Earthquakes can cause serious damage to residential properties — from cracked foundations to compromised load-bearing walls. If you're a homebuyer, homeowner, or real estate investor dealing with a structurally damaged property, you might be wondering whether financing is even possible. The good news is that figuring out how to get a mortgage for a house with structural damage after earthquake is a challenge many borrowers have successfully navigated. While it requires extra steps and careful preparation, several loan programs and lender strategies may open the door to financing — even for homes that need significant repairs.

Why Structural Earthquake Damage Complicates the Mortgage Process

When a home sustains structural damage from an earthquake, lenders become cautious — and for good reason. A mortgage is a secured loan, meaning the property itself serves as collateral. If that collateral is compromised, lenders face greater risk if the borrower defaults and the home can't be sold at full market value.

Lenders typically require a property appraisal before approving any home loan. An appraiser will assess the property's current condition and compare it to similar homes in the area. If structural damage is present — such as a cracked foundation, shifted framing, or damaged load-bearing walls — the appraiser may flag the home as ineligible for standard financing until repairs are completed.

Additionally, most conventional loans backed by Fannie Mae or Freddie Mac follow strict property condition guidelines. Homes with health and safety hazards, including severe structural issues, are often deemed ineligible unless those conditions are resolved prior to closing. This doesn't mean all hope is lost, but it does mean borrowers need to explore the right loan products from the start.

Getting a Professional Structural Assessment First

Before approaching any lender, one of the most important steps is getting a licensed structural engineer or certified home inspector to evaluate the property. This assessment serves multiple purposes. First, it gives you a clear picture of the scope of damage. Second, it documents the condition of the home in writing — something lenders and appraisers will likely require as part of their review.

A structural report can also help you estimate repair costs, which is critical if you're exploring renovation loan options. Lenders offering rehabilitation mortgages typically want to see a detailed scope of work and cost estimate before approving funds for repairs. Having this documentation ready early in the process may speed up your approval timeline significantly.

It's also worth noting that some earthquake-affected areas may have local government programs or disaster relief assessments already in place. Checking with your local building or planning department could reveal additional resources and documentation that support your loan application.

Earthquake-Damaged Home Mortgage Options Worth Exploring

When it comes to earthquake-damaged home mortgage options, borrowers often have more pathways than they expect. The key is matching the right loan program to the property's current condition and the borrower's financial profile. Here are some programs that may be relevant:

