Tapping into your home equity can be a smart financial move — whether you're funding renovations, consolidating debt, or investing in new opportunities. But what happens when your property isn't just a standard house on a single lot? For homeowners whose property includes multiple adjacent vacant lots, the path to a Home Equity Line of Credit (HELOC) can get a bit more complex. Lenders view these properties differently, and understanding the specific requirements for a HELOC on a property with multiple adjacent vacant lots could mean the difference between approval and denial. This guide walks you through what to expect, what lenders typically look for, and how to put your best foot forward.

What Is a HELOC and How Does It Work for Homeowners?

A Home Equity Line of Credit, or HELOC, is a revolving credit line secured by the equity in your home. Think of it like a credit card, but backed by the value of your property. During the draw period — which typically lasts five to ten years — you can borrow, repay, and borrow again up to your approved credit limit. After that, the repayment period begins, and you pay back what you owe, usually over another ten to twenty years.

HELOCs are popular among homeowners because they often come with lower interest rates than personal loans or credit cards, and the interest may be tax-deductible in certain situations. However, since the loan is secured by your home, failing to repay puts your property at risk.

For most standard properties, the HELOC process is fairly straightforward. But when your home sits alongside vacant land parcels, lenders may need to take a closer look before approving your application.

Why Adjacent Vacant Lots Complicate the HELOC Process

Lenders use your property's appraised value as the foundation for calculating how much equity you have — and therefore how much you can borrow. When multiple vacant lots sit adjacent to your primary residence, several complications can arise that affect this valuation and the lender's willingness to extend credit.

First, there's the question of how the lots are titled. Are they on a single parcel with your home, or are they separate legal parcels? If they're separate parcels, many lenders may not include their value in the HELOC collateral at all. This could significantly reduce the equity available to you.

Second, vacant land is generally considered a higher-risk asset class than improved residential property. Lenders may worry about the marketability of raw land if they ever need to foreclose and sell the property to recover their funds.

Third, zoning and land use classifications matter. Lots zoned for residential development may be treated differently than agricultural or commercial parcels. Lenders want to understand exactly what they're securing their loan against.

Understanding these factors upfront can help you set realistic expectations and prepare the right documentation before applying.

Core Requirements for a HELOC on a Property with Multiple Adjacent Vacant Lots

Meeting the requirements for a HELOC on a property with multiple adjacent vacant lots typically involves satisfying a broader set of conditions than a standard HELOC application. Here's what lenders often look for:

