Divorce can turn a straightforward mortgage application into a complicated financial puzzle. If you're trying to secure a new home loan — or refinance an existing one — while your former spouse is still listed on the property title, lenders will want a clear picture of how that relationship affects your finances. Understanding the requirements to get a conventional loan with divorced spouse on title is essential for homebuyers, homeowners, and real estate investors who want to move forward without unnecessary delays or denials. This guide breaks down what conventional lenders typically look for in these situations and how you can put your best foot forward.

What It Means When a Divorced Spouse Remains on Title

When a couple divorces, the legal process of separating property doesn't always move as quickly as the divorce decree itself. In many cases, a former spouse may still appear on the property's title — even if they no longer live in the home or contribute to the mortgage payments. This situation creates a layer of complexity that conventional lenders must carefully evaluate before approving a new loan.

Being on title means having a legal ownership interest in the property. This is different from being on the mortgage, though the two often overlap. A divorced spouse could be on title without being on the loan, or they could appear on both. From a lender's perspective, title status affects who has a claim to the property, which directly influences the security of the loan being underwritten.

It's important to understand that conventional loans — those backed by Fannie Mae or Freddie Mac guidelines — have specific rules about how ownership and liability are documented and verified. Lenders will typically request a copy of your divorce decree, any property settlement agreements, and quitclaim deed documentation to understand the current ownership structure before proceeding.

Core Eligibility Standards for Conventional Loan Applicants

Before addressing the specifics of a divorced co-owner situation, it helps to understand what conventional lenders require of borrowers in general. These baseline standards form the foundation of any approval decision, regardless of marital or title complications.

