For many veterans and active-duty service members, homeownership is a deeply meaningful goal — and the VA loan program exists to help make it more achievable. But what happens when the home you want is a manufactured home sitting on land you don't own? This is where things can get a bit more complicated. Understanding the requirements for a VA loan for manufactured homes on leased land is essential before you start the application process. While the VA does allow financing for manufactured homes, the leased land component introduces a specific set of conditions that both borrowers and lenders must carefully review. This guide breaks down what you need to know so you can move forward with confidence.

What the VA Loan Program Says About Manufactured Homes

The U.S. Department of Veterans Affairs does permit veterans to use their VA loan benefit to purchase manufactured homes — but not without conditions. The VA distinguishes between manufactured homes, modular homes, and site-built homes, and each category carries its own set of guidelines.

A manufactured home, under VA guidelines, is a structure built to the federal HUD (Department of Housing and Urban Development) code and constructed in a factory before being transported to its final location. For a manufactured home to qualify under the VA loan program, it typically must meet the following baseline standards:

- It must have been built on or after June 15, 1976, which is when federal HUD construction standards took effect.

- It must be classified as real property, not personal property — though this standard becomes more complex when land is leased rather than owned.

- It must be on a permanent foundation that meets VA and HUD requirements.

- It must be the borrower's primary residence.

These foundational requirements apply broadly, but the leased land situation adds another layer of review that veterans should be fully prepared for.

How Leased Land Changes the VA Loan Equation

When a manufactured home sits on land that the borrower does not own — such as in a land-lease community or a mobile home park — the VA loan process becomes notably more restrictive. Most VA lenders prefer or require that the borrower own the land on which the manufactured home sits, because it simplifies the collateral position and reduces risk.

That said, the VA does not automatically prohibit financing for manufactured homes on leased land. Instead, it establishes specific conditions that the lease arrangement must meet. Here's what lenders and the VA will generally look for:

- Minimum lease term: The lease on the land must typically extend for a meaningful period beyond the loan term. Many lenders require that the remaining lease term be at least as long as the loan itself, or extend a set number of years past the loan's maturity date.

- Lease renewal provisions: The lease should include language that allows for renewal, giving the borrower reasonable assurance of continued occupancy.

- Protections against eviction: The lease agreement should offer adequate tenant protections, preventing arbitrary or sudden termination that could leave the borrower without a place for their home.

- Lender approval of lease terms: The specific lender participating in the VA loan program will review the lease document directly. Not all lenders have the same appetite for this type of transaction, so shopping around may be necessary.

It's worth noting that because VA loans are backed by the federal government but originated by private lenders, individual lender overlays — meaning additional requirements beyond VA minimums — can significantly affect what's possible in a leased land scenario.

Borrower Eligibility: Who Qualifies for This Type of VA Financing

Before anything else, the borrower must qualify for a VA loan. Meeting the VA's service eligibility requirements is the first and non-negotiable step. Eligible borrowers typically include:

- Veterans who have served the minimum required active duty period

- Active-duty service members currently serving

- Surviving spouses of veterans who died in service or from a service-connected disability, in some cases

- Members of the National Guard or Reserves who meet specific service criteria

To confirm eligibility, borrowers must obtain a Certificate of Eligibility (COE) from the VA. This document verifies to the lender that the borrower has earned the VA loan benefit.

Beyond service eligibility, borrowers must also meet the lender's financial qualification standards, which typically include:

- Credit score: The VA does not set a hard minimum credit score, but most lenders require at least a 620. Some may require higher scores for manufactured home loans on leased land given the added complexity.

- Debt-to-income ratio (DTI): Lenders generally prefer a DTI at or below 41%, though exceptions can sometimes be made with compensating factors.

- Residual income: The VA's residual income requirement — meaning the money left over after paying major monthly expenses — is a key qualifying factor and varies by region and family size.

- Stable income and employment: Lenders will want to see consistent income history, typically at least two years of stable employment or verifiable income.

Property Standards and Permanent Foundation Rules

Even when leased land is involved, the manufactured home itself must meet strict property standards to be approved for VA financing. The VA appraisal process will evaluate the home against VA Minimum Property Requirements (MPRs), which are designed to ensure the home is safe, structurally sound, and sanitary.

Key property-related requirements that lenders and VA appraisers will assess include:

- Permanent foundation: The home must be affixed to a permanent foundation that meets HUD guidelines. Homes still on wheels, axles, or temporary blocking are generally not eligible.