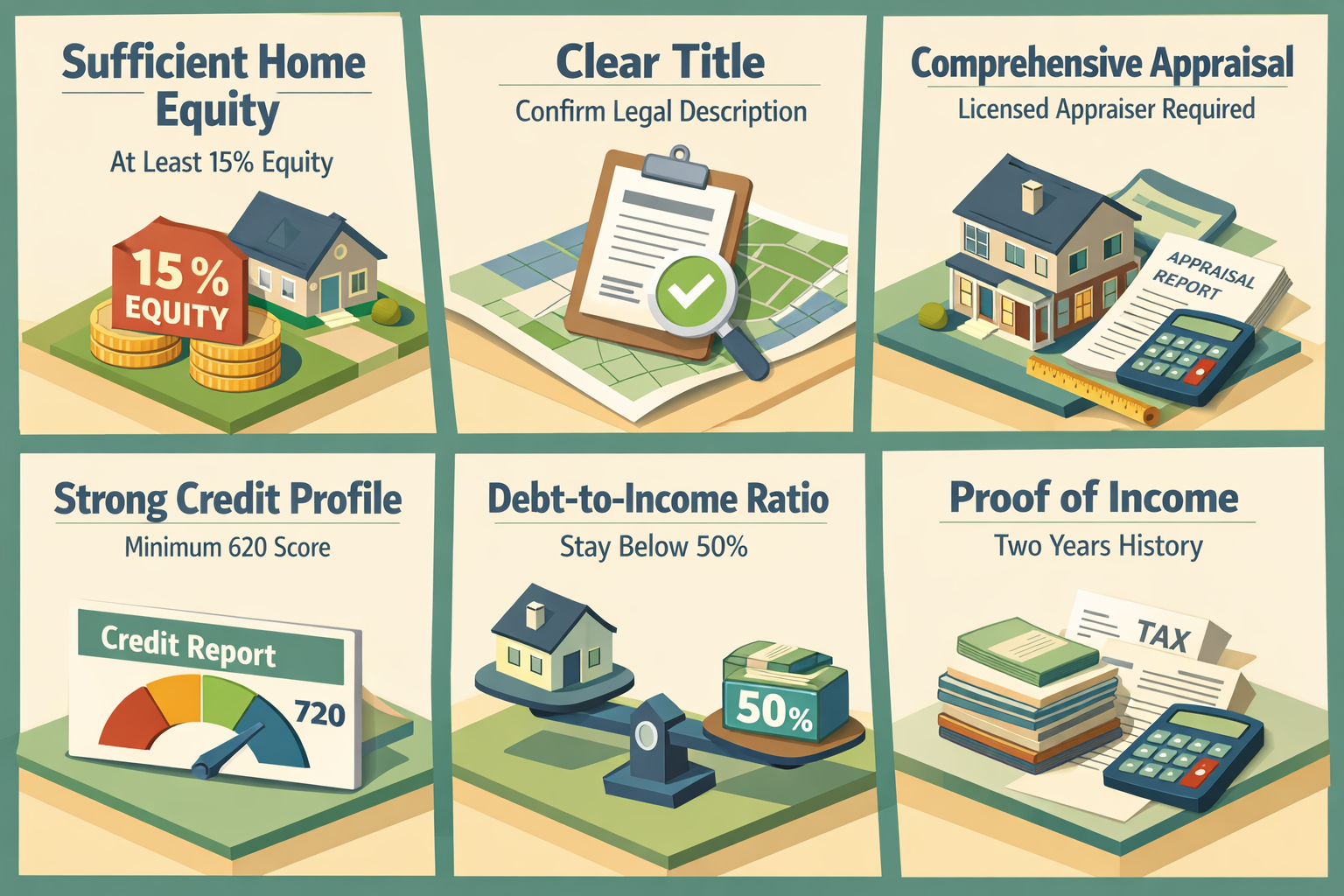

- Sufficient Home Equity: Most lenders require a combined loan-to-value (CLTV) ratio of 80% to 85% or lower, meaning you generally need at least 15% to 20% equity in your property with multiple adjacent vacant lots after the HELOC is factored in. With vacant lots in the mix, the appraised value calculation may be more conservative, so having substantial equity is especially important.

- Clear Title and Parcel Documentation: Lenders will want to confirm how the lots are legally described and whether they're on the same deed as your primary residence. Title searches and surveys may be required to establish clean ownership.

- Comprehensive Property Appraisal: A licensed appraiser will need to assess the entire property, including the vacant lots. Appraisers may use comparable sales of similar land parcels in the area, which can be challenging in rural or unique markets where comps are scarce.

- Strong Credit Profile: A credit score of 620 is often cited as a minimum threshold, though many lenders prefer scores of 680 or higher for non-standard properties. A stronger credit history may help offset some of the perceived risk tied to the land.

- Debt-to-Income Ratio (DTI): Lenders typically want your total monthly debt payments — including the new HELOC — to stay below 43% to 50% of your gross monthly income. The exact threshold may vary by lender and loan program.

- Proof of Income and Employment Stability: Two years of consistent income history, supported by tax returns and pay stubs, is a common expectation. Self-employed borrowers may need additional documentation.

How Lenders Evaluate HELOC on Property with Adjacent Land

When a lender reviews a HELOC on property with adjacent land, their underwriting process typically goes deeper than it would for a traditional single-family home on one lot. Here's what that review might look like:

Parcel Configuration and Use

Underwriters will closely examine whether the vacant lots are contiguous with the primary residence lot and whether they share legal access. Lots that are completely integrated with the home parcel — such as a large country property — may be treated as one unit. Separately deeded lots might require the lender to evaluate each parcel independently or simply exclude them from the collateral entirely.

