For small business owners looking to purchase commercial real estate or invest in major equipment, finding the right financing can feel like a daunting challenge. Interest rates, down payment requirements, and loan terms all play a role in whether a deal makes financial sense. That's where the SBA 504 loan program steps in as a compelling option. Backed by the U.S. Small Business Administration, this program is specifically designed to help entrepreneurs and growing businesses access long-term, fixed-rate financing for major fixed assets. If you've been exploring ways to own your business space rather than lease it, the SBA 504 loan may be worth a closer look.

What Is the SBA 504 Loan Program?

The SBA 504 loan is a federally backed financing program created to support small business growth by making it easier to acquire significant long-term assets. Unlike a traditional bank loan, the 504 program involves a unique three-party structure that spreads the risk across multiple stakeholders — which is a key reason lenders are often more willing to approve these deals.

Here's how the structure typically works:

- A conventional lender (usually a bank or credit union) provides approximately 50% of the total project cost.

- A Certified Development Company (CDC) — a nonprofit organization certified by the SBA — covers roughly 40% of the project through an SBA-guaranteed debenture.

- The borrower contributes a down payment of approximately 10%, though this may be slightly higher for startups or special-use properties.

This structure means that a small business owner could potentially finance the purchase of a commercial building with as little as 10% down — a meaningful advantage over many conventional commercial loan requirements, which often demand 20% to 30% upfront. The SBA 504 loan is not a revolving line of credit or a short-term bridge product. It's a long-term financing solution meant to support sustainable business ownership and asset investment.

Eligible Uses: What Can You Finance With an SBA 504 Loan?

Understanding what the SBA 504 loan program can — and cannot — be used for is essential before applying. This program is purpose-built for fixed assets that promote business growth and job creation. Eligible uses may include:

- Purchasing owner-occupied commercial real estate

- Constructing a new facility or making significant renovations to an existing one

- Acquiring major long-term equipment or machinery with a useful life of at least 10 years

- Financing land purchases connected to a business facility

It's important to note that the SBA 504 loan is not intended for working capital, inventory purchases, debt refinancing in most cases, or investment properties where the borrower does not occupy the space. Owner-occupancy is a core requirement — the business must typically occupy at least 51% of an existing building or 60% of a newly constructed property.

This distinction matters greatly for commercial real estate investors. If your goal is to purchase a rental property or a building you won't operate from, the SBA 504 loan likely won't be the right fit. But for entrepreneurs ready to put down roots and own their operational space, it could offer significant financial advantages over time.

Rate Structures and Loan Terms That Favor Long-Term Planning

One of the most appealing features of the SBA 504 loan is the fixed interest rate on the CDC portion of the financing. Because this portion is tied to U.S. Treasury bond rates and sold as debentures on the bond market, borrowers typically benefit from rates that are competitive with — and sometimes lower than — conventional commercial loan rates.

The fixed-rate nature of the CDC portion provides predictability, which is a valuable asset for small business financial planning. Knowing your loan payment won't fluctuate with market conditions can make it significantly easier to budget for growth over a 10- or 25-year term. The conventional lender's portion may carry a variable or fixed rate depending on the institution, so it's worth asking your lender about their specific terms.

Loan terms typically available through the SBA 504 program include:

- 10-year terms — commonly used for equipment financing

- 20-year and 25-year terms — commonly used for commercial real estate

Longer repayment terms generally mean lower monthly payments, which helps preserve cash flow — a critical concern for most small business owners. While the total interest paid over a longer term may be higher, many entrepreneurs find the improved monthly cash position well worth the trade-off, especially during growth phases.