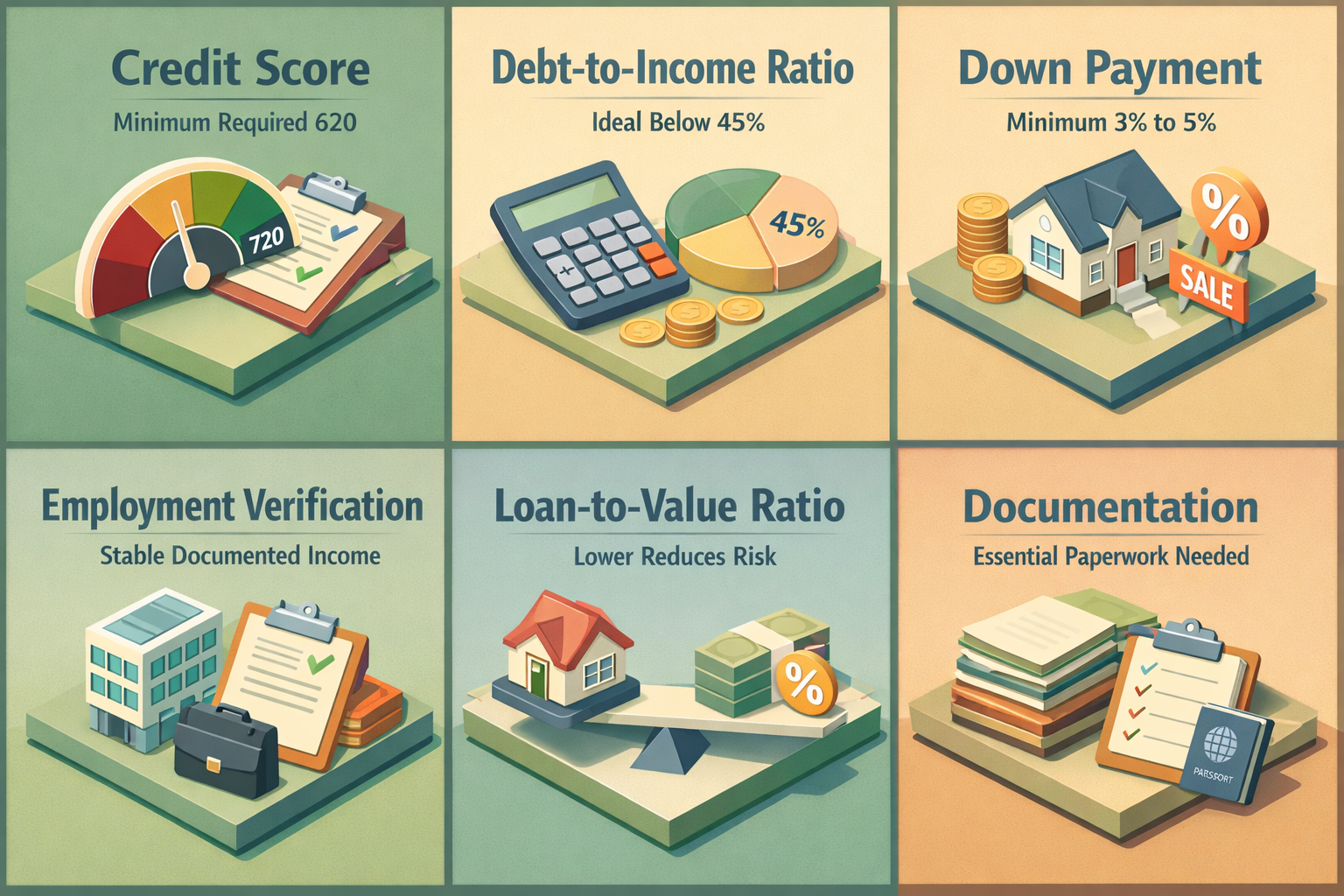

- Credit Score: Most conventional loan programs typically require a minimum credit score of 620, though a higher score — generally 740 or above — may help you qualify for better interest rates and terms.

- Debt-to-Income Ratio (DTI): Lenders usually look for a DTI ratio at or below 45%, though some programs may allow slightly higher ratios with compensating factors. Your DTI measures how much of your gross monthly income goes toward recurring debt payments.

- Down Payment: Conventional loans generally require a minimum down payment of 3% to 5% for primary residences, with higher requirements for investment properties or second homes.

- Employment and Income Verification: Stable, documentable income is critical. Lenders will review pay stubs, W-2s, tax returns, and bank statements to confirm your ability to repay.

- Loan-to-Value Ratio (LTV): This ratio compares your loan amount to the home's appraised value. A lower LTV may reduce your risk profile and could eliminate the need for private mortgage insurance (PMI).

Meeting these benchmarks is a prerequisite, but when a divorced spouse remains involved in the title or prior mortgage, additional documentation and underwriting steps are typically required.

How a Divorced Spouse on Title Affects Your Loan Application

One of the most common challenges borrowers face when meeting the requirements to get a conventional loan with divorced spouse on title is how lenders treat the financial obligations connected to that former partner. Even if your divorce was finalized years ago, the lender's underwriting team will likely consider several key factors.

Existing Mortgage Liability

If your ex-spouse is still listed on the original mortgage for the property in question — or on any other property — their debt may affect your application. Fannie Mae guidelines generally allow lenders to exclude a co-borrower's mortgage debt from your DTI calculation if you can document that the other party has been making payments independently for at least 12 months. You'll typically need to provide 12 months of canceled checks, bank statements, or similar evidence to support this exclusion.

Divorce Decree and Property Settlement Agreements

Your divorce decree is one of the most important documents in this scenario. Lenders will review it to confirm what obligations each party has assumed, who is responsible for the existing mortgage, and whether any court orders govern the property. A clear, legally binding settlement agreement can help streamline the underwriting process considerably.

Quitclaim Deed Considerations

If your divorced spouse has signed a quitclaim deed relinquishing their ownership interest, lenders may treat the title situation more favorably. However, a quitclaim deed does not remove someone from the mortgage — only a refinance or formal assumption can accomplish that. Lenders will distinguish between these two scenarios carefully.

Conventional Loan Requirements With an Existing Co-Borrower After Divorce

Understanding the conventional loan requirements with existing co-borrower dynamics is especially important when divorce is involved. In some cases, the divorced spouse may still technically function as a co-borrower on an active loan connected to the property. This creates a unique set of underwriting considerations.