- HUD certification label: Each section of the manufactured home should display a HUD certification label (sometimes called a HUD tag), confirming it was built to federal standards.

- Data plate: Inside the home, there should be a HUD data plate showing the home's construction specifications, including wind and thermal zones.

- Utilities and systems: The home's electrical, plumbing, heating, and cooling systems must be functional and meet local code requirements.

- Roof and structure: The roof and overall structure must be in acceptable condition with no significant water damage, structural defects, or safety hazards.

Because the VA appraisal for manufactured homes can be more detailed than a standard home appraisal, it's wise to have the property inspected independently before formally applying. Addressing issues early can prevent delays or loan denials later in the process.

Understanding the Requirements for a VA Loan for Manufactured Homes on Leased Land

To bring it all together, the requirements for a VA loan for manufactured homes on leased land can be grouped into three categories: borrower eligibility, property standards, and lease conditions. All three must be satisfied simultaneously for approval to be possible.

Here's a consolidated overview of what veterans should prepare:

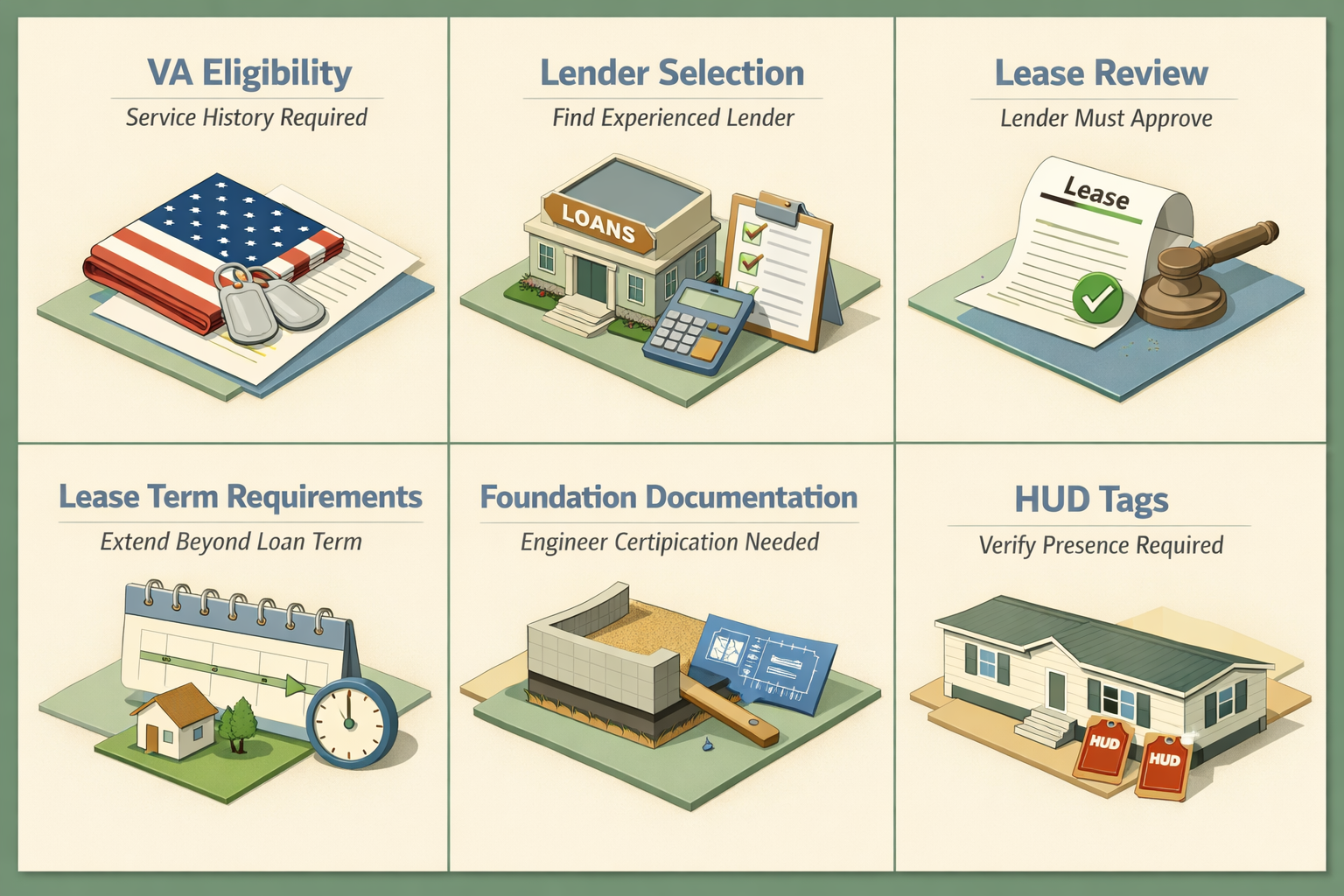

- VA eligibility: A valid Certificate of Eligibility is required. Confirm your service history meets VA thresholds.