Who Qualifies: Key Eligibility Requirements for Small Business Borrowers

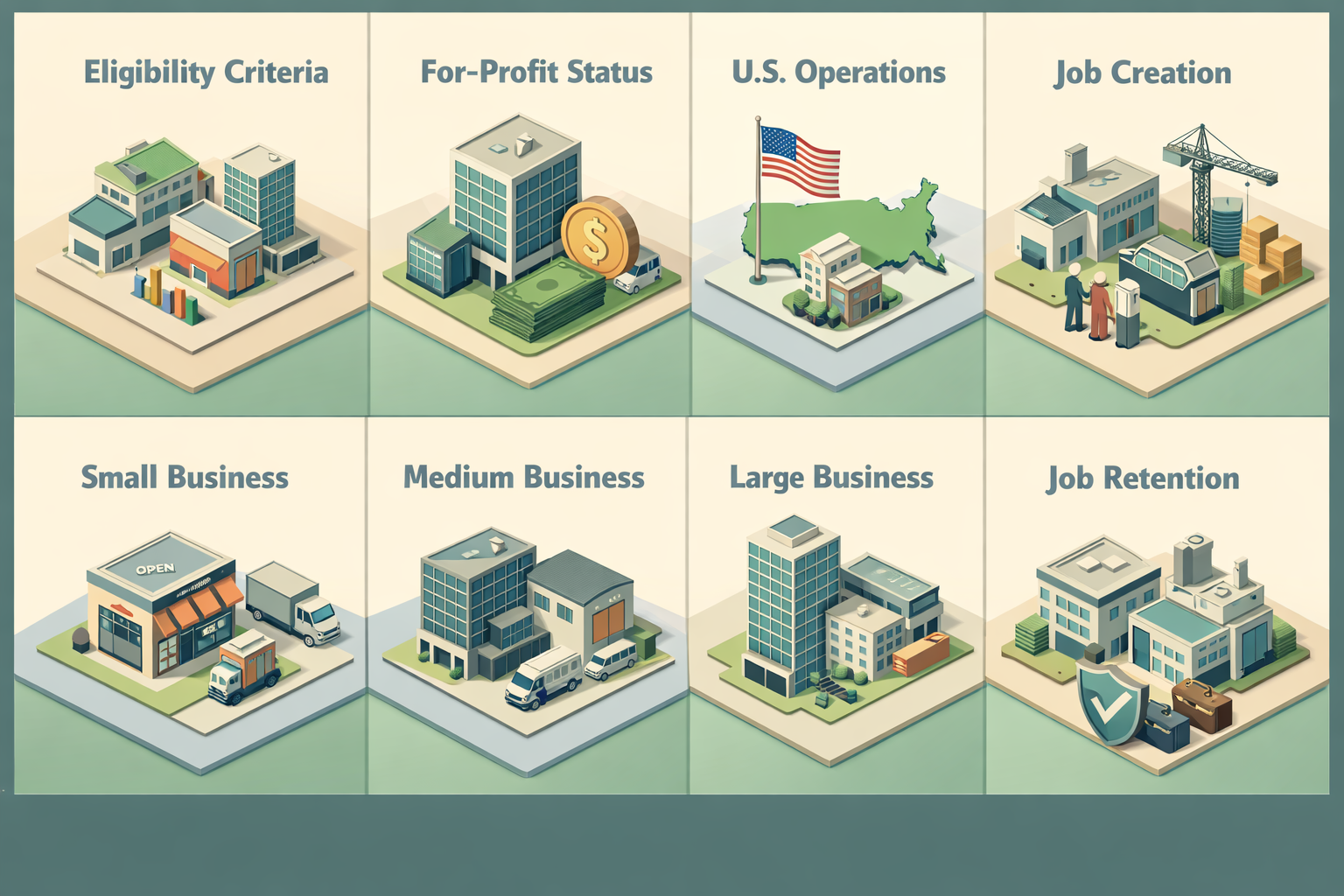

The SBA 504 loan is designed specifically for small businesses, and eligibility is determined by a combination of size standards, financial health, and operational criteria. While specific qualification thresholds can vary based on the lender and the CDC involved, general eligibility requirements typically include:

- Business size: The business must qualify as a "small business" under SBA standards, which often means a tangible net worth of less than $15 million and average net income of less than $5 million after taxes for the prior two years.

- For-profit status: The program is available to for-profit businesses only.

- U.S. operations: The business must operate in the United States.

- Job creation or community development: Projects are often expected to create or retain jobs, or meet other public policy goals such as minority business development or rural economic growth.

Beyond these baseline criteria, lenders and CDCs will also evaluate your personal and business credit history, existing debt obligations, cash flow, and management experience. A strong credit profile and documented business revenue will generally improve your chances of approval, though some CDCs may work with businesses that have less-than-perfect credit histories, particularly when the project demonstrates strong economic impact.

Entrepreneurs should be aware that the approval process for SBA 504 loans can take longer than a conventional loan — sometimes several weeks to a few months — due to the involvement of both a lender and a CDC. Planning ahead and working with an experienced lending professional can help streamline the process.

Costs and Fees to Factor Into Your Budget

While the SBA 504 loan offers many advantages, small business owners should also account for associated fees and closing costs as part of their total project budget. Like most government-backed loan programs, the 504 program does involve certain fees that help fund the SBA's operating costs and guarantee structure.

Fees that borrowers may encounter include:

- SBA guarantee fees — typically a percentage of the loan amount, which may be financed into the loan itself

- CDC processing fees — charged by the Certified Development Company for structuring and managing the SBA portion

- Attorney and closing fees — standard costs associated with commercial real estate transactions

- Third-party fees — such as appraisals, environmental reports, and title insurance

While these costs add up, it's worth noting that many of the SBA-related fees can be rolled into the loan rather than paid out of pocket at closing. This can be a meaningful benefit for business owners who want to preserve working capital. Even so, getting a detailed fee estimate from your CDC and lender early in the process is a smart step to avoid surprises.

Comparing the SBA 504 Loan to Other Business Financing Options

Understanding how the SBA 504 loan stacks up against other financing tools can help you make a more informed decision. Here's a brief look at how it compares to a few common alternatives:

- SBA 7(a) Loan: The SBA 7(a) is more flexible — it can be used for working capital, debt refinancing, and real estate — but it may carry higher interest rates and smaller loan amounts for real estate projects. The 504 is generally preferred when the primary goal is a large real estate or equipment purchase.

- Conventional Commercial Mortgage: Traditional commercial loans often require larger down payments (20%–30%) and may come with shorter amortization periods. The SBA 504's lower down payment requirement and longer terms can provide meaningful cash flow advantages.

- USDA Business Programs: In rural areas, USDA business loan programs may offer competitive alternatives, though availability and eligibility criteria can differ significantly from the SBA 504.

- Equipment Financing: For equipment-only purchases, standalone equipment loans or leases may offer a faster path to approval. However, the SBA 504 may offer better long-term rates for larger equipment investments.

The right choice depends on your specific goals, timeline, and financial profile. Consulting with a lending professional familiar with both SBA programs and conventional commercial financing can help you identify the most cost-effective path for your situation.

●Conclusion

The SBA 504 loan represents a meaningful opportunity for small business owners and entrepreneurs who are ready to invest in their own commercial space or major equipment. With its lower down payment requirements, competitive fixed rates on the CDC portion, and long repayment terms, it's designed to support sustainable business growth without overwhelming your monthly cash flow. That said, it's not a one-size-fits-all solution — eligibility requirements, owner-occupancy rules, and the multi-party structure mean it works best for businesses with a clear long-term vision for their physical operations. If you're exploring commercial real estate financing or looking to take your business to the next level, speaking with a knowledgeable lending advisor could help you determine whether the SBA 504 loan aligns with your goals. At LoanWise, we're here to help you navigate your options with clarity and confidence.