipment financing and asset-based lending are alternatives for businesses focused purely on machinery or technology acquisition, but they don't offer the same scope as the 504 program when real estate is also part of the equation. In many cases, entrepreneurs find that the SBA 504 loan is the most cost-efficient path when the goal is long-term commercial property ownership combined with major equipment investment.

The Application Process: What to Expect

Applying for an SBA 504 loan involves more steps than a standard bank loan, but the process is manageable when approached with the right preparation. The key parties involved — the private lender, the CDC, and the SBA — each play a distinct role, and understanding the flow helps borrowers set realistic expectations around timing and documentation.

The process typically begins with a conversation with a CDC in your region. CDCs are your main point of contact for the SBA-guaranteed portion of the loan, and they can help assess eligibility, outline required documentation, and guide you through the SBA's forms and approvals. At the same time, you'll need to identify and work with a participating private lender for the first mortgage portion of the financing.

Documentation requirements can be extensive. Borrowers should generally be prepared to provide business financial statements for the past two to three years, personal financial statements, federal tax returns, a business plan or project narrative, a purchase agreement or construction estimates, and environmental review documentation for real estate projects. The more organized and complete your financial records, the smoother the process tends to go.

Approval timelines can vary. Some borrowers may receive preliminary approvals within a few weeks, while more complex projects may take longer depending on the scope of the review and the responsiveness of all parties involved. Working with an experienced CDC and a lender familiar with SBA processes may help streamline the timeline. Once approved and funded, the investment can begin delivering long-term value to the business almost immediately.

●Conclusion

The SBA 504 loan represents one of the most powerful financing tools available to small business owners who are ready to invest in commercial real estate or major equipment. With low down payment requirements, long repayment terms, and fixed interest rates on the government-backed portion, this program is designed to make serious capital investment achievable — even for businesses that might struggle to qualify for conventional commercial financing. While the application process requires careful preparation and documentation, the long-term financial benefits can be well worth the effort. If you're a small business owner or entrepreneur looking to stop renting and start owning, or aiming to expand your operational capacity with significant equipment, exploring the SBA 504 program could be a smart next step. Connect with a qualified CDC or speak with a knowledgeable lender at LoanWise to find out if this program aligns with your growth goals.