Retirement is meant to be a time of financial peace — but if you're still carrying an adjustable-rate mortgage (ARM), that peace can feel fragile. ARM loans are designed with an initial fixed-rate period, after which the interest rate adjusts periodically based on market conditions. For retirees living on a fixed income, those unpredictable rate changes can create real budgetary stress. The good news is that there are several solid options for refinancing ARM mortgage with retirement income that can help you transition into a more stable financial position. This guide walks you through what to expect, how lenders evaluate your application, and which loan paths may be the best fit for your situation.

Why Retirees With ARMs Should Consider Refinancing Now

An adjustable-rate mortgage can seem appealing when rates are low, but as the rate adjustment period kicks in, monthly payments can climb significantly. For homeowners who were still earning a salary when they took out the loan, these fluctuations were manageable. In retirement, however, that flexibility disappears. Most retirees rely on predictable income sources — Social Security, pension payments, IRA distributions, or investment income — and a sudden mortgage payment increase can disrupt an entire budget.

Refinancing ARM mortgage into a fixed-rate mortgage could lock in a consistent monthly payment for the life of the loan. That kind of certainty is especially valuable when you're managing a retirement portfolio. Beyond payment stability, refinancing may also offer the opportunity to shorten your loan term, reduce your interest rate (depending on current market conditions), or even access home equity if needed.

It's worth noting that mortgage rates shift over time, and when you choose to refinance matters. Working with a knowledgeable lending advisor can help you time the decision strategically, balancing current rates against the costs of refinancing itself.

How Lenders Evaluate Retirement Income for Mortgage Qualification

One of the most common concerns among retirees is whether their income will be sufficient to qualify for a refinance. The short answer is: it often can be, but the documentation process looks different than it does for traditional W-2 earners. Lenders are primarily concerned with your ability to repay the loan, so they'll look carefully at the types, stability, and continuity of your income sources.

Accepted Retirement Income Sources

Most conventional and government-backed lenders accept the following income types when evaluating a refinance application from a retiree:

- Social Security benefits: These are typically well-regarded because they're government-guaranteed and continue for life. Lenders may also gross up this income by a certain percentage since it's often not taxed at the full rate, which could help your qualifying numbers.

- Pension and annuity income: Regular payments from a pension plan or annuity are generally treated similarly to a salary, provided you can document the payment schedule and expected duration.

- IRA and 401(k) distributions: If you're already taking regular distributions, lenders may count this as qualifying income. Some lenders may also use an asset depletion or asset dissipation method, where they calculate how long your retirement assets could generate income, even if you're not actively withdrawing.

- Investment and dividend income: Consistent dividends or interest income from brokerage accounts may be counted, particularly if it has been received for at least two years and is expected to continue.

- Part-time or self-employment income: If you're doing consulting or freelance work in retirement, some lenders will include this, though they may require two years of documented income history.

The key is documentation. Lenders will typically ask for award letters, bank statements, tax returns, and brokerage account statements to verify and support your income claims. Being organized and thorough with paperwork can make the qualification process smoother.

Exploring Your Options for Refinancing ARM Mortgage with Retirement Income

There's no single path when it comes to refinancing — your best option will depend on your financial profile, how much equity you have, your credit standing, and your long-term goals. Here's a look at the most commonly available routes for retirees looking to exit an ARM.