Zoning and Development Potential

Lenders may consider the zoning classification of the vacant lots. Residentially zoned lots with utilities available and road frontage tend to carry more lendable value than raw, undeveloped land without infrastructure. If the lots have clear development potential, this could work in your favor during the appraisal process.

Marketability of the Collateral

A key concern for any lender is: if we had to sell this property to recover our funds, could we do it quickly and at a fair price? Properties with multiple vacant lots can be harder to sell as a package, which may lead lenders to apply a more conservative loan-to-value ratio or require additional documentation.

Environmental and Legal Considerations

Lenders may also check for environmental liens, easements, or deed restrictions that could limit the use or sale of the vacant lots. Any unresolved legal matters could delay or derail your application, so it's wise to review these issues before you apply.

Tips for Strengthening Your HELOC Application

If your property includes vacant lots and you're planning to apply for a HELOC, a little preparation can go a long way. Here are some practical strategies that may improve your chances of approval:

- Get a Pre-Appraisal Assessment: Before formally applying, consider consulting with a local appraiser who has experience valuing mixed-use or rural properties. This can give you a realistic picture of how lenders might value your collateral.

- Resolve Title Issues Early: Pull a title report on all parcels and address any liens, easements, or ownership disputes well before submitting your application. Clean title is non-negotiable for most lenders.

- Consolidate Parcels if Possible: Depending on your county's regulations, you may be able to merge adjacent lots into a single parcel with your primary residence. This can simplify the appraisal and underwriting process significantly.

- Boost Your Credit Score: Pay down revolving balances, avoid new credit inquiries, and make sure your credit report is free of errors. A higher credit score can help compensate for the added complexity of your property.

- Shop Multiple Lenders: Not all lenders have the same appetite for non-standard properties. Community banks, credit unions, and portfolio lenders — those who keep loans on their own books rather than selling them — may be more flexible than large institutional lenders.

- Document the Land's Value and Use: Prepare a clear summary of each lot's size, zoning, improvements (if any), and any plans you have for the land. The more information you provide, the easier it is for the lender to assess risk.

Alternative Financing Options to Consider

If a traditional HELOC turns out to be difficult to obtain because of your property's configuration, don't lose hope. There are several alternative financing routes that may be worth exploring.

Cash-Out Refinance

A cash-out refinance replaces your existing mortgage with a new, larger loan and gives you the difference in cash. Some lenders may be more willing to fold adjacent land into a cash-out refinance if they're already securing the primary residence. However, this option resets your mortgage terms, so it's worth weighing the long-term cost carefully.

Land Equity Loan

Some lenders offer standalone land equity loans secured specifically by vacant land. These products tend to carry higher interest rates and stricter LTV requirements than standard home equity products, but they could provide access to funds if the land holds significant value.

Portfolio Loans

Portfolio lenders write their own underwriting rules, which means they may have more flexibility when it comes to properties with unusual configurations. If your property doesn't fit neatly into conventional guidelines, a portfolio loan could be a practical solution.

Home Equity Loan

If a revolving line of credit isn't essential, a fixed-rate home equity loan — sometimes called a second mortgage — may be easier to structure for non-standard properties. You receive a lump sum upfront and repay it in fixed monthly installments, which some lenders find simpler to underwrite against complex collateral.

●Conclusion

Navigating the requirements for a HELOC on a property with multiple adjacent vacant lots takes more preparation than a standard home equity application — but it's far from impossible. The key is understanding how lenders view your property, addressing potential red flags early, and working with financing professionals who have experience with non-standard collateral. Whether you decide to pursue a HELOC, a cash-out refinance, or an alternative lending product, being well-informed puts you in the strongest possible position. At LoanWise, we're here to help homeowners and real estate investors find the right financing solutions, no matter how unique their property may be. Ready to explore your options? Connect with a LoanWise lending specialist today and take the next step with confidence.