- Lender selection: Not every VA-approved lender will finance manufactured homes on leased land. Finding a lender experienced in this niche is critical.

- Lease review: The ground lease must be reviewed and approved by the lender. Bring a copy of the full lease agreement early in the process.

- Lease term requirements: Many lenders require the lease to extend well beyond the loan term. A 30-year loan may require a lease with at least 30 years remaining — or more.

- Permanent foundation documentation: An engineer's certification or foundation inspection report may be required to confirm the home is properly anchored.

- HUD tags and data plate: These must be present and verifiable. If tags are missing, there's a process to apply for a label verification letter, though this adds time.

- VA appraisal: A VA-approved appraiser familiar with manufactured homes must conduct the appraisal. Not all appraisers specialize in this property type.

Because this combination of factors creates a more complex transaction than a standard home purchase, patience and thorough preparation are especially valuable here.

Common Challenges Veterans Face — and How to Address Them

Veterans pursuing VA loan manufactured home leased land financing often encounter a handful of recurring hurdles. Being aware of these ahead of time can save significant time and frustration.

Limited Lender Availability

Because this loan type carries more complexity and risk, many VA-approved lenders simply won't offer it. Some may offer manufactured home loans only when the borrower also owns the land. To work around this, veterans may need to contact multiple lenders or work with a mortgage broker who specializes in VA and manufactured home financing.

Lease Terms That Don't Meet Requirements

Many land-lease communities have standard lease agreements that weren't designed with VA lending in mind. A lease that's renewable on a year-to-year basis, for example, is unlikely to satisfy lender requirements for a long-term mortgage. Before falling in love with a property, review the lease carefully with a lender or housing counselor.

Missing HUD Documentation

Older manufactured homes may be missing their HUD certification labels due to age, renovations, or prior moves. In these cases, borrowers may need to contact the Institute for Building Technology and Safety (IBTS) to request a label verification letter. This process takes time, so it's best to initiate it early.

Appraisal Complexity

VA appraisals for manufactured homes on leased land can be challenging to complete because there may be fewer comparable sales in the area. Lenders and appraisers will typically look for similar manufactured home sales within a reasonable geographic radius, but data can be limited in rural or less-populated markets.

Steps to Start the Process the Right Way

If you're a veteran interested in purchasing a manufactured home on leased land using your VA benefit, a structured approach can make the process smoother. Here are recommended steps to take:

- Obtain your Certificate of Eligibility: You can request this through the VA's eBenefits portal, through your lender, or directly from the VA. This is your starting point.

- Review your credit and finances: Pull your credit reports, check your debt-to-income ratio, and calculate your residual income to get a realistic sense of where you stand financially.

- Find a VA-approved lender experienced in manufactured homes: Ask specifically whether the lender finances manufactured homes on leased land before spending time on an application.

- Gather lease documentation: Obtain the full lease agreement for the land and have your lender review it early to identify any issues.

- Research the home's HUD compliance: Verify that HUD tags are present and that the home was built after June 15, 1976.

- Get a foundation inspection: If documentation isn't available, commission an engineer's report confirming the home meets permanent foundation standards.

- Work with a VA-approved appraiser: Your lender will order the VA appraisal, but you can ask about the appraiser's experience with manufactured homes in leased land situations.

Taking these steps in order can help avoid surprises and keep the transaction moving forward efficiently.

●Conclusion

Navigating the requirements for a VA loan for manufactured homes on leased land takes preparation, the right lender, and a clear understanding of what the VA and private lenders expect. While the process is more involved than a typical home purchase, it's not out of reach for veterans who are organized and informed. The VA loan benefit is a powerful tool — and with the right guidance, it can help eligible service members and veterans achieve homeownership even in non-traditional housing situations. If you're ready to explore your options, connect with a VA-experienced mortgage professional at LoanWise who can walk you through the specific steps based on your unique situation.