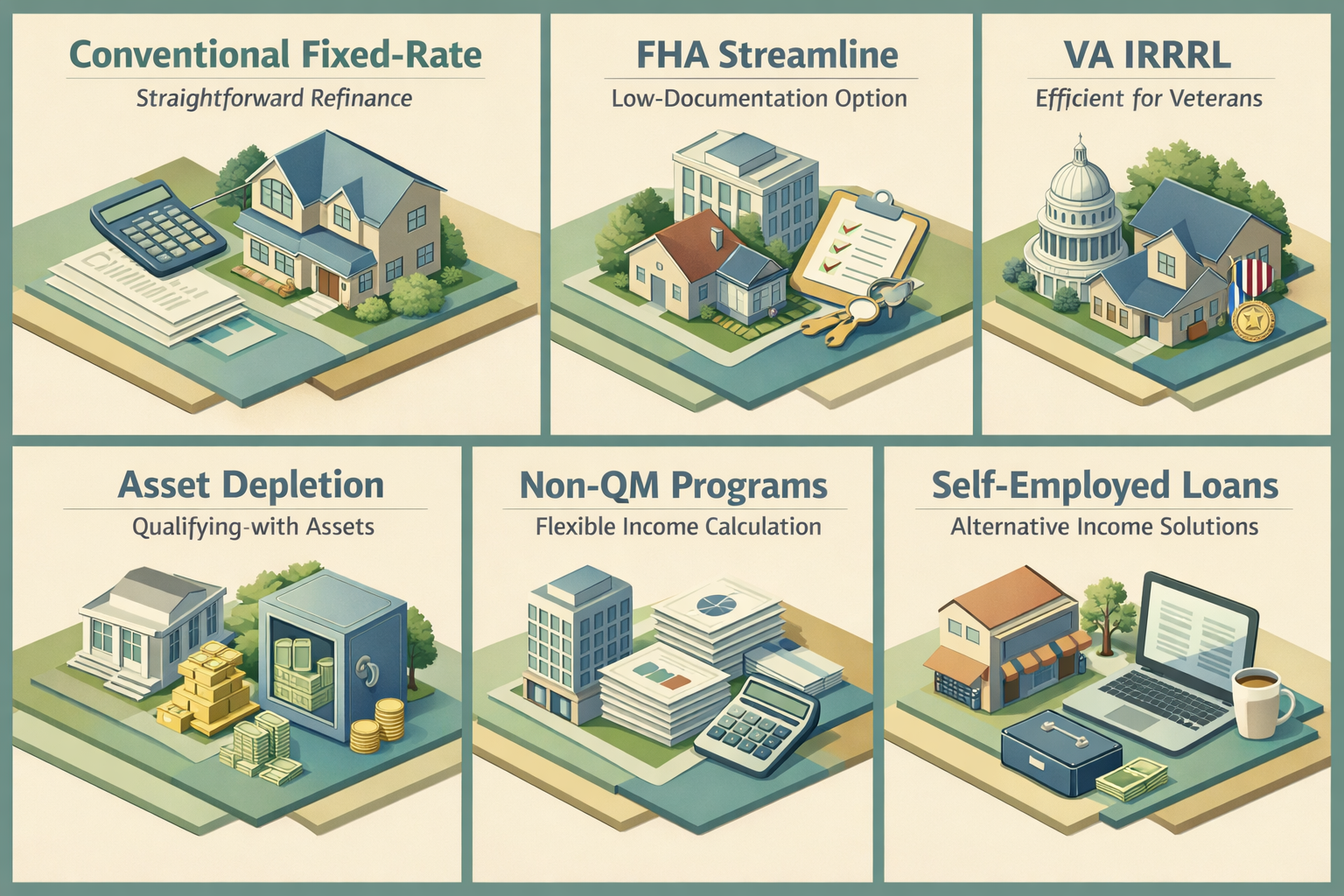

Conventional Fixed-Rate Refinance

A conventional 30-year or 15-year fixed-rate mortgage is one of the most straightforward ways to replace an ARM. If you have solid credit and enough verifiable income, a conventional refinance through Fannie Mae or Freddie Mac guidelines may be accessible. Fannie Mae, in particular, has guidelines that allow asset depletion as a qualifying income method — a significant advantage for retirees with substantial savings but modest monthly income.

FHA Streamline or Standard FHA Refinance

If your current mortgage is FHA-insured, an FHA Streamline Refinance could be a low-documentation option that simplifies the process. Standard FHA refinances are also available and may be more flexible with credit requirements compared to conventional loans. This could be a helpful path for retirees whose credit profile isn't perfect but whose equity position is strong.

VA Interest Rate Reduction Refinance Loan (IRRRL)

For retired military veterans, the VA IRRRL — often called the VA Streamline Refinance — is one of the most efficient ways to move from an ARM to a fixed-rate loan. It typically requires minimal paperwork, no appraisal in many cases, and no income verification in some scenarios. If you're eligible, this could be among the most retiree-friendly options for refinancing ARM mortgage with retirement income.