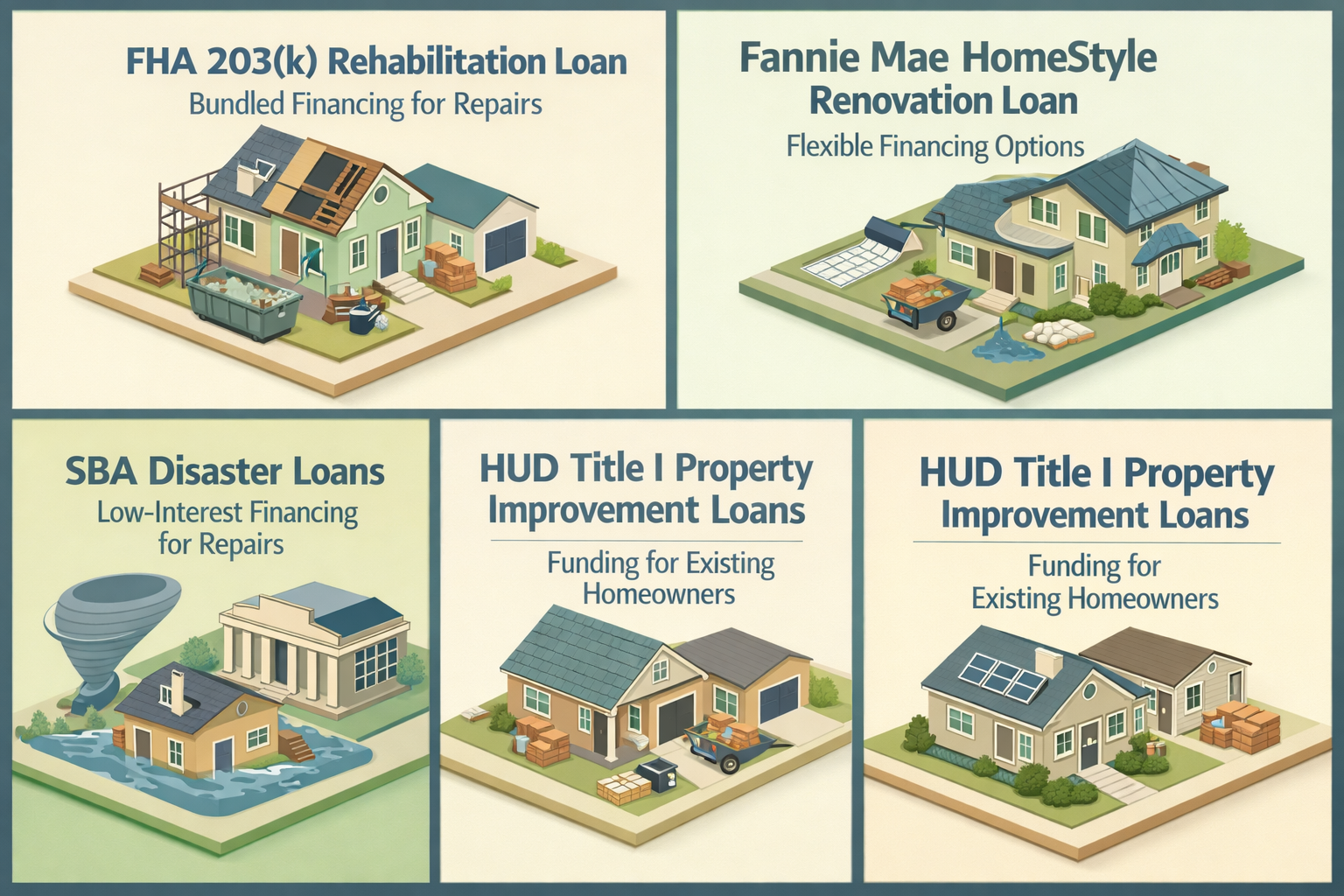

- FHA 203(k) Rehabilitation Loan: This is one of the most commonly used programs for financing homes that need significant repairs. The FHA 203(k) loan bundles the purchase price and estimated renovation costs into a single mortgage. There are two versions — the Standard 203(k) for major structural repairs and the Limited 203(k) for smaller projects. For earthquake damage, the Standard version is likely more appropriate, as it covers structural work.

- Fannie Mae HomeStyle Renovation Loan: This conventional renovation loan works similarly to the 203(k) but may offer more flexibility in terms of eligible properties and borrower qualifications. It allows buyers to finance the cost of repairs into the mortgage, with funds held in escrow and released as work is completed.

- Freddie Mac CHOICERenovation Loan: Another conventional option, the CHOICERenovation loan is designed specifically to help borrowers finance homes that need significant improvements, including disaster-related repairs. It may be particularly relevant for earthquake-affected properties.

- SBA Disaster Loans: While not a traditional mortgage product, the U.S. Small Business Administration offers low-interest disaster loans to homeowners and renters in federally declared disaster areas. These loans can be used to repair or replace damaged property and may complement other financing options.

- HUD Title I Property Improvement Loans: For homeowners who already own the damaged property, HUD-approved lenders may offer Title I loans to fund repairs without requiring a full refinance.

Each of these options carries its own eligibility requirements, loan limits, and approval timelines. Speaking with a knowledgeable mortgage advisor is the best way to determine which path fits your specific situation.

How Lenders Evaluate Risk on Earthquake-Affected Properties

Understanding how lenders think about risk can help you prepare a stronger application. When a lender reviews a mortgage request for a structurally damaged home, they're evaluating several factors beyond your credit score and income.

Property value and collateral integrity are at the top of the list. If the appraised value of the home — in its current damaged state — is significantly lower than the purchase price or loan amount, the lender may decline the loan or require a larger down payment to offset the risk. Renovation loans address this by using the after-repair value (ARV) of the home rather than its current damaged condition, which can make qualification easier.

Title and insurance considerations also come into play. Lenders will want to confirm that the property can be insured. In earthquake-prone regions, standard homeowners insurance may not cover seismic damage — separate earthquake insurance is typically required. Some lenders may make earthquake insurance a condition of loan approval, especially in high-risk zones.