When a co-borrower relationship persists after divorce, the lender will typically evaluate both parties' credit profiles, income, and liabilities — even if only one person is applying for the new loan. This is because the co-borrower's financial health can still influence the risk level of the existing lien or the new financing being requested.

Removing a Co-Borrower Through Refinancing

One of the most effective ways to resolve a lingering co-borrower issue is through a refinance. If you refinance the existing mortgage solely in your name, your former spouse is legally removed from the loan obligation. This approach requires that you meet all conventional loan qualification standards independently, including income, credit, and DTI thresholds. It's often the cleanest solution from both a legal and financial standpoint.

Adding Context With a Letter of Explanation

Underwriters may ask for a letter of explanation (LOE) describing the circumstances of the divorce and the current ownership arrangement. Being transparent and providing thorough documentation — including the divorce decree, any court orders, and updated title records — can help prevent delays and build confidence with the lender.

Documentation You'll Likely Need to Gather

Being well-prepared with the right paperwork can make the difference between a smooth approval and a frustrating back-and-forth with your lender. When navigating a conventional loan application that involves a divorced spouse on title, you may need to provide some or all of the following:

- Final Divorce Decree: This legally binding document outlines asset division, debt assignments, and any court orders related to the property.

- Property Settlement Agreement: A detailed breakdown of what each party is responsible for post-divorce, especially regarding real estate and mortgage obligations.

- Quitclaim Deed (if applicable): Evidence that your ex-spouse has formally relinquished their ownership interest in the property.

- 12 Months of Payment History: If you're trying to exclude your former spouse's mortgage debt from your DTI, you'll need documented proof that they've been making those payments independently.

- Updated Title Report: A current title search to confirm who is legally listed as an owner and whether any liens or encumbrances exist.

- Letter of Explanation: A clear, concise narrative explaining the ownership situation and how it has been legally resolved or managed.

Gathering these documents early in the process can significantly speed up your application timeline and reduce the chance of last-minute surprises during underwriting.

Strategies to Strengthen Your Application in Complex Title Situations

When your title situation is complicated by a prior marriage, it pays to be proactive. There are several strategies that may help improve your approval odds and present a stronger application to conventional lenders.

Work With an Experienced Mortgage Professional

Not all loan officers have the same level of experience with post-divorce lending scenarios. Seeking out a lender or mortgage broker who is familiar with Fannie Mae and Freddie Mac guidelines — particularly around co-borrower liability and title complications — can be a significant advantage. They can help you identify potential issues before you apply and guide you toward the most suitable loan product.

Improve Your Individual Credit Profile

Since your divorced spouse may no longer be part of the loan application, your personal credit score carries more weight than ever. Paying down revolving balances, resolving any collections or derogatory marks, and avoiding new credit inquiries in the months before applying could meaningfully improve your eligibility and the interest rate you're offered.

Consider a Title Update Before Applying

If your ex-spouse is willing to cooperate, working with a real estate attorney to update the title — through a quitclaim deed or other legal instrument — before you apply for the new loan may simplify the underwriting process. Lenders generally prefer clean title situations, and resolving ownership ambiguity upfront can prevent delays.

Maintain Clear Financial Boundaries

Commingled finances or shared accounts with your former spouse can raise red flags during underwriting. Demonstrating that your income, savings, and debts are clearly separated and independently managed may help the lender feel more confident in your application.

●Conclusion

Navigating the requirements to get a conventional loan with divorced spouse on title is genuinely challenging, but it's far from impossible. With the right documentation, a clear understanding of conventional loan guidelines, and a knowledgeable lending partner by your side, you can move through the process with confidence. Whether you're buying a new home, refinancing an existing mortgage, or simply trying to establish clean financial independence after a divorce, taking the time to understand how lenders evaluate your situation puts you in a much stronger position. At LoanWise, we're here to help you make sense of complex lending scenarios and find a path forward that works for your unique circumstances. Connect with one of our mortgage specialists today to get started.