Asset Depletion or Asset Dissipation Loans

For retirees who hold significant assets but don't show enough traditional monthly income to qualify under standard guidelines, asset depletion loans can be a viable solution. In this approach, a lender divides your total eligible assets by the remaining loan term in months to calculate a hypothetical monthly income. This method can significantly boost your qualifying income figure without requiring you to actually draw down those assets.

Non-QM (Non-Qualified Mortgage) Programs

Non-QM lenders operate outside of standard agency guidelines and may offer greater flexibility in how income is calculated and documented. Bank statement loans, for example, allow retirees who receive irregular income or investment distributions to qualify based on 12 to 24 months of bank statements rather than traditional tax returns. These products typically carry slightly higher rates, but they can open doors for borrowers who don't fit the conventional mold.

Credit Score and Debt-to-Income Ratio Considerations for Senior Borrowers

Your credit score remains one of the most important factors in any refinance application, regardless of age. Lenders use it to assess repayment risk, and it has a direct impact on the interest rate you'll be offered. Most conventional refinance programs prefer a credit score of at least 620, though better rates are generally available at 740 or above. FHA programs may allow scores as low as 580 in some cases.

If your credit score has slipped in recent years — perhaps due to medical expenses, reduced income, or changes in credit utilization — it may be worth spending a few months improving it before applying. Paying down revolving balances, correcting errors on your credit report, and avoiding new credit inquiries are all steps that might help lift your score meaningfully.

Debt-to-income (DTI) ratio is the other major qualifier. Lenders typically look for a DTI below 43% for conventional loans, though some programs allow up to 50% with compensating factors. Because retirement income is often lower in absolute terms than working income, managing your DTI carefully is essential. Paying off other debts — car loans, credit cards — before refinancing can improve your ratio and strengthen your application considerably.

Weighing the Costs of Refinancing Against Long-Term Savings

Refinancing isn't free, and for retirees especially, the upfront costs deserve careful consideration. Closing costs on a refinance typically range from 2% to 5% of the loan amount, though this can vary depending on the lender, loan type, and your location. These costs may include origination fees, appraisal fees, title insurance, and prepaid escrow items.

The critical calculation is your break-even point — the number of months it takes for your monthly payment savings to offset the cost of refinancing. If you plan to stay in your home for many years, and your new payment is meaningfully lower than your current adjusted ARM payment, a refinance could make strong financial sense. But if you're considering downsizing in the near term, the math might not work in your favor.

Some lenders offer no-closing-cost refinance options, where the costs are either rolled into the loan balance or offset by a slightly higher interest rate. While this eliminates the upfront burden, it's important to model out the total cost over time to ensure you're making the most financially sound choice for your situation.

Practical Steps to Strengthen Your Refinance Application as a Retiree

If you're ready to explore the options for refinancing ARM mortgage with retirement income, a little preparation can go a long way. Here are some practical steps to set yourself up for a smoother process:

- Gather income documentation early: Compile Social Security award letters, pension statements, tax returns from the past two years, and recent bank and brokerage statements. The more organized you are, the faster your application can move.

- Check your credit report: Review all three major credit bureaus — Equifax, Experian, and TransUnion — for errors. Disputing inaccuracies before you apply can protect your score.

- Calculate your home equity: A higher equity position (typically 20% or more) gives you access to more loan programs and better rates. If your home has appreciated, you may have more equity than you realize.

- Compare multiple lenders: Rates and program eligibility can vary widely between lenders. Consulting with both traditional banks and mortgage brokers who specialize in retirement lending can give you a more complete picture.

- Consider working with a HUD-approved housing counselor: Free or low-cost counseling is available and can help you evaluate your options for refinancing ARM mortgage objectively before committing to a loan.

Taking these steps before you formally apply could make the difference between an approval and a denial — and help ensure that the loan terms you receive truly align with your refinancing ARM mortgage with retirement income goals.

●Conclusion

Navigating a mortgage refinance in retirement doesn't have to be overwhelming. Whether you're looking to lock in a stable fixed rate, reduce your monthly payment, or simply eliminate the uncertainty of an adjustable-rate loan, there are meaningful paths forward. Lenders today recognize that retirement income comes in many forms, and a growing number of programs are designed to accommodate borrowers in your situation. The most important step is to start the conversation — explore your eligibility, compare your options, and make a decision that supports the financial security you've worked so hard to build. At LoanWise, we're here to help you find the right lending solution for every stage of life.