Contractor qualifications and repair timelines matter for renovation loans. Lenders offering 203(k) or HomeStyle loans typically require that repairs be completed by licensed contractors within a set timeframe — often six to twelve months from closing. Delays or contractor issues can create complications, so vetting your repair team carefully before applying is a smart move.

Steps to Strengthen Your Mortgage Application for a Damaged Property

Knowing how to get a mortgage for a house with structural damage after earthquake isn't just about choosing the right loan program — it's also about presenting yourself as a qualified, prepared borrower. Here are some practical steps that may improve your chances of approval:

- Check your credit profile early. Lenders for renovation loans often have minimum credit score requirements. Reviewing your credit report in advance and addressing any errors or outstanding issues may put you in a better position.

- Build a strong down payment. A larger down payment reduces the lender's exposure and may make them more willing to work with a non-standard property. Some renovation loan programs require as little as 3.5% down (FHA 203k), but contributing more can strengthen your offer.

- Get multiple contractor bids. Renovation lenders want realistic cost estimates. Having two or three contractor bids ready demonstrates due diligence and helps ensure the loan amount accurately covers the repair scope.

- Work with a HUD-approved consultant. For Standard FHA 203(k) loans, a HUD-approved 203(k) consultant is typically required to help develop the scope of work and oversee the repair process. Engaging one early can streamline your application.

- Document everything. Lenders and appraisers will want records of the damage, repair estimates, inspection reports, and any communications with local authorities. Keeping organized documentation from day one may prevent delays.

Refinancing a Home You Already Own After Earthquake Damage

If you're an existing homeowner whose property was damaged by an earthquake, refinancing a home may be a viable path to access funds for repairs. However, the process comes with its own set of challenges. Most standard rate-and-term refinances require the home to be in acceptable condition for the lender's appraiser. If severe structural damage is present, a traditional refinance may be declined until repairs are made — which creates a frustrating catch-22.

One possible solution is a cash-out renovation refinance, which works similarly to purchase renovation loans by incorporating the cost of repairs into the new loan balance. Programs like the FHA 203(k) refinance or the Fannie Mae HomeStyle refinance may allow eligible homeowners to roll repair costs into a new mortgage based on the home's projected after-repair value.

Additionally, if you live in a federally declared disaster area, you may qualify for SBA Home Disaster Loans regardless of whether you have a business. These loans can provide up to a certain amount in low-interest financing to repair your primary residence. Checking FEMA's disaster declaration list for your county is a worthwhile first step.

Homeowners with existing equity might also consider a Home Equity Line of Credit (HELOC), though many lenders may be hesitant to approve one on a property with active structural damage. A HELOC could be more accessible once initial stabilization work has been completed and the home's value is more clearly established.

Working with the Right Lender Makes All the Difference

Not every lender is equipped — or willing — to handle mortgage applications for earthquake-damaged properties. Finding the right lending partner is arguably the most important step in the entire process. Look for lenders with demonstrated experience in renovation lending, FHA 203(k) programs, or disaster recovery financing. These lenders understand the nuances of appraisal conditions, escrow holdbacks, and contractor oversight that standard purchase loans don't require.

Mortgage brokers can be especially valuable in this situation because they have access to multiple lenders and can match your specific scenario to the most appropriate loan product. A broker familiar with specialty lending for distressed or damaged properties may be able to identify options that a single-bank lender might not offer.

It's also worth asking potential lenders directly about their experience with earthquake-affected homes. Ask how many renovation loans they've closed, how they handle appraisal disputes, and what their average timeline looks like from application to funding. These questions can reveal a great deal about whether a lender is the right fit for your situation.

Finally, if you're purchasing a damaged property as a real estate investor, be aware that some renovation loan programs are limited to owner-occupied homes. Investors may need to explore alternative financing such as hard money loans or private bridge loans, which tend to carry higher interest rates but offer more flexibility on property condition.

●Conclusion

Navigating the world of home financing after an earthquake is undeniably more complex than a standard mortgage transaction — but it's far from impossible. From FHA 203(k) loans to disaster relief programs and specialty refinance options, there are genuine pathways available for homebuyers, homeowners, and investors willing to do their homework. The key is starting with a solid structural assessment, understanding the loan programs best suited to your situation, and working with a lender who has real experience in this space. If you're ready to explore your options, LoanWise is here to help you find the right financing solution for your unique circumstances.